2020 was a uniquely challenging year for the world of offline retail, but it also presented an opportunity to truly appreciate its value. The resilience of consumer demand and the ongoing ability of many brands to continue driving engagement and interest, even amid the pandemic, served as a huge testament to the retail landscape’s strength.

We kicked off 2020, without knowledge of the impending COVID storm, by acknowledging six brands we felt would show tremendous strength over the course of the year. Then, as the retail recovery was getting rolling, we dove into six others that would perform well in the second half of the year.

The performance of those brands, even during the pandemic, validated our perspective. Target, Ulta, and CVS were among the year’s best performers irrespective of sector. Chick-fil-A and Chipotle continued to show strength in the restaurant space, and Bed Bath & Beyond ended up widely appreciated for its impressive turnaround even as many had expected the opposite to start the year.

And while we’d happily put any of those onto our 2021 list, the one rule we’ve set is that a retailer cannot be on the list two years running. This means an all-new group of brands we expect to have exceptional 2021 performances, who were not included in either of our 2020 lists.

So, here are our 2021 winners.

Kohl’s

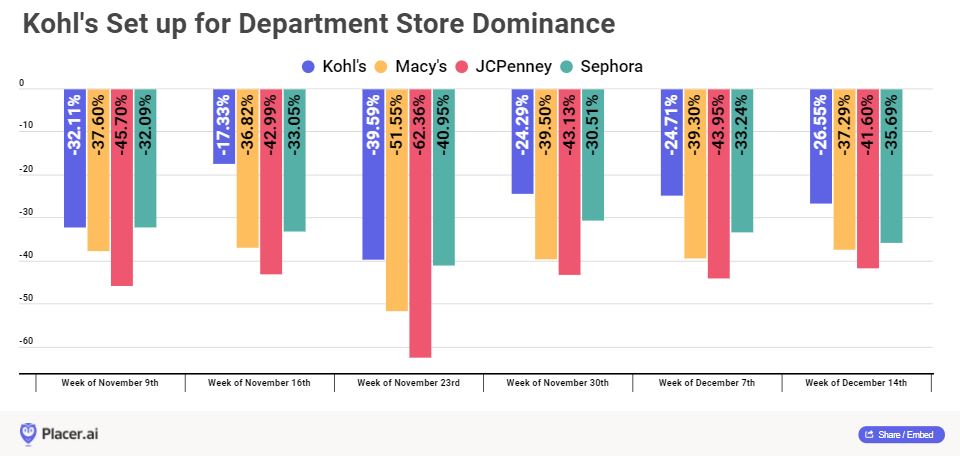

Kohl’s is one of the hardest apparel players to categorize properly. While it is a department store leader, the retailer has elements of off-price appeal and tends to more closely mimic the traffic patterns of those players. And this combination may be the brand’s magic mix. Looking at weekly visits year over year since the week of November 9th, shows Kohl’s visits down an average of 27.4%. While this is less than ideal, it is far better than Macy’s or JCPenney who saw weekly visits down an average of 40.3% and 46.6% respectively.

Importantly, this is less a referendum against mall-based department stores, whom we also expect to see a significant rebound – than a testament to some very impressive traits for Kohl’s. The outdoor advantage and focus on value is clearly serving it well, but it is not resting on this short term boost.

Instead, Kohl’s is making bold moves with a forward looking outlook. Serving as a return location for Amazon can boost store traffic while a newly announced partnership with Sephora could help the brand tap into an entirely new audience. Kohl’s should be very well positioned for 2021 with outdoor locations still serving as a benefit and a value orientation providing a boost. But the willingness to leverage its existing strength, especially relative to the wider apparel sector, to drive new initiatives should make 2021 a kick-off to a string of strong years to come.

Traditional Grocers – Albertsons, Kroger, Publix

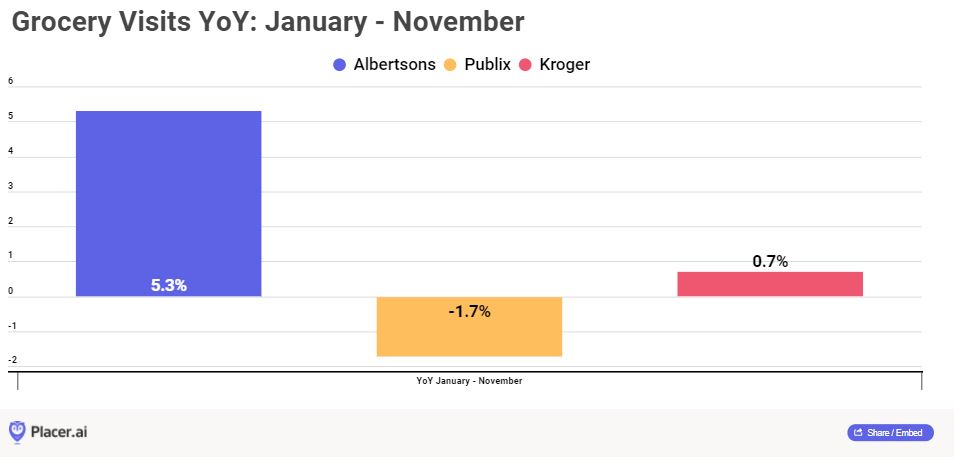

It was exceptionally difficult to choose between these three, so we decided to group them together as a ‘traditional’ grocery category. Why? All three have already had a huge year with visits from January through November up 5.3% for Albertsons and 0.7% for Kroger with Publix down just 1.7% even though it operated heavily in Florida, one of the hardest hit states. Yet, this is only a small piece of the puzzle.

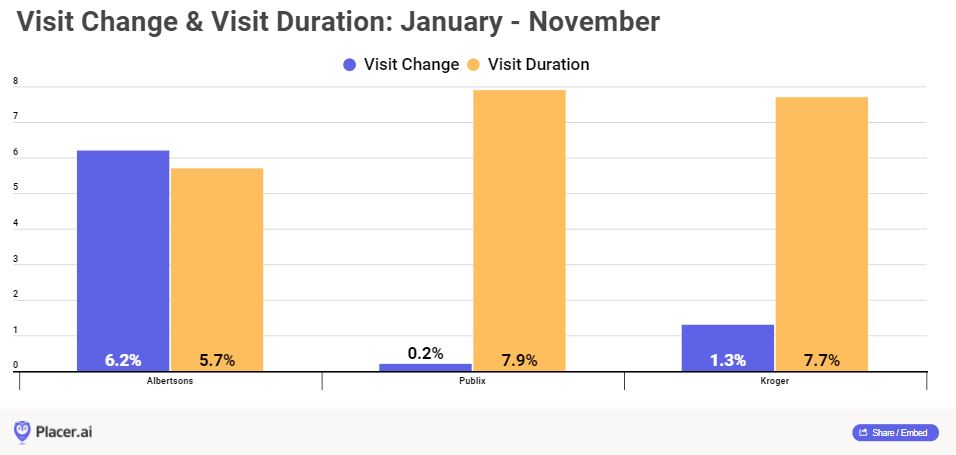

While their respective overall visits were impressive enough, looking at the period between June and November saw visits up for all three year over year. And the situation was even better because the pace of visit growth actually increased as the year went on. But not only did these brands see more visits, they saw more valuable visits. Visit duration for the three rose an average of 7.1% for the period from June through November year over year, indicating jumps in basket size. Publix led the way with a 7.9% increase, while Kroger and Albertsons saw jumps of 7.7% and 5.7% respectively. These are huge leaps, and when taken alongside visit growth, present a powerful picture. Not only are these brands seeing more visitors, but they are seeing those visitors spend more time at the locations, even while visits-per-visitor numbers decline for the same period year over year.

With periods of economic uncertainty often privileging grocers for their ability to provide meal-time value, and mission-driven shopping likely to linger at least through Q1 2021, it is hard to see any of these brands not producing very effective performance in the coming year.

Home Goods Risers – At Home, HomeGoods, Tractor Supply

Another sector, another argument on the most deserving player to represent the category – so another excuse to include all three. Critically, we couldn’t include Home Depot or Lowe’s following their spot in the 2020 Winners: Pandemic Update. This sector benefits from a surge in focus on the home that is likely to continue as wider economic uncertainty continues to make home upgrades a smarter decision than new homes entirely.

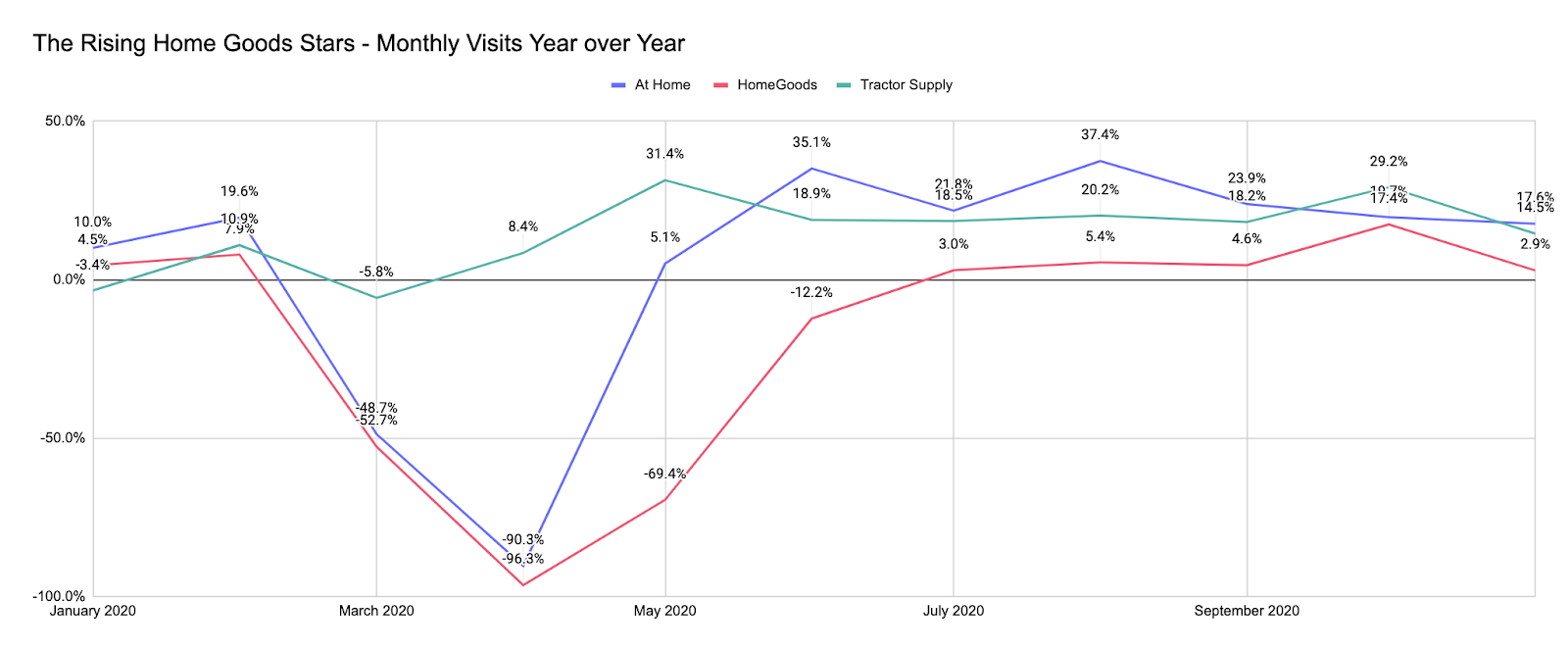

At Home deserves all the credit for a year that saw an average year-over-year increase of 4.6% even though visits completely disappeared in April. In fact, from June through November, the brand saw monthly visits that were 25.9% higher on average than they were the same months in 2019 – data that validates claims from the brand that a threefold increase in stores could be necessary.

HomeGoods hits the list for its unique combination of strong performance and value orientation, something that should position the brand uniquely well in the coming year. HomeGoods saw an average 6.7% year-over-year increase in traffic from July through November after starting off the year with 6.2% average year-over-year growth in January and February. This ability to start and finish with strength makes the chain uniquely well-situated for whatever the year may bring.

And finally, Tractor Supply earns its spot not just for a year where monthly visits were up an average of 14.6% from January through November, but because of the turnaround it marked. While many of 2020’s strongest performers saw strong performances to kick off the year, Tractor Supply began with January visits down 3.4% year over year. Yet, since June, no month has seen year-over-year growth lower than 14% giving a strong indication that this surge has real staying power.

Planet Fitness

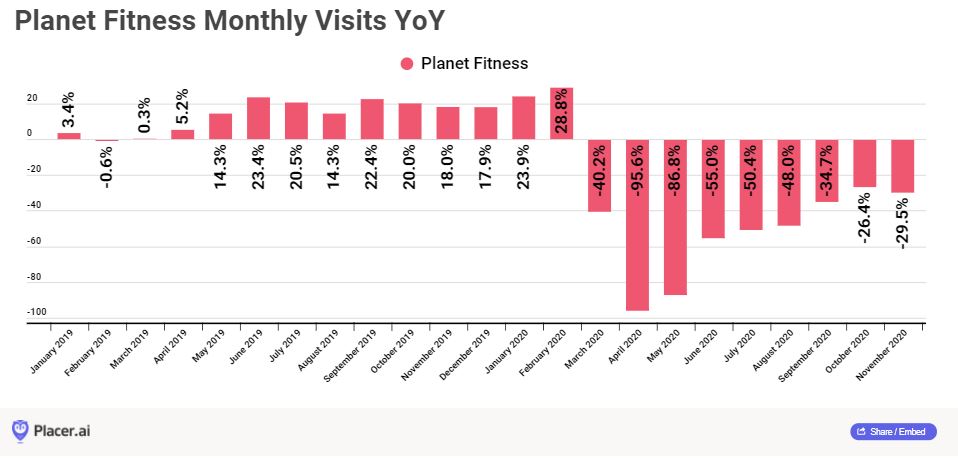

In 2019, Planet Fitness monthly visits were up over 13% year over year on average. This included a slower start to the year, likely driven by the strength of Q1 for the fitness sector. Yet, 2020 started even stronger with visits up 23.9% and 28.8% year over year in January and February, setting up a torrid pace that was sadly but obviously upended by COVID. However, visits have been tracking steadily towards 2019 levels with October and November seeing visits down 26.4% and 29.5% respectively – compared to 34.7% in September – even with November suffering under a surge of COVID cases nationwide.

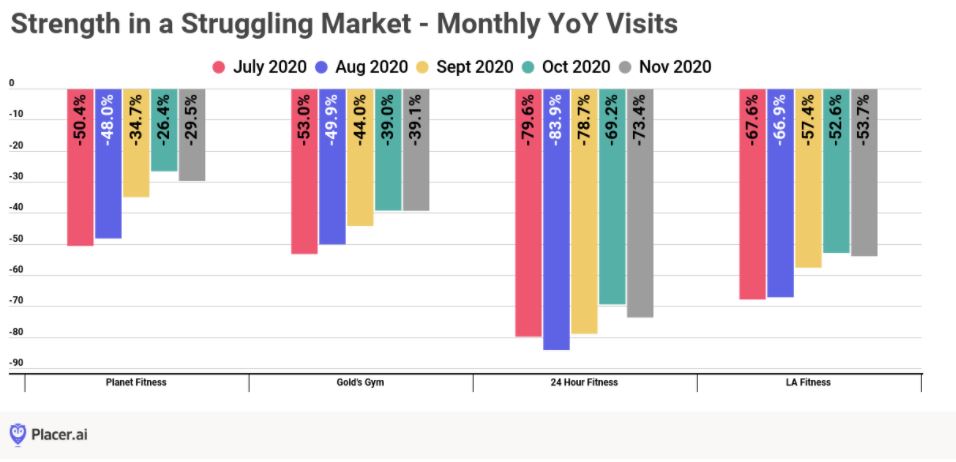

And the brand’s relative performance has been even more impressive. While other key players in the space have seen visits down as much as 70% year over year in November, Planet Fitness was within 30% of ‘normalcy’. The pre-COVID strength and strong relative performance within the sector all indicate that if a fitness chain rises above the noise in 2021, it is likely to be Planet Fitness.

But even more, the sector does seem to be well positioned – even amid the difficult 2020 environment. Health and wellness have become huge issues, fitness could see a surge in renewed ‘first time demand’, and omnichannel approaches in the space could help chains like this sustain visitors with a more holistic approach. All told, expect Planet Fitness to lead the gym sector with an impressive rebound in 2021.

Malls

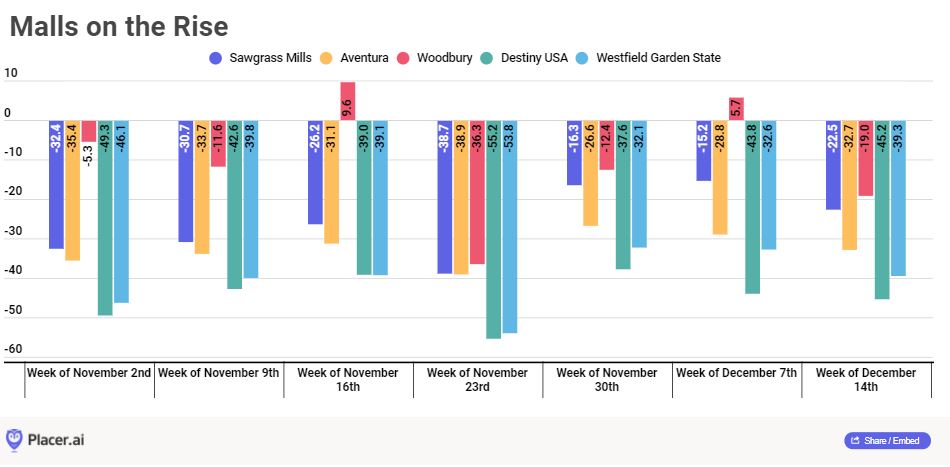

If you designed a test in a lab to put indoor malls in the most difficult possible situation, it wouldn’t look all that dissimilar from what 2020 actually produced. Yet, even in that environment, top tier malls have consistently shown that when visitors are able to come shop, they will. Looking at several top tier malls shows that after seeing visits on Black Friday week decline by 49.7% on average, they were down only 29.9% on the week of Super Saturday.

And there are lots of factors working in the favor of malls in 2021. Firstly, people miss them. When shopping was open, visitors came back and if COVID comes under control in early 2021, the impact on malls could be massive. Secondly, the retail mix inside of them is changing. This is creating more diversity in malls, and therefore, more complementary interactions between malls that could create a bigger overall pie. Thirdly, it feels like mall owners are ready to get aggressive and creative. From Simon buying JCPenney to major renovations at top malls bringing more office and residential into the mix, to the aforementioned changes to tenant mix – COVID may actually bring a long term positive to the sector.

By forcing adaptation and evolution, malls could end up stronger in the coming years than they were before. And while top tier malls were actually up year over year in January and February of 2020, even struggling malls could benefit strongly from a ‘redefinition’. If this trend starts to show signs of taking place, expect a powerful surge for the wider space.

Dollar General

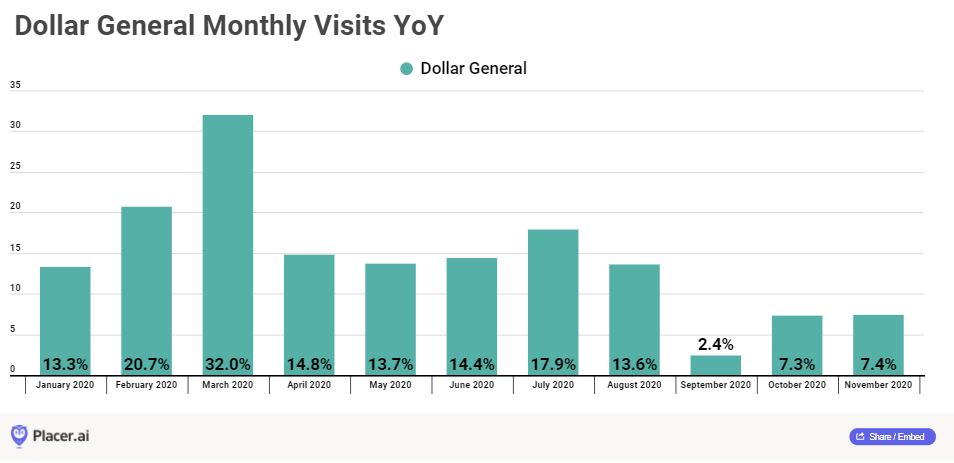

Our final winner for 2021 is Dollar General. In 2020, Dollar General saw 2.9% more visits than in 2019, and that’s without counting December 2020 at all. Looking at January through November only, Dollar General saw visits increase by 14.0% year over year.

And the trends driving this added success aren’t changing, and may actually become more significant. Firstly, Dollar General is not afraid to expand offline and has even moved upmarket with its new Popshelf concept. Second, the brand has a huge audience that may actually be expanding with average household income metrics increasing as more audiences look to their value offering. Finally, even when COVID goes away, the economic uncertainty it caused will linger far longer, putting an even greater emphasis on the value Dollar General can provide. In the end, it’s hard to see anything but success for the brand in 2021.

To learn more about the data behind this article and what Placer has to offer, visit https://www.placer.ai/.

Sign up to receive our stories in your inbox.

Data is changing the speed of business. Investors, Corporations, and Governments are buying new, differentiated data to gain visibility make better decisions. Don't fall behind. Let us help.

Sign up to receive our stories in your inbox.

Data is changing the speed of business. Investors, Corporations, and Governments are buying new, differentiated data to gain visibility make better decisions. Don't fall behind. Let us help.