In our Q3 Quarterly Index, we analyzed a wide array of brands in several major retail categories including apparel, grocery, fitness, home improvement, and superstores to bring you the latest insights and identify trends shaping retail right now.

Apparel Yo2Y Visit Gap Almost Closed

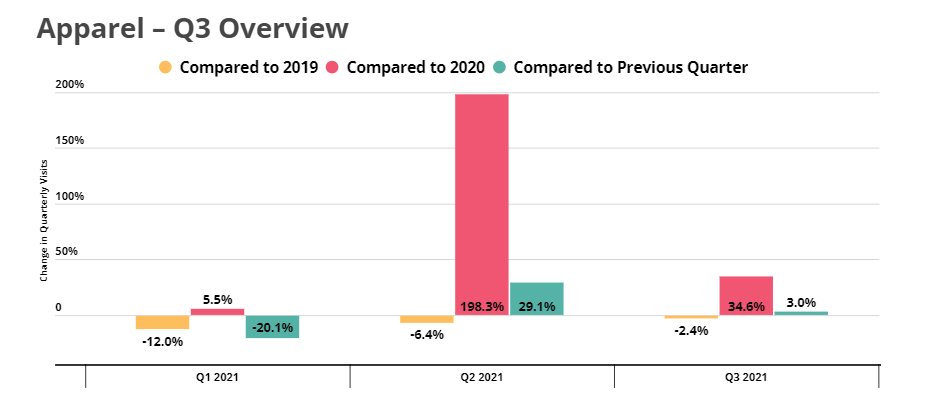

The apparel sector was hit hard by the pandemic, but foot traffic data shows that the category is bouncing back. Despite renewed COVID concerns, apparel visits grew this quarter, with foot traffic to apparel brands 3.0% higher, on average, than in Q2 2021. And year-over-two-year foot traffic data seems to confirm that apparel is on its way to a full recovery, with overall visits in Q3 2021 only 2.4% lower than they were in Q3 2019.

And apparel visits may well get a major boost next quarter, with the holiday season giving consumers the opportunity to shop for new, festive clothing.

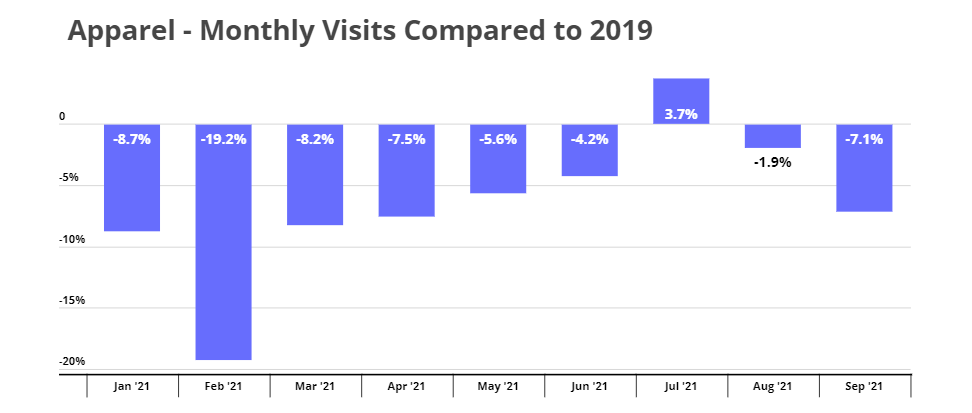

But the quarterly average belies a more complex reality, with year-over-two-year apparel visits rising by 3.7% in July only to fall by 1.9% August and 7.1% in September amidst rising COVID concerns.

Still, the sector’s ability to almost close the quarterly visit gap – especially given the particularly strong 2019 Back-to-School season to which current visit numbers are being compared – means that there is still a strong demand for offline apparel shopping. As the current COVID wave continues to recede, a new wave of pent-up demand may well fuel a fuller apparel recovery in Q4.

Off-Price and Athletic Wear Still Strong

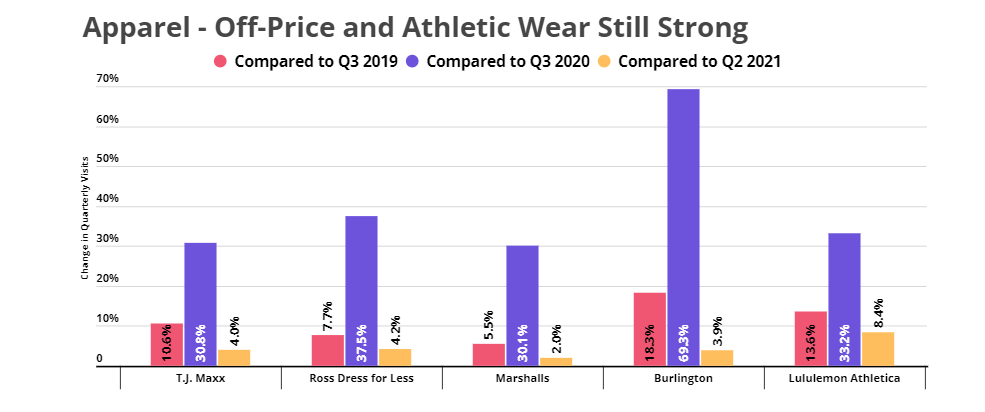

Two apparel categories in particular are buoying the wider apparel category: off-price and athletic wear. Ross Dress for Less, Burlington, Lululemon Athletica, and others showed strong year-over-two-year gains in Q3, with Ross, Burlington, and Lululemon seeing year-over-two-year visit increases of 7.7%, 18.3%, and 13.6%, respectively.

The offline success of athletic and athleisure brands seems to reflect an overall increase in demand for comfortable clothes and workout gear. And off-price’s success comes in spite of – and perhaps due to – the category leaders’ more limited focus on e-commerce channels, indicating that apparel retailers with little to no e-commerce presence can still be relevant in 2021.

As the return to the office continues and socializing returns, the demand for new clothes may rise even further – positioning for success the apparel players that weathered the COVID storm.

To learn more about the data behind this article and what Placer has to offer, visit https://www.placer.ai/.

Sign up to receive our stories in your inbox.

Data is changing the speed of business. Investors, Corporations, and Governments are buying new, differentiated data to gain visibility make better decisions. Don't fall behind. Let us help.

Sign up to receive our stories in your inbox.

Data is changing the speed of business. Investors, Corporations, and Governments are buying new, differentiated data to gain visibility make better decisions. Don't fall behind. Let us help.