It takes an affordable and sustainable exit plan to keep borrowers in their homes and preserve homeownership

Summary:

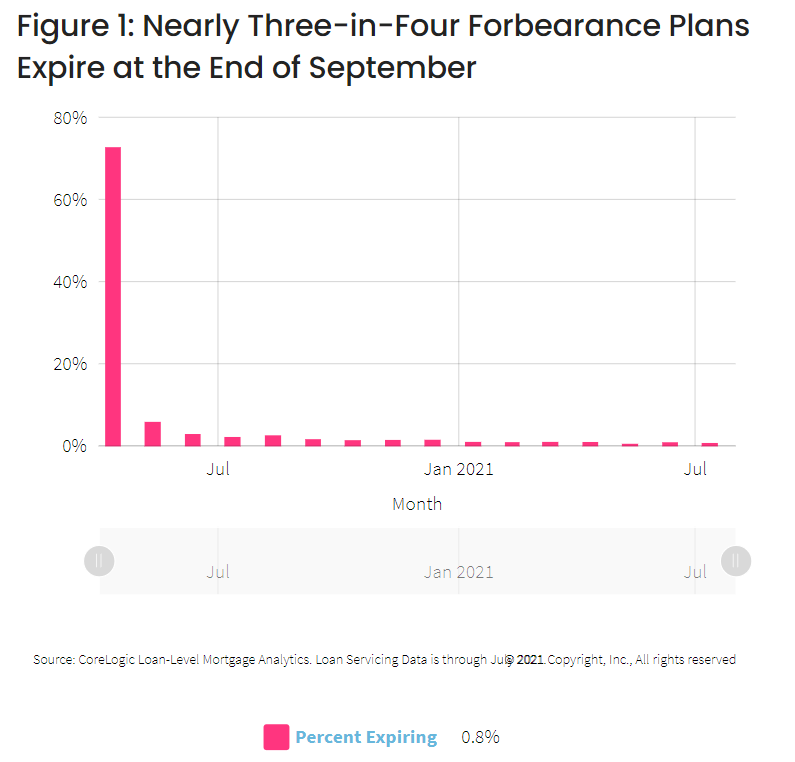

At the end of September 2021 – 18 months after the passage of the CARES Act which provided millions of homeowners the protection of COVID-19 payment forbearance – many mortgage loans are expected to reach the end of forbearance. That is, of an estimated 1.7 million mortgage loans that are in forbearance at the start of August, more than 1.2 million loans will reach the maximum 18-month term limit at the end of September, representing 73% of the total forbearance plans. Initially, a 360-day forbearance provision was authorized by the CARES Act for federally backed loans, but it was further extended by federal agencies for an additional six months.

As shown in Figure 1, the first wave of borrowers to exit forbearance will be the largest. These are the borrowers who entered a COVID-19 forbearance plan in April 2020, shortly after the CARES Act was signed into law on March 27, 2021. Expectedly, exit-related servicing demand – from contacting borrowers to handling borrowers request and working with borrowers through different options – could become overwhelming for servicers.

In addition to the large volume of forbearance exits, many borrowers will likely require assistance finding an affordable and sustainable exit plan so that borrowers could avoid foreclosure and remain in their homes. At the start of August 2021, one-in-two GSE backed loans and two-in-three federally insured FHA, VA, and USDA/RHS loans that are in forbearance – irrespective of the loans’ securitization status –are behind on mortgage payments, wherein borrowers typically have missed the last 12 payments.

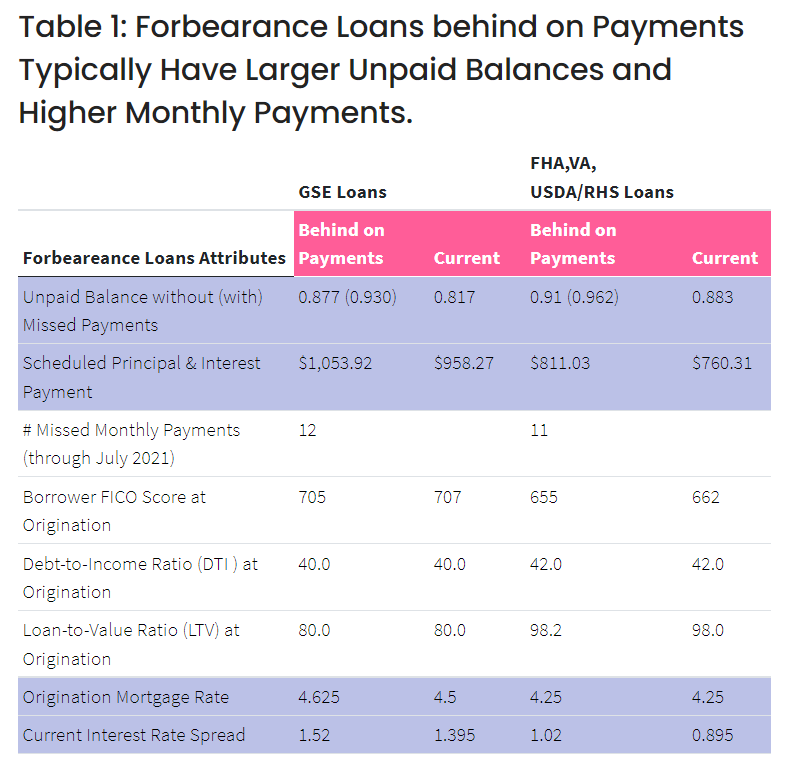

Table 1 provides a glimpse of potential challenges ahead should some borrowers find themselves financially strapped and unable to resume the pre-pandemic mortgage payments or need substantial monthly payment relief in an exit plan to avoid losing their homes. All the numbers are reported at the median value.

As shown in Table 1, whether missed payments are considered or not, forbearance plans that are behind on payments generally have a much higher unpaid principal balance (UPB) as a percentage of the origination loan amount, as well as higher scheduled monthly principal & interest payments. Among forbearances that are behind on payments with a GSE-backed loan, median UPB before missed payments is 0.877 with a scheduled payment amount of about $1,054 – meaning 87.7% of the original balance has remained unpaid at the time of entering forbearance. In comparison, borrowers who are current on their payments while in forbearance have a much lower UPB at 0.82, with a scheduled payment of $957. When missed payments are added to the unpaid principal, median UPB is up by more than five percentage points at 0.93.

There are similar differences among federally-insured FHA, VA and USDA/RHS loans: Forbearances that are behind on payments have a median UPB of 0.91 and 0.96 before and after missed payments, with a higher monthly payment of $811, compared to a UPB of 0.88 and $760 in monthly payment among the forbearance plans that are current on payments.

However, Table 1 reveals that key underwriting risk attributes at the time of origination are mostly similar between borrowers who are behind on payments and who are current on the payments despite being in a forbearance plan – suggesting that there are no clear sign of adverse risk selection on non-performing forbearance plans. For instance, for GSE backed forbearance plans the median borrower FICO score is 705 among loans that are behind on payments and 707 among loans that are current, whereas borrower FICO score among non-current FHA, VA and USDA/RHS forbearances is only slightly lower than the loans that are current (655 versus 662). Likewise, other risk attributes such as borrower DTI and LTV ratios show a similarity between non-current and current forbearance loans.

In addition, Table 1 reports the average mortgage rates and spread to prevailing market rates. The spread is calculated based on a loan’s type and term against corresponding market rates. In GSE backed forbearance plans, the average mortgage rate is 4.625% among the loans that are behind on payments and 4.5% for the loans that are current – resulting in a deep “in-the-money” spread of more than 1.5%.

Similarly, federally insured loans in forbearance plans have a median mortgage rate of 4.25% and spread at 1.0% and 0.9% respectively among non-current and current loans. An “in-the-money” spread – that is, a positive difference between the existing loan rate and refinancing rate – means that many loans in forbearance plans may be able to reduce their mortgage rate by refinancing.

While all exiting borrowers with modest or deep in-the-money interest spread could benefit from a rate reduction regardless of their exit options, it will be particularly helpful to those who can no longer afford to resume regular payments or require a loan modification – such as extending the maturity of the loan – to bring down post-forbearance payments.

It is true that rapidly rising home prices during the pandemic have boosted home equity, which is helpful in preventing borrowers from losing their home through foreclosure. But it will take an affordable and sustainable exit plan to keep borrowers in their homes and preserve homeownership.

To learn more about the data behind this article and what CoreLogic has to offer, visit https://www.corelogic.com/.

Sign up to receive our stories in your inbox.

Data is changing the speed of business. Investors, Corporations, and Governments are buying new, differentiated data to gain visibility make better decisions. Don't fall behind. Let us help.

Sign up to receive our stories in your inbox.

Data is changing the speed of business. Investors, Corporations, and Governments are buying new, differentiated data to gain visibility make better decisions. Don't fall behind. Let us help.