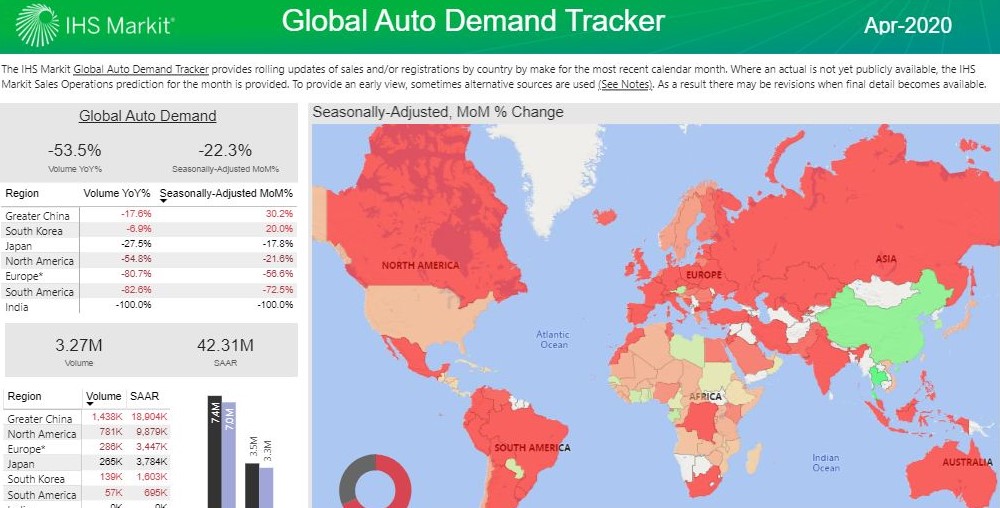

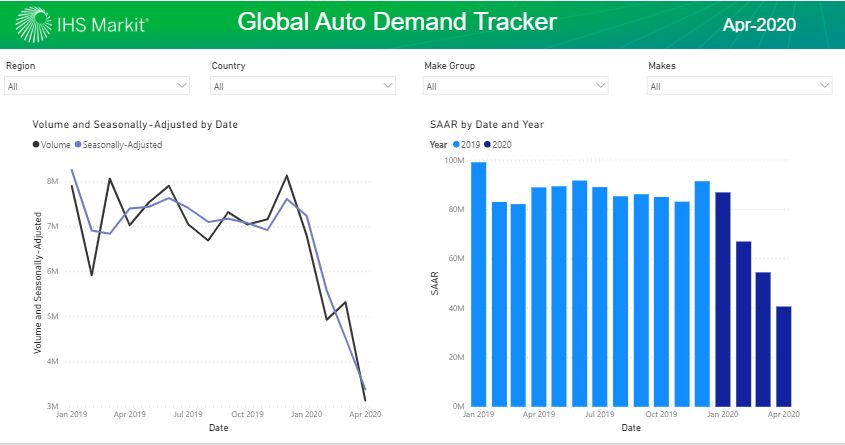

The month of May underlined the volatility expected in global demand as markets wrestled with the fallout from the COVID-19 virus pandemic and the resultant regional lockdown measures. The Seasonally Adjusted Annualised Rate (SAAR) has fallen to just 49 million units in April 2020, from 91 million units in December 2019. Click here to access the Global Auto Demand Tracker for free.

The US market has contracted to levels not seen since the 2007-2009 recession. Demand fell over 43% year on year (y/y) in April and has dropped 23.7% for the year to date as lockdown measures in many states brought vehicle sales to a standstill.

Europe has been even harder hit, with a 53% month-on-month (m/m) decline compared to March, which was itself already hit hard by lockdown measures.

Austria is the only country in West Europe showing early signs of recovery in April.

While Scandinavian countries appear to have been least affected, the United Kingdom is the hardest hit in terms of m/m decline.

Of the largest five auto markets, Germany has performed the ‘least worst’.

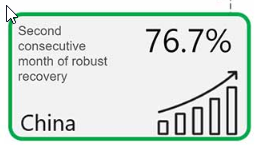

Although the pace of decline does not seem to be letting up yet, there are some indications of a tenuous recovery. China has enjoyed a resurgence in demand, recording an increase of over 76% compared to March.

To learn more about the data behind this article and what IHS Markit has to offer, visit https://ihsmarkit.com/index.html.

Sign up to receive our stories in your inbox.

Data is changing the speed of business. Investors, Corporations, and Governments are buying new, differentiated data to gain visibility make better decisions. Don't fall behind. Let us help.

Sign up to receive our stories in your inbox.

Data is changing the speed of business. Investors, Corporations, and Governments are buying new, differentiated data to gain visibility make better decisions. Don't fall behind. Let us help.