A common narrative during the COVID recovery period has been that indoor malls are facing a near existential crisis. To analyze the validity of this argument, we dove into ten of the top indoor malls and ten of the top outdoor centers to compare their relative performance in order to break down the pace of recovery and the potential for the coming months.

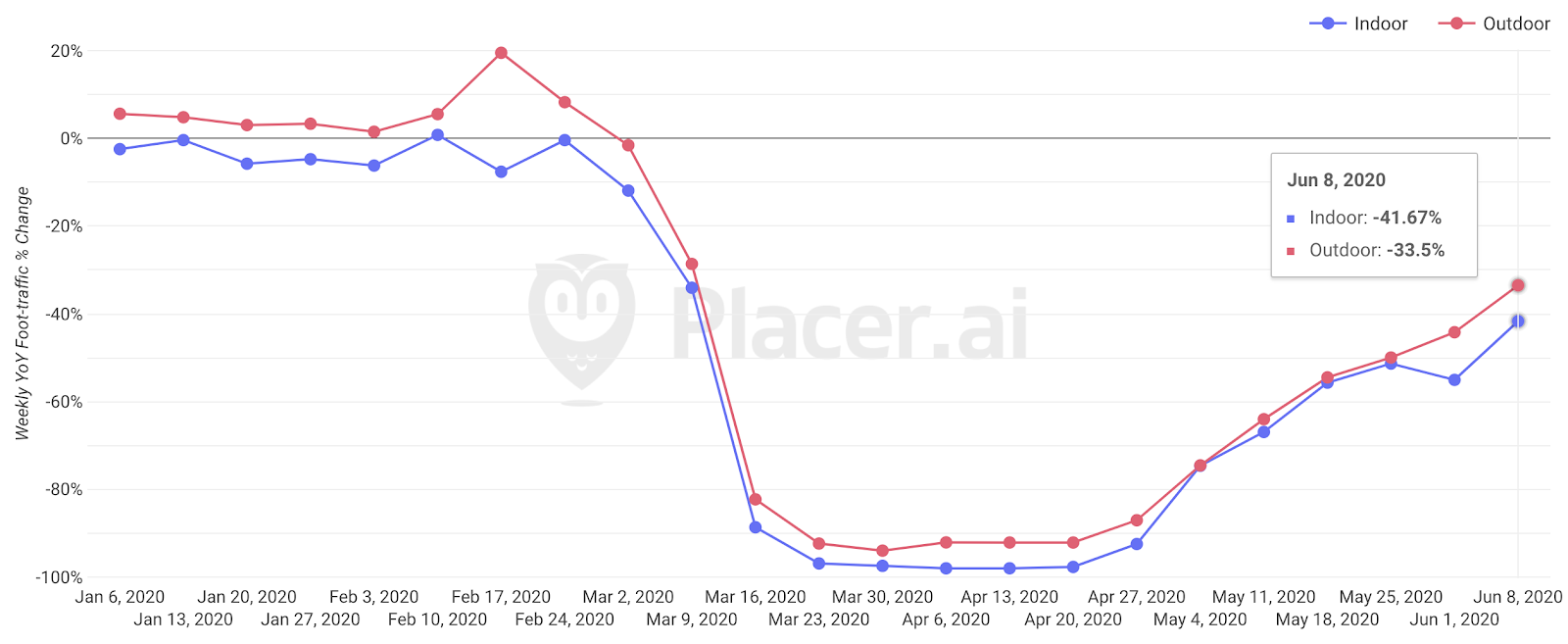

Visit Comparison

Obviously, indoor centers were harder hit than outdoor centers with visits having dropped to nothing by mid-March and continuing that way through late April. Outdoor centers benefitted from the essential retailers that were able to stay open, though in a very limited capacity.

Yet, the pace of recovery for indoor centers has been far better than many expected. By the week of June 8th, visits to the centers analyzed were down 41.7% year-over-year compared to being down 74.6% the week of May 4th, just a little over a month earlier. And all this with malls in states like New York and California still closed during this period.

Outdoor shopping centers were performing better with a decrease of just 33.5% the week of June 8th, compared to being down 74.5% the week of May 4th.

Engagement Metrics

Yet, visits aren’t the only critical measure of success. Indoor malls gain strength from the magnitude of visits they are able to generate. Visitors are generally willing to travel longer distances to a mall with the promise of having an experience that goes beyond just shopping. And if you’re willing to spend a long amount of time in a mall, the likelihood of multiple purchases, whether food, entertainment, apparel, or home goods, is significantly increased.

The key measure of this magnitude is the visit duration, and while visits rates are typically longer in indoor centers, they are also returning closer to normal levels faster.

Comparing visit durations the week of June 8th, with the week of March 9th – the last pre-pandemic week – shows indoor centers down just 9.2% while outdoor centers were down 15.8%. The latter is likely being impacted by shifts in consumer behavior that focus on more ‘mission-driven’ shopping that privileged longer visits to retailers with a wider product range at the expense of more visits to a number of locations – and ultimately, a longer overall visit. However, this too could bounce back soon.

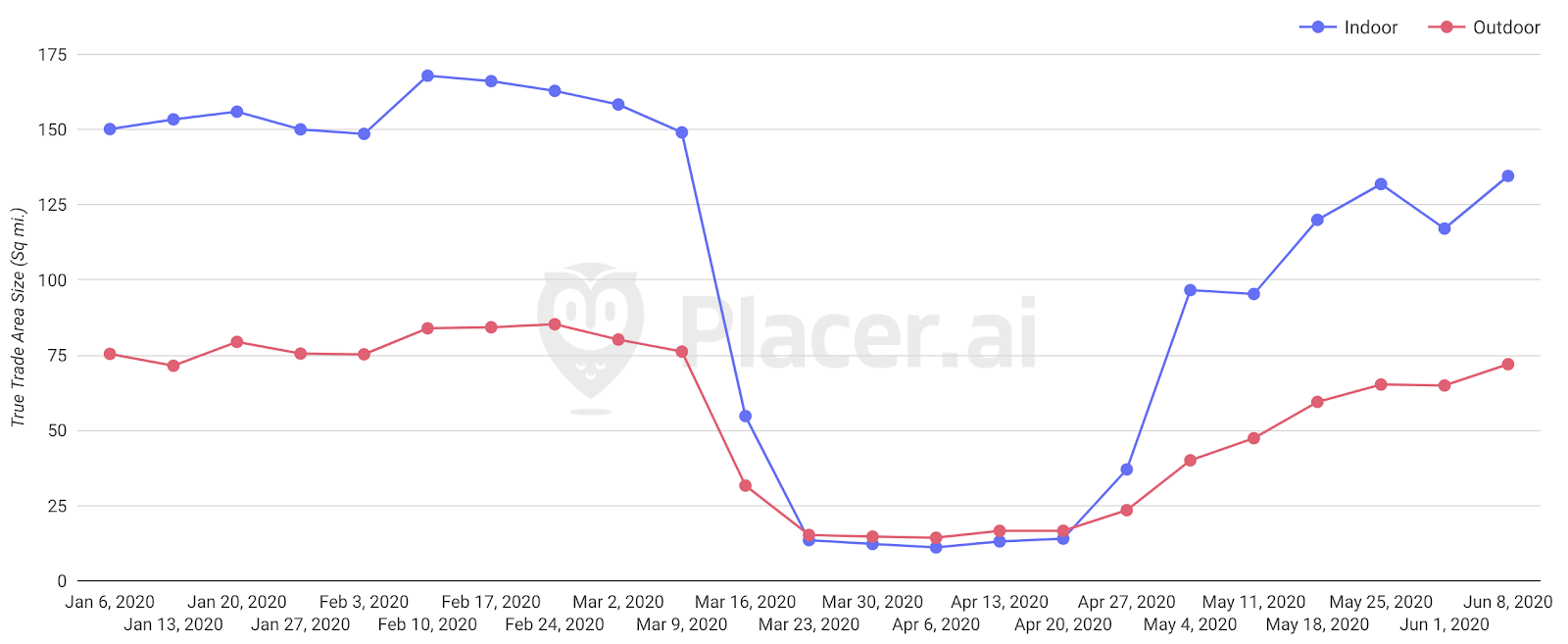

Reach

A third factor that can provide critical insights is the size of the True Trade Area these centers pull from. The ‘reach’ of a center helps define its addressable market, and the larger the True Trade Area, the larger a population a specific mall can pull from, helping to bring consistency to their visit rates. With restricted hours and only certain stores open, the ‘pull’ for indoor centers was limited during the early days of their reopenings, impacting the willingness of shoppers to travel farther distances.

Yet, here too, the size of these True Trade Areas are returning to ‘normal’. While the average True Trade Area size for indoor centers was still down 9.7% the week of June 4th compared to the week of March 9th, this reflected a True Trade Area size that was 41.1% larger than it was the week of May 11th.

Conclusions and Key Takeaways

Yes, the wider mall sector has been undergoing a significant change over the last few years. However, this does not mean that the fundamental value of the mall is decreasing. Rather, it is more likely that some of the means of driving success are changing, but this was a process already taking place long before the pandemic

Looking at these indexes of top centers shows that leading malls are recovering at a healthy pace, even with all of the uncertainty surrounding performance and the myriad of obstacles in their path. Does it guarantee success for all? No. Does it show that opportunities for players in this sector and demand from consumers still clearly exist? Absolutely.

On the other hand, it is difficult to argue with the newfound value that outdoor centers have received. Their ability to anchor around essential retail and the comfort that they can provide with a less enclosed experience should provide them strength so long as concerns of a second wave persist. Additionally, their orientation towards well-positioned retailers like off-price apparel, traditional grocers, home improvement brands, and more all help strengthen their current status.

However, the likeliest scenario is not one of dominance by indoor or outdoor centers, but an evolving landscape of retailers and tenants that look to take advantage of the unique benefits of either option. In fact, it’s very likely that an increasing number of brands will look to capitalize on the benefits of the forum they don’t currently dominate as a means of adding value and diversifying their reach. The key moving forward will be identifying the ideal way of differentiating and providing mechanisms to boost the specific strengths that each one offers.

To learn more about the data behind this article and what Placer has to offer, visit https://www.placer.ai/.

Sign up to receive our stories in your inbox.

Data is changing the speed of business. Investors, Corporations, and Governments are buying new, differentiated data to gain visibility make better decisions. Don't fall behind. Let us help.

Sign up to receive our stories in your inbox.

Data is changing the speed of business. Investors, Corporations, and Governments are buying new, differentiated data to gain visibility make better decisions. Don't fall behind. Let us help.