Apparel was among the hardest-hit sectors during the pandemic, with potentially huge ramifications coming from this downturn. So, we decided to break down the early recovery and highlight three sectors that could surge in the coming months.

Apparel – Overall

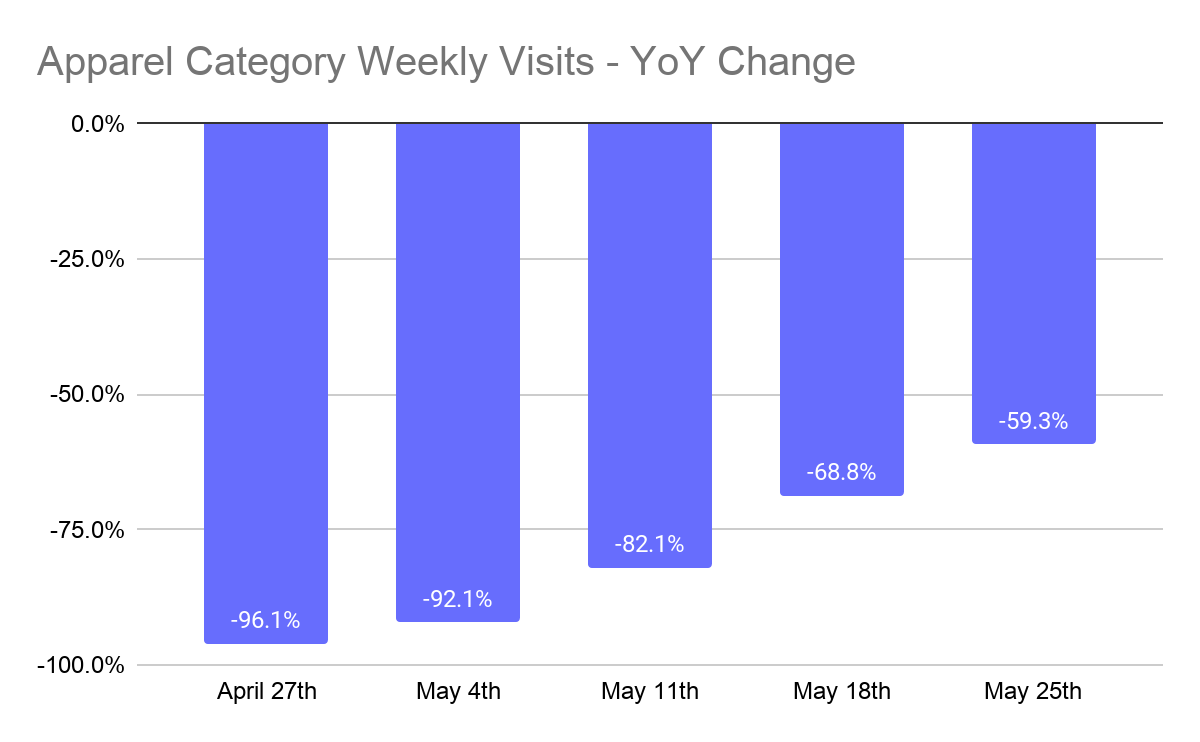

From a nationwide perspective, the apparel sector is clearly deep into the recovery process. The week of April 27th, the category was down 96.1% year over year in terms of weekly visits, yet this number had improved to being down 59.3% by the week of May 25th a month later.

The trend speaks to two critical factors. First, the recovery is taking place. Second, the process is going to take time, especially considering the staggered rollout of loosening restrictions across different states and brands.

Positioned to Thrive: Off-Price

In early March, we noted that few sectors were as well situated for the post-pandemic recovery as the off-price sector. Why? The sector had shown strong results heading into the pandemic, would enjoy a large quantity of inventory from a missed season, and had a value orientation well aligned for a period of economic uncertainty. And the early results from the recovery validate this thesis, so we’re doubling down.

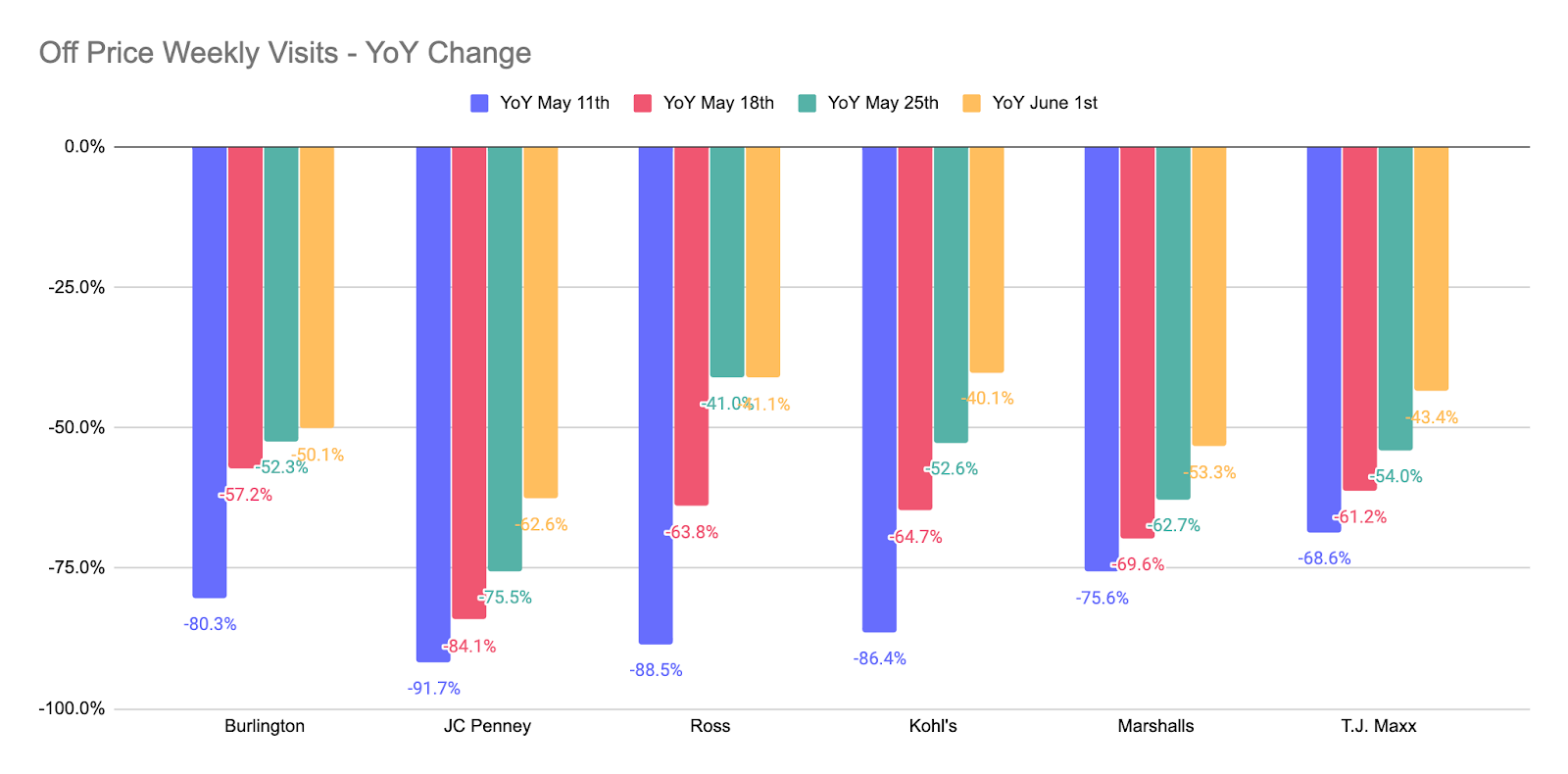

Analyzing six leading players in the space shows a surprisingly strong performance, considering the recovery only began in May and many states with high numbers of stores were still locked down throughout May and early June. Looking at the week of May 11th, 2020, the group averaged visits that were down 81.8% on the equivalent week in 2019. Yet, by the week of June 1st, just four weeks later, that average was down to a decline of just 48.4% year over year.

Kohl’s and Ross were pushing closest to ‘normal’ with visits down just 40.1% and 41.1% respectively, while JC Penney was the furthest away with visits down 62.6%

And the JC Penney decline is significant as well, with the brand announcing it would be closing over 120 stores nationwide. Looking at the period from January 2019 through June 2020, saw 41.8% of JC Penney shoppers also visiting a Kohls. Overlap with T.J. Maxx, Ross and Marshalls was 34.5%, 31.4% and 28.8%, respectively. Even Burlington, with the lowest overlap of the group, still saw 22.6% of JC Penney shoppers visit a Burlington location during that period.

So not only did the brands have a strong performance pre-pandemic and possess an offering uniquely suited for the coming period, but they also benefited from a thinning competitive landscape.

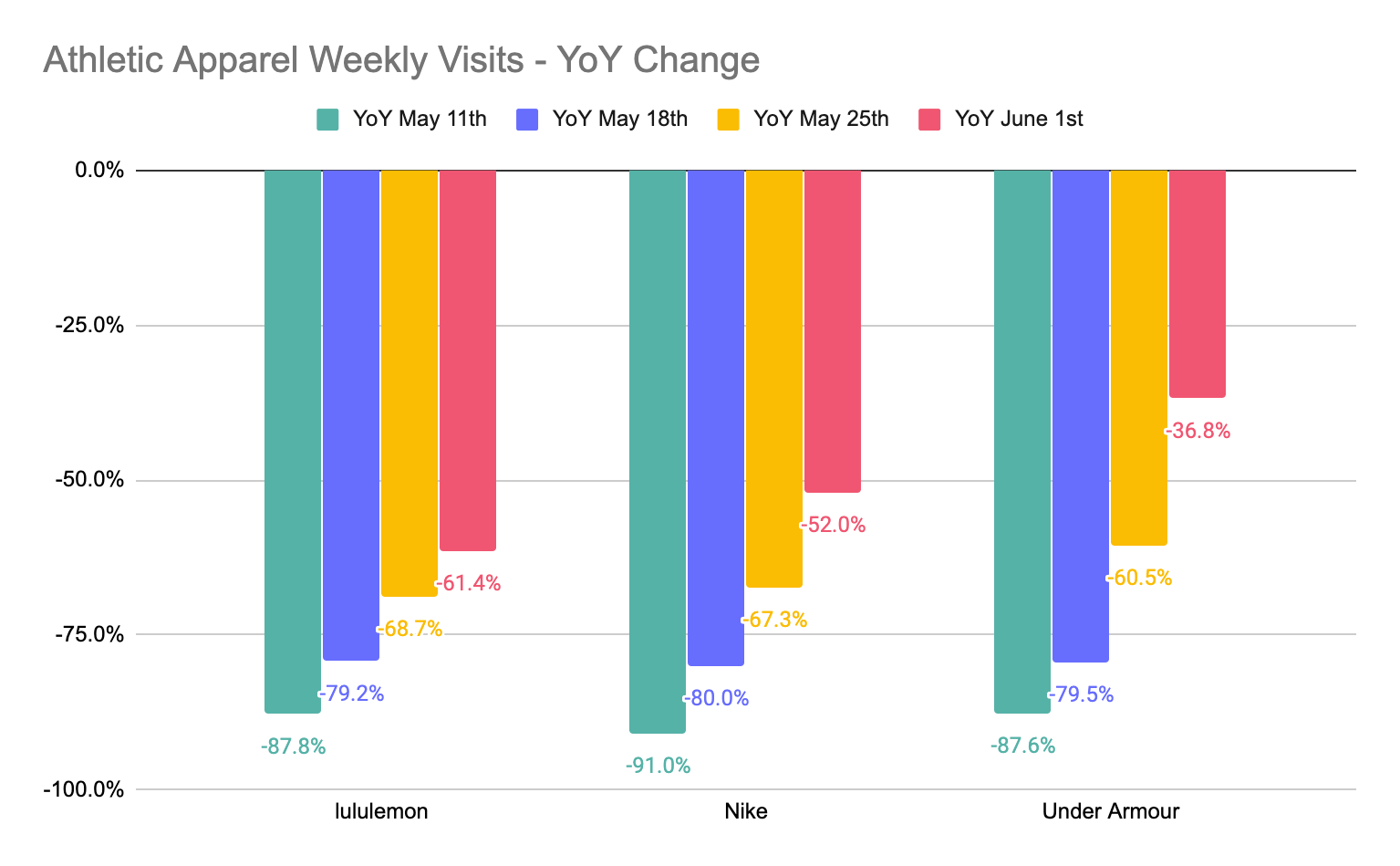

Can the Athleisure Trend Continue?

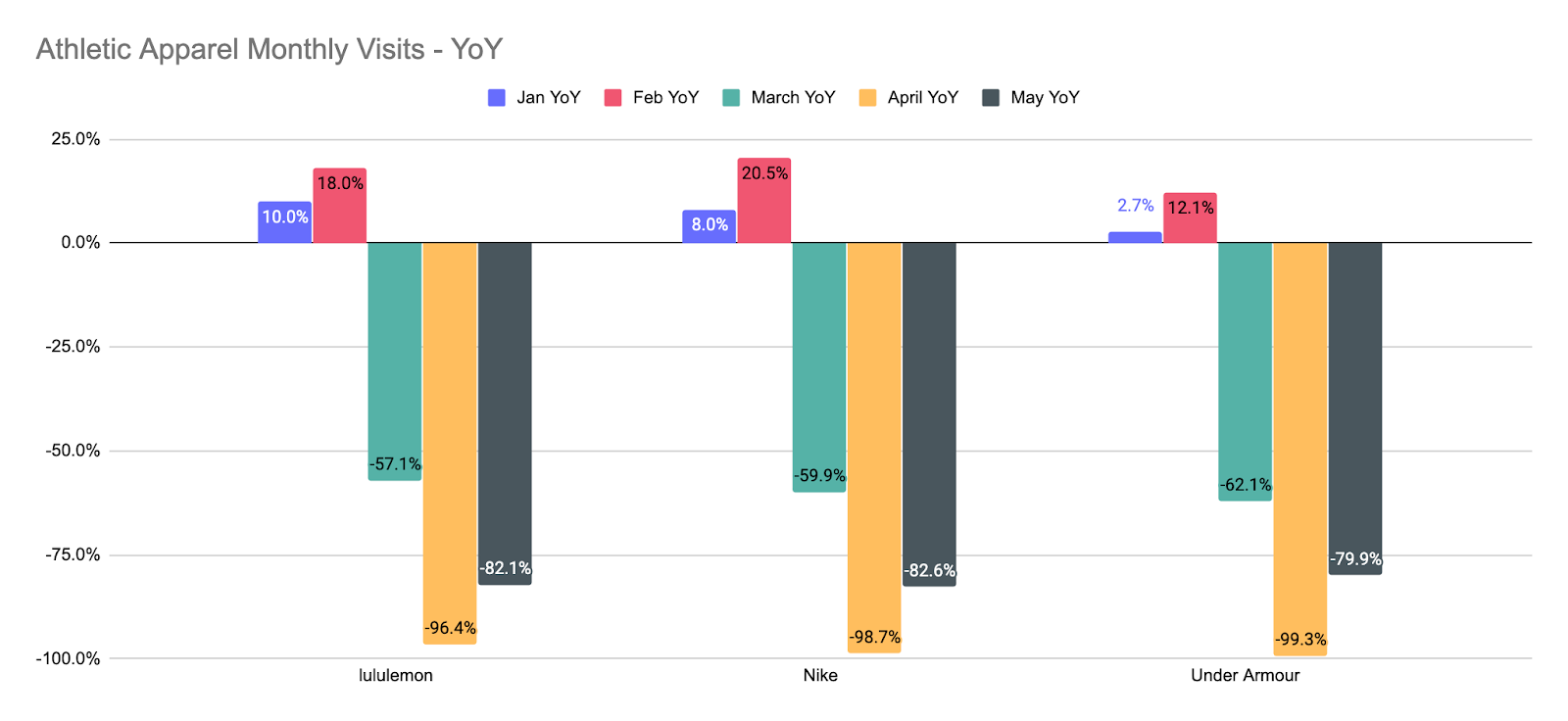

Another sector with a strong pre-pandemic buzz was the wider athletic apparel space. Led by an ever dominant Nike and a rising Lululemon, even the maligned Under Armour was seeing offline visit growth. And while a leap year in February contributed to strong numbers, the knowledge of impending store shutdowns was enough to drive late month surges as well.

And the brands are recovering. Nike and Under Armour have already put pre-pandemic numbers in their sights, while Lululemon trails slightly behind. Critically, Lululemon is impacted by its significant orientation towards major cities, among the hardest hit locations and the slowest to reopen. As cities reopen, expect the pace of return in this sector to pick up, enabling it to be among the first to truly ‘recover.’ Even more, the return in this space is especially interesting as it is centered around brands that focus on one line of products. This push for brand-owned stores could serve as a further push for other product and DTC companies to dive deeper into their owned offline strategy.

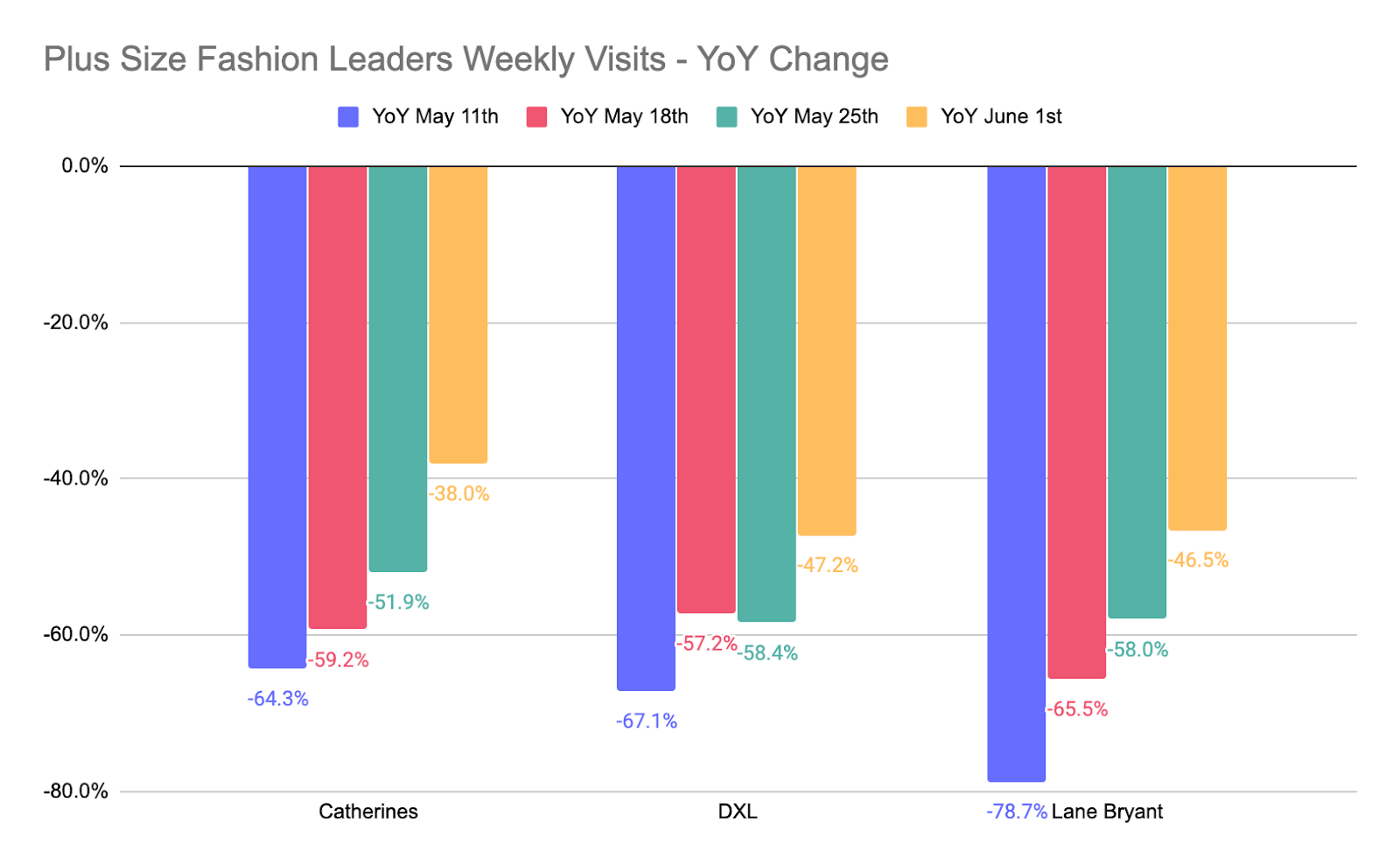

Plus-Sized Retail Grows Strong

Admittedly, we’ve had high hopes for the plus size apparel market for a while, and the more time passes, the more confidence we feel in the sector. And the data from the recovery has only reinforced the position. Catherines, Destination XL and Lane Bryant are all moving within 50% of their 2019 weekly visits numbers and the pace is increasing.

And there is no reason to believe this will tail off. The brands are able to offer a needed product to an underserved market that’s growing each year. The only question centers around the stability of Lane Bryant parent company, Ascena. Yet, should this situation be handled effectively, the umbrella brand could raise this sectors’ wave to renewed strength.

Lessons

Retail is recovering and so is apparel retail. While some sectors like the luxury market and department stores are seeing a slower return, others are rising quickly. Can the off-price, athleisure, and plus size sectors drive the next wave of apparel evolution?

To learn more about the data behind this article and what Placer has to offer, visit https://www.placer.ai/.

Sign up to receive our stories in your inbox.

Data is changing the speed of business. Investors, Corporations, and Governments are buying new, differentiated data to gain visibility make better decisions. Don't fall behind. Let us help.

Sign up to receive our stories in your inbox.

Data is changing the speed of business. Investors, Corporations, and Governments are buying new, differentiated data to gain visibility make better decisions. Don't fall behind. Let us help.