Introduction

Welcome to the September 2020 National Apartment List Rent Report. As the country continues to navigate the coronavirus pandemic and double-digit unemployment, many renters are still moving and looking for new homes to match their changing opportunities and lifestyles. Peak moving season was busy, but the economic slowdown that accompanied Covid-19 has tempered rent growth. Our national rent index inched up marginally by 0.1 percent during August, and national rents are just 0.3 percent above where they were a year ago. This represents the smallest national year-over-year rent increase we’ve seen in August since we started tracking rent prices in 2014. That said, there is significant variation in rent changes across regions in the U.S. Many small markets are seeing rent growth pick back up, while some of the largest and priciest markets continue to see material rent drops.

Rents tick up nationally, but growth remains sluggish

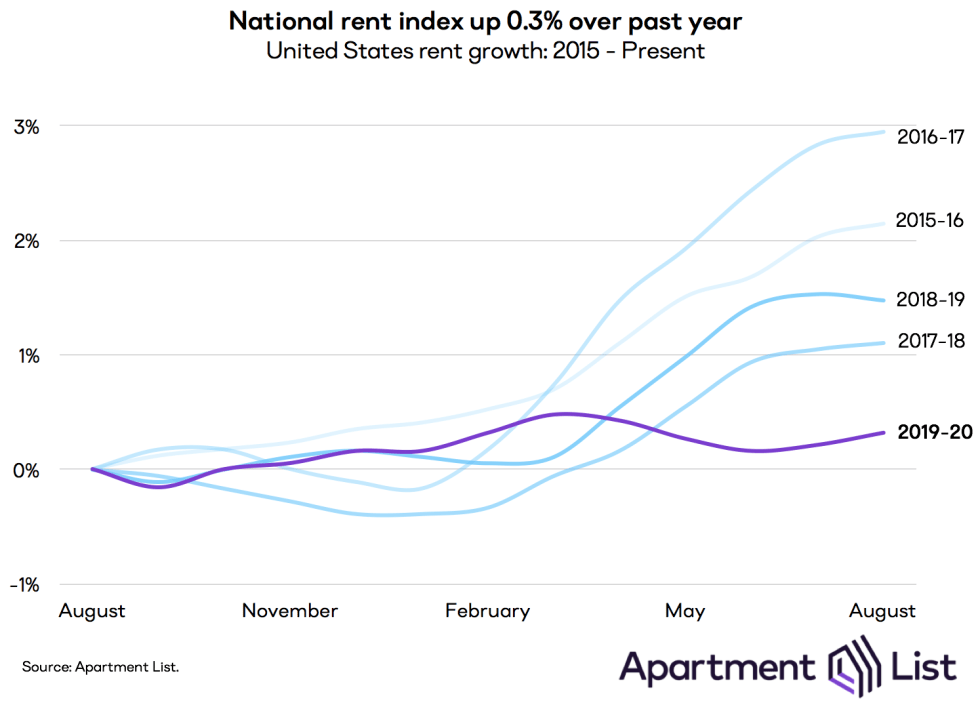

Over the past month, our national rent index inched up by 0.1 percent. Despite this slight increase, our national index has still experienced a cumulative decline of 0.2 percent since the pandemic began. While this dip may seem modest, it is occurring at a time of year when rent growth is normally at its fastest due to seasonality in the market. Rent growth from March to August has ranged from 1.2 percent to 2.5 percent in prior years, going back to 2014, when our rent estimates begin. And over the entirety of the past year, our national index has increased by just 0.3 percent. As shown in the chart below, this is by far is by far the lowest year-over-year growth rate that we’ve observed in August over any of the past five years. The fact that we’re seeing rents decrease at what is normally the peak season for rental activity is reflective of the financial hardship and shifting preferences being imposed by the pandemic.

A number of factors are driving the recent rental market softness. Public health concerns are causing many to delay both moves and new household formation. In a recent survey, we found that 33 percent of Americans are less likely to move during the remainder of 2020 because of the pandemic, and that these changing plans are most commonly attributed to the belief that it is not currently safe to move. At the same time, we’re seeing a spike in adults moving in with family this summer, which drags down rental demand further.

Widespread economic hardship is also keeping rents steady. Today’s unemployment rate remains at a historic high, and many are struggling to make their monthly housing payments and accumulating unpaid rent. Job growth is a strong driver of housing demand, and as a V-shaped recovery starts to feel out of reach, the rental market is cooling.

Property owners are beginning to respond to these new realities by offering lower prices in order to fill vacancies. The overall decline in our national index is still fairly modest, and is now showing signs of levelling off, but this masks significant variation across markets. Prices are responding much more rapidly in the most heavily impacted parts of the country, which we explore below.

Rents are falling in the largest and most expensive markets

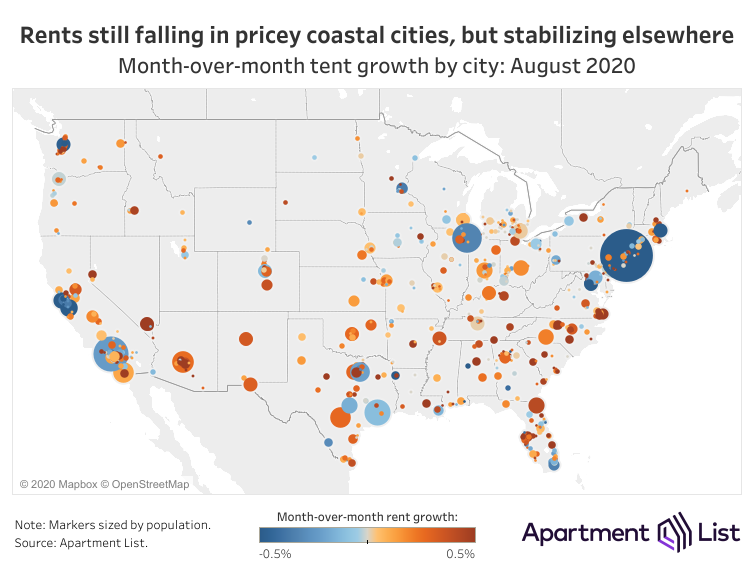

Market-level data give us a clearer picture of the significant variation in pandemic rent changes across the country. Of the 100 largest cities for which we have data, 42 have seen rents fall or hold steady since the start of the pandemic in March, however, 67 have experienced month-over-month increases.

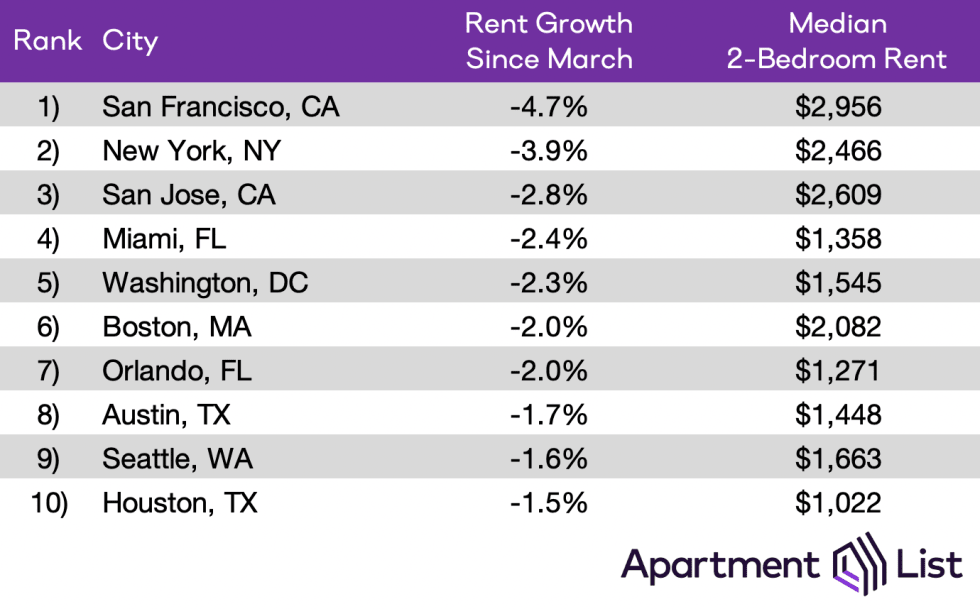

The cities experiencing the biggest dropoff in rent prices generally fall into two categories:

The first group is typified by Orlando (-2.0 percent rent decline since March) and Miami (-2.4 percent rent decline). As tourism ground to a halt at the onset of the pandemic, we predicted these cities would be particularly vulnerable because they have the 2nd and 3rd highest shares of workers facing extreme employment risk. Today, with a significant share of households now facing financial hardship, landlords have begun to lower rents in order to attract qualified renters to fill their vacancies.

The second group contains cities that entered the pandemic with high rents and supply shortages, topped off by the nation’s priciest markets: San Francisco, New York, and San Jose. Since the start of the pandemic, San Francisco rents have fallen by 4.7 percent, New York rents have fallen 3.9 percent, and San Jose rents have cooled 2.8 percent. These markets are most affected by a number of critical trends, such as concerns over density during the pandemic, the rise of remote work opportunities, and the changing constraints on international immigration.

Year-over-year rent growth is fastest in affordable secondary cities

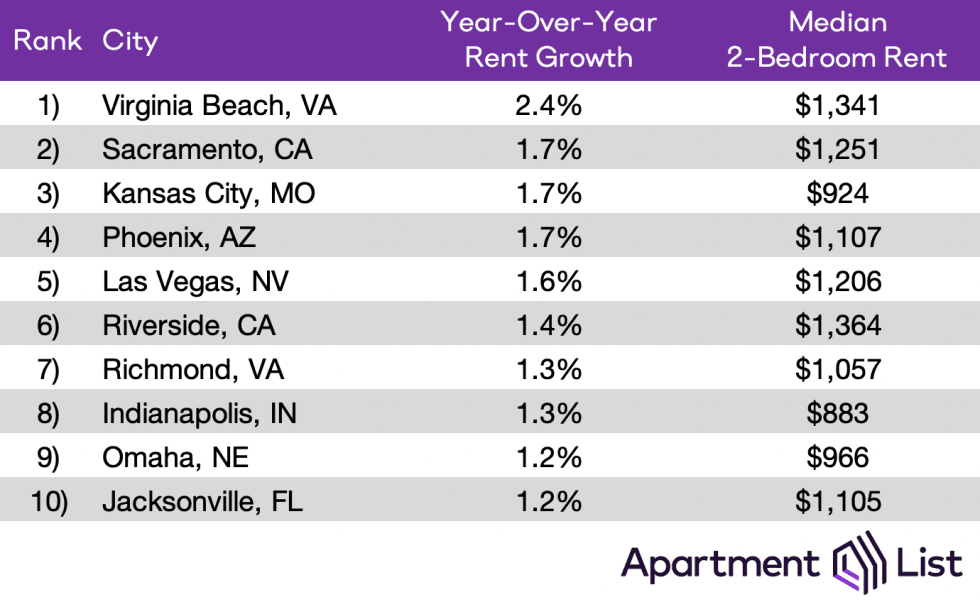

While rents fall in the country’s largest and priciest markets, a number of affordable midsize metros are gaining momentum. Virginia Beach leads the pack, with 2.4% year-over-year rent growth. Sacramento, Riverside, and Richmond are also heating up. In our latest analysis of renter search patterns, we noted that these three markets saw a large increase this year in their inbound interest from out-of-town. After years of San Francisco, Los Angeles, and DC taking center-stage, their neighbors appear to be stepping into the spotlight as the pandemic shifts market preferences.

Notably, cities like Sacramento, Riverside, and Richmond all lie within long commuting distance of “superstar cities” (San Francisco, Los Angeles, and Washington, D.C., respectively). Although a wider embrace of remote work may mean that knowledge workers will no longer need to go into the office on a daily basis, many of them may still want to be within reasonable distance of these thriving job centers. Broadly speaking, the list above indicates that rental demand has not fallen off as quickly in the nation’s more affordable housing markets. That said, even among this group of cities, rent growth remains quite modest – Virginia Beach is the only one of the nation’s 50 largest cities in which rents have grown by more than 2 percent over the past twelve months.

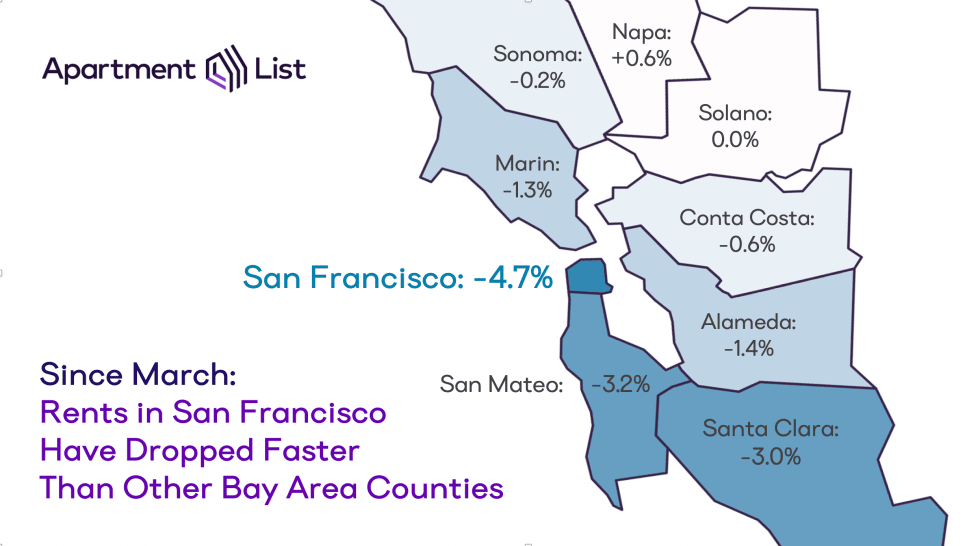

In San Francisco, rents are falling fastest in the core city

Delving a bit deeper into the data for San Francisco specifically, we notice an interesting nuance in rent changes throughout the region as a whole. Specifically, while the city of San Francisco has seen rents come down by 4.7 percent since March, surrounding regions have experienced more modest declines.

In the South Bay counties of San Mateo and Santa Clara, where rents also tend to be quite expensive, rents have fallen by 3.2 percent and 3.0 percent, respectively. Meanwhile, the more affordable East Bay counties of Alameda and Contra Costa have seen modest declines of 1.4 percent and 0.6 percent respectively, while rents in the North Bay counties of Marin and Sonoma have come down 1.3 percent and 0.2 percent, respectively. Rents in Solano County have held flat, while Napa County remains the only Bay Area locale to experience a slight (0.6 percent) increase in rent over the course of the pandemic.

As some Bay Area tech companies signal that a growing embrace of remote work will outlast the pandemic, many have hypothesized that workers will take advantage of this new flexibility by abandoning downtown in search of more space and greater affordability in the suburbs. However, a recent analysis of our user search data does not show San Francisco’s renters look to flee the core city in droves. Instead, a more significant factor could be diminishing demand from new renters moving in from across the country. Our latest renter migration report uncovered a steep year-over-year dropoff in the share of apartment searches coming to San Francisco from other parts of the country. This could be easing competition in San Francisco’s undersupplied housing market, pushing rent prices down for local movers.

Conclusion

Since the start of the COVID-19 pandemic, we have seen shelter-in-place ordinances put a halt to normal moving activity, combined with staggering job losses as huge segments of the economy were put on pause. These unprecedented forces have dampened the demand for rental housing across the country. 33 percent of Americans say that they are now less likely to move since this year, while the 21 percent who are more likely to move are being driven primarily by a need to find more affordable housing. These financial losses and general uncertainty are creating softness in the market. While rents have levelled off at the national level, prices are still declining rapidly in some markets.

As far as longer-term impacts, the pandemic’s effect on rent prices will depend heavily on how quickly the economy is able to recover. There are indications that the recovery will be more drawn out than many had initially hoped, making it likely that we’ll see a protracted uptick in downgrade moves as many households facing financial hardship begin looking for more affordable housing. We may also see a significant slowdown in new household formation, as more Americans move in with family or friends to save on housing costs. These trends could mean that competition will remain tight for rental units at the middle and lower ends of the market, while luxury vacancies get harder to fill. As long-term remote work gains traction, we may also be seeing the beginning of a shift away from expensive downtown markets and toward more affordable suburbs. The decisions that families and businesses are making today are already starting to reshape the rental market, even if national rents remain largely unchanged.

To learn more about the data behind this article and what Apartment List has to offer, visit https://www.apartmentlist.com/.

Sign up to receive our stories in your inbox.

Data is changing the speed of business. Investors, Corporations, and Governments are buying new, differentiated data to gain visibility make better decisions. Don't fall behind. Let us help.

Sign up to receive our stories in your inbox.

Data is changing the speed of business. Investors, Corporations, and Governments are buying new, differentiated data to gain visibility make better decisions. Don't fall behind. Let us help.