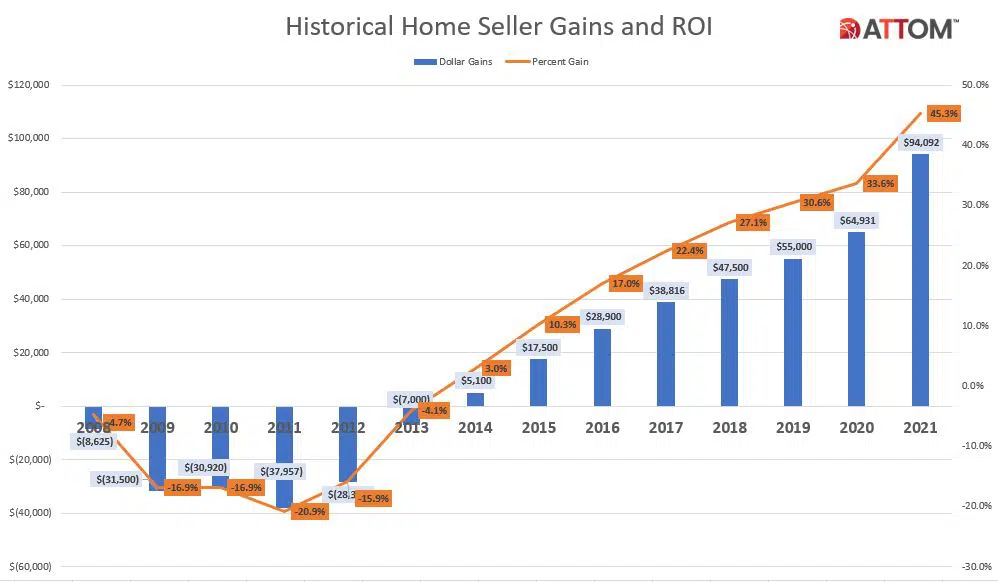

ATTOM, curator of the nation’s premier property database, today released its Year-End 2021 U.S. Home Sales Report, which shows that home sellers nationwide realized a profit of $94,092 on the typical sale in 2021, up 45 percent from $64,931 in 2020 and up 71 percent from $55,000 two years ago. Profits rose in more than 90 percent of housing markets with enough data to analyze and the latest figure, based on median purchase and resale prices, marked the highest level in the United States since at least 2008.

The $94,092 profit on the median-priced home sale in 2021 represented a 45.3 percent return on investment compared to the original purchase price, up from 33.6 percent last year and from 30.6 percent in 2019. The latest profit margin also stood out as the largest since at least 2008.

Both raw profits and ROI have improved nationwide for 10 straight years. Moreover, last year’s gain in ROI – up nearly 12 percentage points – was the biggest annual increase since 2013.

Profits shot up as the national median home price rose 16.9 percent in 2021 to $301,000, another annual record.

The combination of rising prices and profits came during a year when a decade-long boom in the national housing market steamed ahead both because of and in spite of the Coronavirus pandemic that caused widespread economic damage in 2021 and continued to threaten a recovery that began to took hold in 2021.

A surge of buyers financially unscathed by the pandemic continued flooding the market throughout 2021. They were driven heavily by a combination of historically low interest rates and a desire by many households to trade congested virus-prone areas for the perceived safety and wider spaces of a single-family home and yard. As they chased a tight supply of homes for sale, prices spiked and so did seller profits.

A few signs that prices could flatten out in 2022 emerged late last year in the form of declining affordability, lower investor profits and rising foreclosure activity. That was layered over rising inflation and likely increases in mortgage rates this year. But the current imbalance in demand and supply suggests that there is room for at least some additional price gains.

“What a year 2021 was for home sellers and the housing market all around the U.S. Prices went through the roof, kicking profits and profit margins up at a pace not seen for at least a decade. All that happened as the virus pandemic raged on, which actually helped drive the increases instead of stifle them,” said Todd Teta, chief product officer at ATTOM. “Households that escaped job losses from the pandemic dove into the market, in large part as a response to the crisis. And the rising demand led the market boom onward. No doubt, there are warning signs that the surge could slow down this year. But 2021 will go down as one of the greatest years for sellers and one of the toughest for buyers.”

Among 173 metropolitan statistical areas with a population greater than 200,000 and sufficient sales data in 2021, those in western states continued to reap the highest returns on investment, with concentrations on or near the West Coast. The West region had 16 of the 20 metro areas with the highest ROIs on typical home sales last year, led by Boise, ID (121.8 percent return on investment); Spokane, WA (86.5 percent); Bremerton, WA (82.7 percent); Prescott, AZ (81.2 percent) and Salem, OR (81.2 percent).

Prices rise at least 10 percent in three-quarters of the country as most markets again hit new highs

The U.S. median home price increased 16.9 percent in 2021, hitting an all-time annual high of $301,000. The annual home-price appreciation in 2021 outpaced the combined increases of 9.5 percent in 2020 plus 5.9 percent in 2019.

Since 2011, when the U.S. housing market was mired in the aftermath of the Great Recession of the late 2000s, the national median home price has risen 109 percent.

The latest price spike came as more than 5.7 million single-family houses and condominiums sold in 2021, the highest number since at least 2005.

All but four of the 173 metropolitan statistical areas with a population of 200,000 or more and sufficient home price data in 2021 saw median prices increase from 2020 while 124 saw prices jump at least 10 percent. Those with the biggest year-over-year increases in median home prices were Worcester, MA (up 39.6 percent); Barnstable, MA (up 39.2 percent); Boston, MA (up 28.8 percent); Boise, ID (up 27.2 percent) and Phoenix, AZ (up 26 percent).

Aside from Boston and Phoenix, the largest median-price increases in metro areas with a population of at least 1 million in 2021 came in Austin, TX (up 25.4 percent); Nashville, TN (up 22.2 percent) and Las Vegas, NV (up 21.5 percent).

Home prices in 2021 reached new peaks since the Great Recession in 168 of the 173 metros analyzed (98 percent), including New York, NY; Los Angeles, CA; Chicago, IL; Dallas, TX, and Houston, TX.

The four metro areas among the 173 where median prices dropped in 2021 were Gulfport, MS (down 4.9 percent); Peoria, IL (down 1.8 percent); Beaumont, TX (down 1.4 percent) and Kansas City, MO (down 0.7 percent). The smallest increase among the 173 metros was in Fort Wayne, IN (up 1.8 percent).

Profit margins up in almost 90 percent of nation

Profit margins on typical home sales rose from 2020 to 2021 in 150 of the 173 metro areas with sufficient data to analyze (87 percent).

The largest increases in investment returns came in Salisbury, MD (margin up 267.2 percent); Lafayette, LA (up 227.4 percent); Montgomery, AL (up 195.4 percent); Mobile, AL (up 179.9 percent) and Augusta, GA (up 167.7 percent).

Among metro areas with a population of at least 1 million in 2021, the largest ROI increases from 2020 to 2021 were in Raleigh, NC (ROI up 80.6 percent); Oklahoma City, OK (up 64.4 percent); Virginia Beach, VA (up 62.6 percent); Washington, DC (up 60.2 percent) and Chicago, IL (up 59.4 percent).

The biggest decreases in investment returns in 2021 came in Kansas City, MO (ROI down 33.2 percent); Gulfport, MS (down 23.3 percent); Harrisburg, PA (down 22.8 percent); Columbus, GA (down 20.4 percent) and Myrtle Beach, SC (down 17.8 percent).

Aside from Kansas City, metro areas with a population of at least 1 million and declining profit margins in 2021 included Los Angeles, CA (down 11.9 percent); Houston, TX (down 11.5 percent); Cleveland, OH (down 11.4 percent) and Las Vegas, NC (down 10.4 percent).

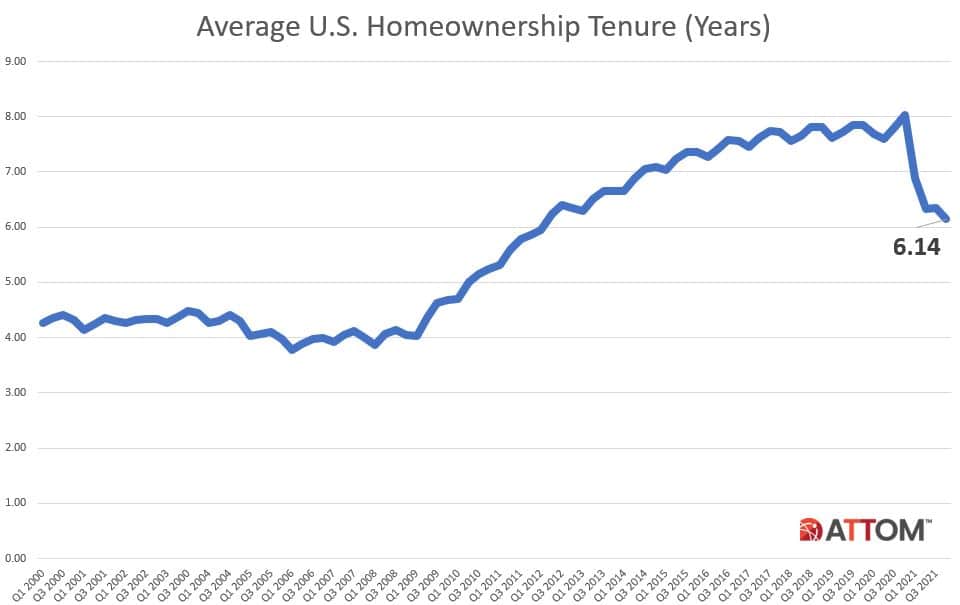

Homeownership tenure dips to nearly 10-year low

Homeowners in the U.S. who sold in the fourth quarter of 2021 had owned their homes an average of 6.14 years, down from 6.34 years in the previous quarter and from 8.03 years in the fourth quarter of 2020. The latest figure represented the shortest average home-seller tenure since the first quarter of 2012. Average seller tenures were down, year over year, in 102, or 95 percent, of the 107 metro areas with a population of at least 200,000 and sufficient data.

The biggest declines in average seller tenure from the fourth quarter of 2020 to the fourth quarter of 2021 were in Lakeland, FL (down 79 percent); Tucson, AZ (down 54 percent); Cleveland, OH (down 49 percent); Knoxville, TN (down 47 percent) and Torrington, CT (down 46 percent).

The longest tenures for home sellers in the fourth quarter of 2021 were in Bellingham, WA (10.03 years); Manchester, NH (9.87 years); Kahului-Wailuku, HI (9.71 years); Rockford, IL (9.27 years) and Lake Havasu City, AZ (8.33 years).

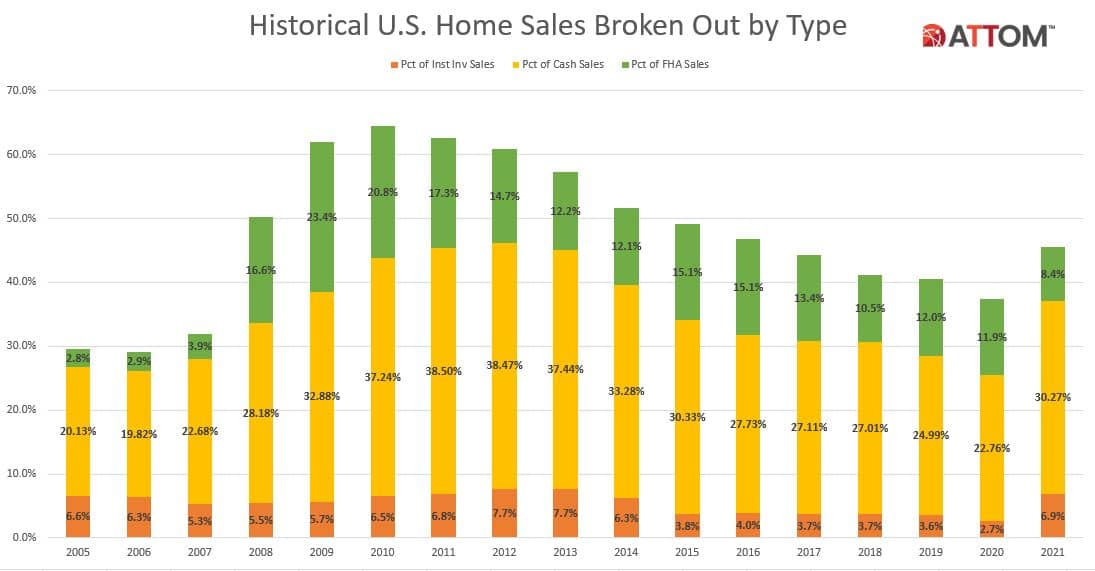

Cash sales hit six-year high in 2021

Nationwide, all-cash purchases accounted for 30.3 percent, or one of every three single-family house and condo sales in 2021 – the highest level since 2015. The latest figure was up from 22.8 percent in 2020 and from 25 percent in 2019, although still off the 38.5 percent peaks in 2011 and 2012.

Among 156 metropolitan statistical areas with a population of at least 200,000 and sufficient cash-sales data, those where cash sales represented the largest share of all transactions in 2021 were Detroit, MI (59.8 percent of sales); Macon, GA (54.1 percent); Flint, MI (53.7 percent); Buffalo, NY (52.1 percent) and Salisbury, MD (48.8 percent).

Lender-owned foreclosure purchases in U.S. at lowest level in at least 16 years

Foreclosure sales to lenders accounted for just 1.4 percent, or one of every 69 single-family home sales in 2021 – the lowest level since at least 2005. The 2021 figure was down from 3.5 percent of sales, or one in 29, in 2020 and 5.1 percent, or one in 20, in 2019.

States where lender-purchased (REO) foreclosure sales comprised the largest portion of total sales in 2021 were Illinois (3.5 percent of sales), Michigan (2.4 percent), Maryland (2.4 percent), New Jersey (2 percent) and West Virginia (2 percent).

Institutional investing at eight-year high

Institutional investors nationwide accounted for 6.9 percent, or one of every 14 single-family home and condo sales in 2021 in the U.S., the highest level since 2013. The latest figure was up from 2.7 percent in 2020 and 3.6 percent in 2019.

Among 190 metropolitan statistical areas with a population of at least 200,000 and sufficient institutional-investor sales data, those with the highest levels of institutional-investor transactions in 2021 were Atlanta, GA (19.5 percent of sales); Jacksonville, FL (18.8 percent); Charlotte, NC (18.6 percent); Memphis, TN (16.8 percent) and Phoenix, AZ (16.3 percent).

FHA sales at lowest level in 14 years

Nationwide, buyers using Federal Housing Administration (FHA) loans accounted for 8.4 percent, or one of every 12 single-family house and condo purchases in 2021. That was down from 11.9 percent in 2020 and from 12 percent in 2019 to the lowest point since 2007.

Among 190 metropolitan statistical areas with a population of at least 200,000 and sufficient FHA- buyer data in 2021, those with the highest share of purchases made with FHA loans were McAllen, TX (19.2 percent of sales); Hagerstown, MD (18.1 percent); Bakersfield, CA (17.9 percent); El Paso, TX (17.7 percent) and Yuma, AZ (17.7 percent).

To learn more about the data behind this article and what Attom Data Solutions has to offer, visit https://www.attomdata.com/.

Sign up to receive our stories in your inbox.

Data is changing the speed of business. Investors, Corporations, and Governments are buying new, differentiated data to gain visibility make better decisions. Don't fall behind. Let us help.

Sign up to receive our stories in your inbox.

Data is changing the speed of business. Investors, Corporations, and Governments are buying new, differentiated data to gain visibility make better decisions. Don't fall behind. Let us help.