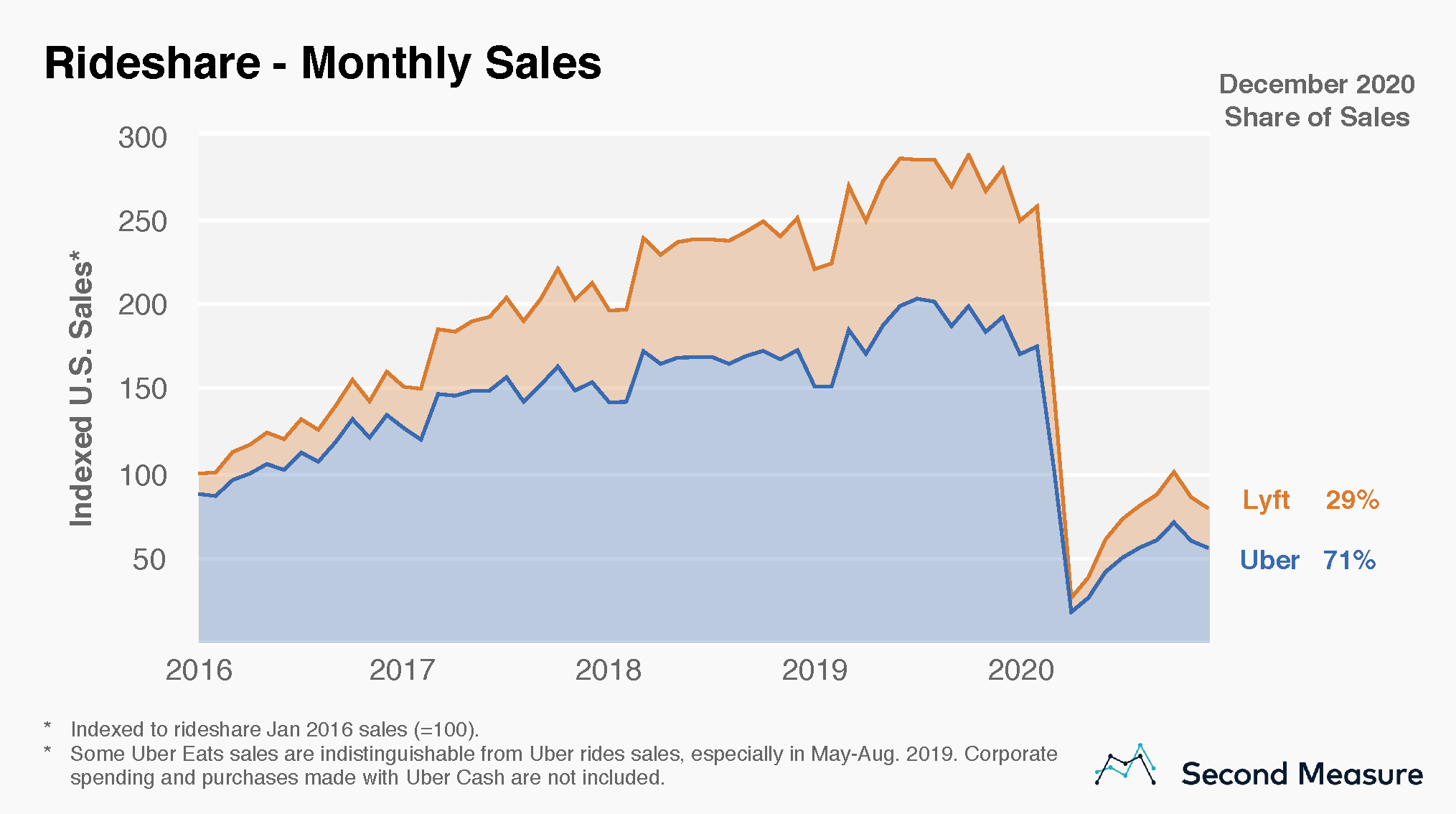

When U.S. cities and states faced shelter-in-place orders to limit the spread of the coronavirus, Americans’ reduced mobility resulted in plummeting sales at rideshare companies. While rideshare sales have been gradually recovering over the past several months, November marked a decline for the first time since April. Sales declined even further in December, with Uber sales down 71 percent year-over-year and Lyft sales down 73 percent year-over-year.

In August, rideshare operators entered a standoff with regulators in California over how employees are classified and compensated. Both Uber and Lyft were on the brink of suspending operations before reaching an agreement with the state to continue service. In November, Uber and Lyft won a major victory when California voters approved Proposition 22, which will allow gig economy companies to continue classifying their drivers as independent contractors rather than as employees.

The breakdown of December sales between Uber and Lyft reveals that market share has remained stable, relative to prior months. Uber still dominates, taking in 71 percent of U.S. rideshare spending. Starting in August 2017, Uber’s share of the market excludes most Uber Eats transactions, though some remain indistinguishable, especially from May to mid-August 2019. Both Uber and Lyft are also reportedly making inroads with corporate rideshare clients, although Second Measure’s analysis excludes business spending.

Rideshare trends vary by coast

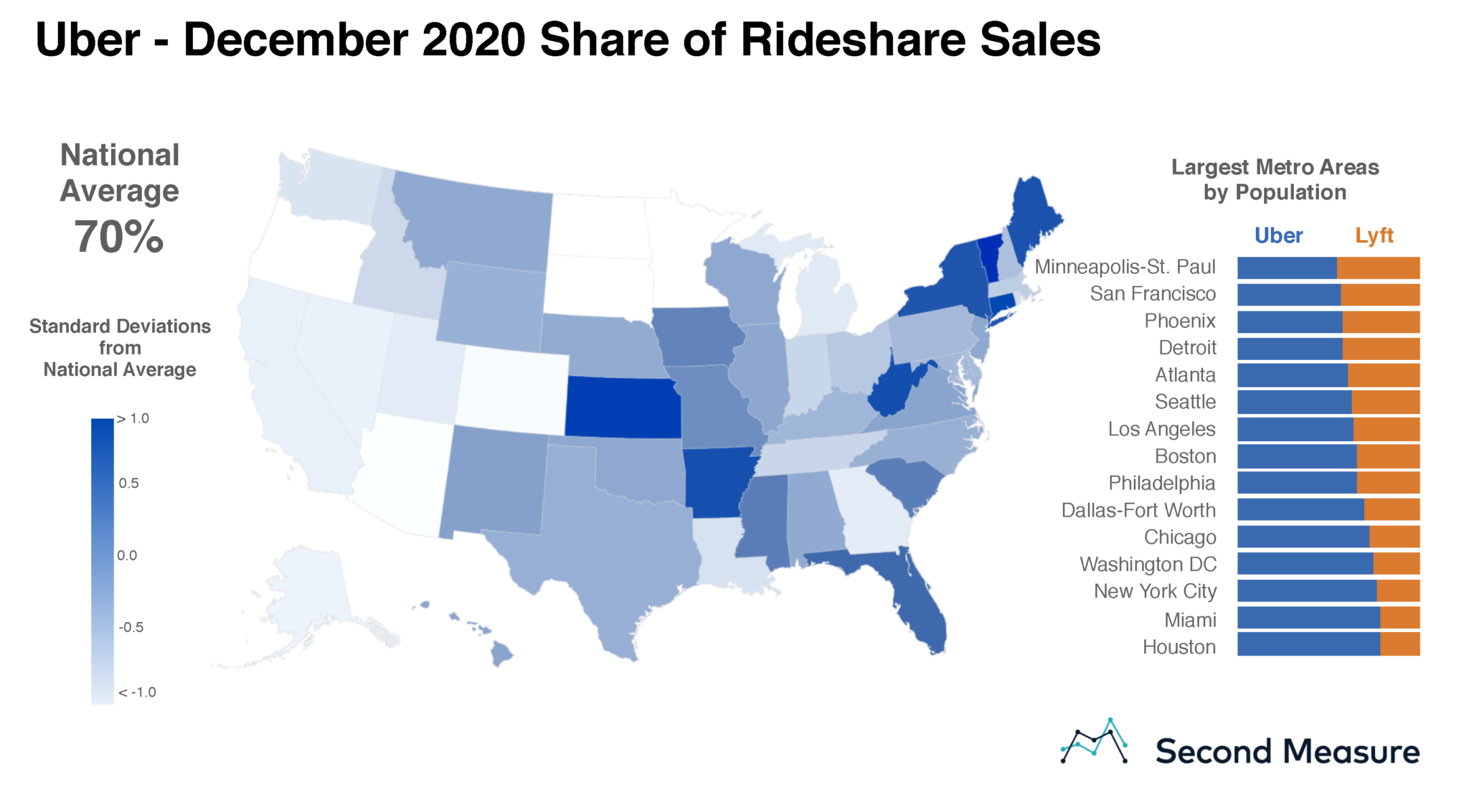

Though Uber commands the U.S. market, a geographic analysis of rideshare sales reveals that riders are more likely to hail a Lyft on the West Coast or Midwest than in the Northeast. In several major cities, Lyft’s market share is higher than the national average. In December, 45 percent of rideshare sales went to Lyft in Minneapolis-St. Paul, its highest share among the top 15 most populous U.S. cities.

Few customers use both Uber and Lyft

Nationwide, most customers are loyal to just one rideshare service. Only 8 percent of U.S. rideshare customers used both Uber and Lyft in December. Sixty-six percent used only Uber, while 26 percent used only Lyft.

Uber also wins out on rider engagement. Riders who use both Uber and Lyft typically spend more on rideshare each year than riders who are loyal to a single service. And, on average, these riders who hail cars on both services spend more with Uber than Lyft. Over the past year, the average rider of both Uber and Lyft spent $272 with Uber, and $184 at Lyft.

Uber also among top U.S. meal delivery companies

Uber has established itself as more than a rideshare company. Its successful foray into food delivery has surprised its own CEO. As meal delivery companies are thriving in the COVID-19 era, Uber purchased Postmates in early July.

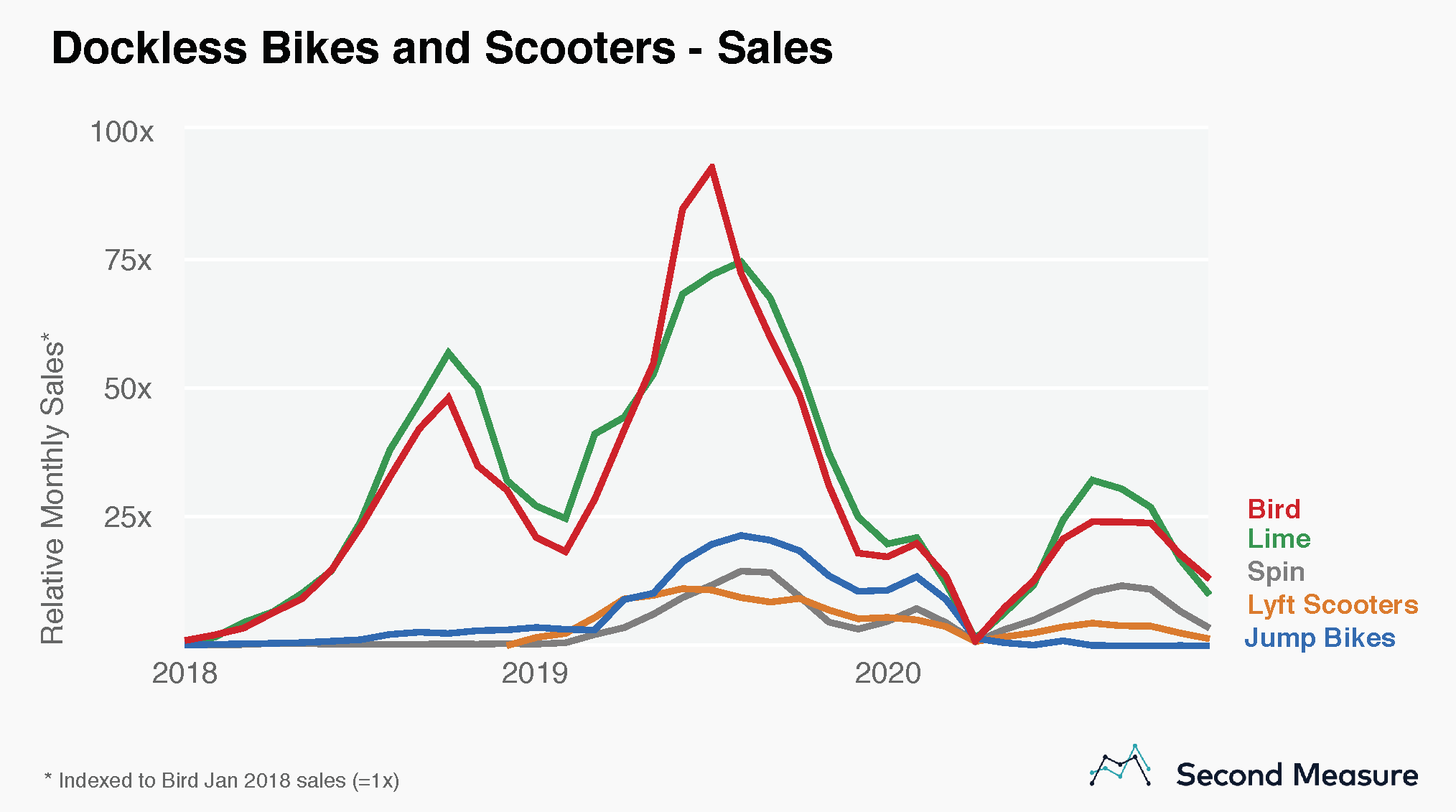

Uber and Lyft among brands vying for scooter and bike sales

Uber and Lyft have also segued into scooters and bikeshare. Lyft launched a scooter fleet in September 2018, but last fall, it announced it was pulling scooters out of six U.S. cities due to a lack of riders. In May 2020, Lime received funding from Uber and also acquired Jump Bikes, which Uber bought in 2018. Micro-mobility has also shown declining sales in light of the pandemic, falling 56 percent year-over-year, collectively.

Bird kept busy in late 2019, raising $275 million in new funding in October and launched a kids’ scooter, Birdie, in November. The company also acquired Scoot in June 2019.

In December 2019, Lime announced it would be leaving four U.S. markets and eight international ones. Even before COVID-19, Lime and its competitors were experiencing the annual winter slump after most saw sales grow over the summer. In 2019, Lime’s sales dropped 65 percent from July to December, while Bird’s sales fell 81 percent over the same period.

The legal landscape for scooters is perpetually shifting, as federal agencies and cities across the country grapple with regulating this new form of urban transport. In January 2020, it was reported that the U.S. Consumer Product Safety Commission conducted probes into scooter safety while the previous fall, Los Angeles suspended Uber’s scooter permit over a data-sharing dispute. Other cities are concluding pilot programs, seeking public feedback, and implementing strict regulations that have prompted some companies to leave the market.

Remembering rough roads traversed

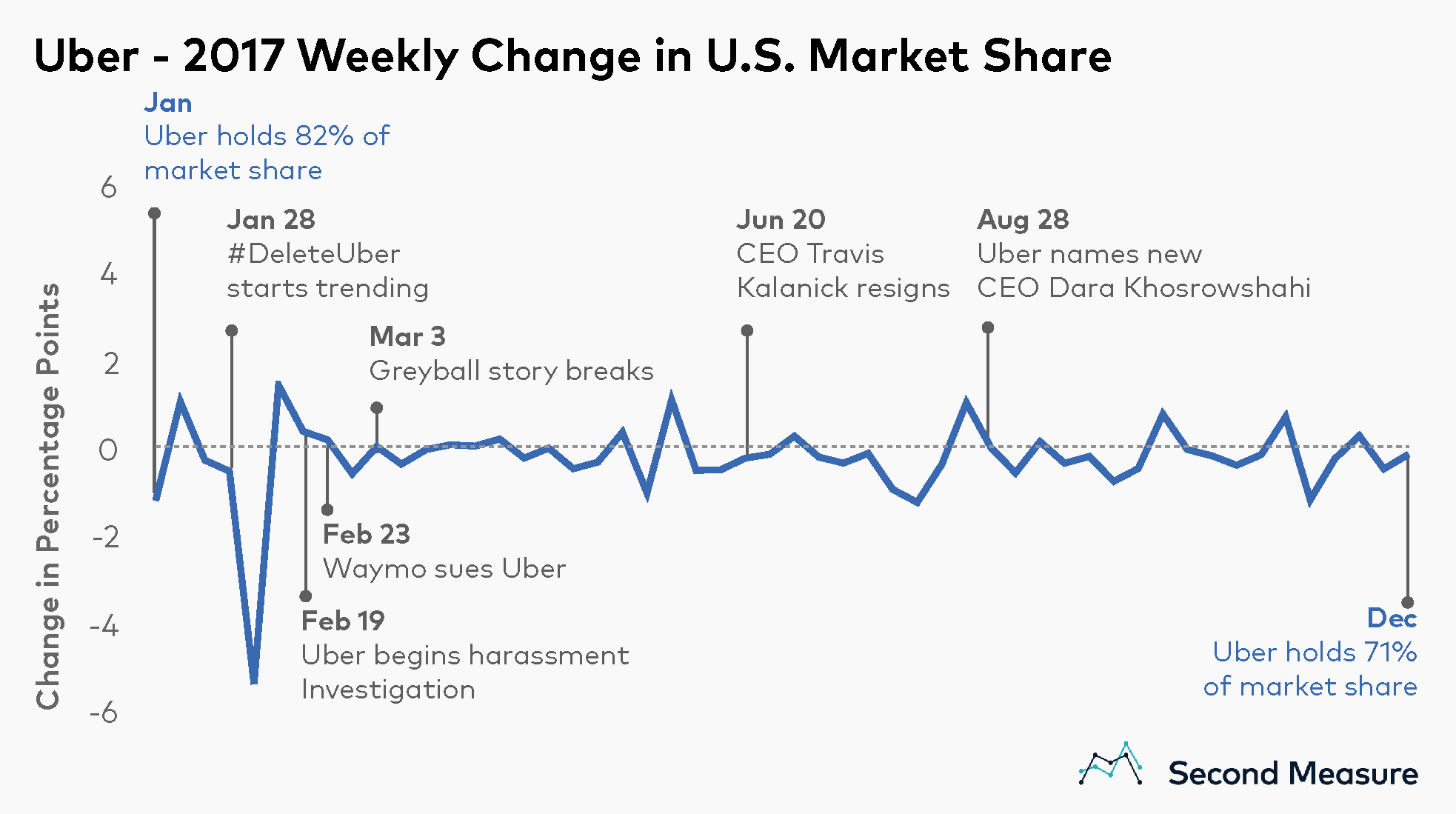

Though Uber has always worn the U.S. rideshare crown, one of the most pivotal years in its history was 2017. That January, the #DeleteUber hashtag went viral, and Uber’s market share dropped 5 percentage points in a single week, the start of what would turn out to be a challenging year.

Former CEO Travis Kalanick resigned in June 2017 following other publicized issues, including questions surrounding the company’s culture. A new CEO and 2018 brand overhaul have since helped Uber elevate its image and calm market-share fluctuations.

To learn more about the data behind this article and what Second Measure has to offer, visit https://secondmeasure.com/.

Sign up to receive our stories in your inbox.

Data is changing the speed of business. Investors, Corporations, and Governments are buying new, differentiated data to gain visibility make better decisions. Don't fall behind. Let us help.

Sign up to receive our stories in your inbox.

Data is changing the speed of business. Investors, Corporations, and Governments are buying new, differentiated data to gain visibility make better decisions. Don't fall behind. Let us help.