In April, US tight oil completions dropped to the lowest level of activity in any single month since 2016. When plummeting demand due to COVID-19 and increased OPEC output drove WTI prices to historic lows in March, operators reacted immediately, cutting well completion activity to bare minimums in every basin except the Delaware. Though drilling activity was also reduced, operators kept enough drilling rigs running to drive a spike in DUC inventories to the highest level in four years. With this new backlog of uncompleted wells and WTI prices climbing toward $40/b, US producers are poised for a comeback.

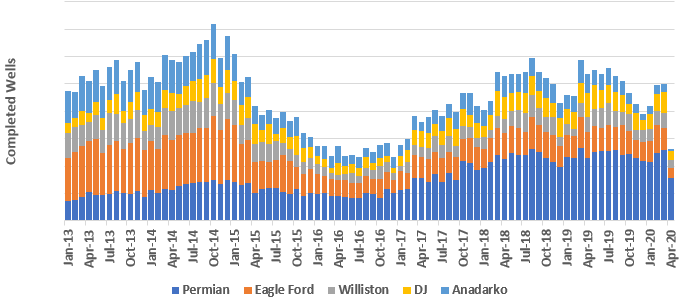

Well completions fall 48% M/M in April as historically low prices drive operators to cut

Figure 1. Well completions fall 48% M/M in April as historically low prices drive operators to cut (Source: Kayrros)

When Saudi Arabia announced that it would increase output in March, even as COVID-19 brought the global economy to a standstill, US tight oil operators did not hesitate to act. In 2014, the last time OPEC made this kind of market share gambit, it took US producers a full year to cut well completions by 50%. (Figure 1) In 2020, it only took a month. US operators have made efforts over the past two years to prove that they were listening to their investors, transitioning from a culture of “growth at any cost” to one focused on returns and cash flow, but this reaction may be the strongest proof yet of that transition.

US operators cut activity across all the major tight oil basins, but some were more resilient than others. Completions in the Delaware dropped 32% M/M, and 45% M/M in both the Midland and Williston Basins. The decline was most dramatic in the Rockies and in the Anadarko. DJ operators cut well completions by 58% in April. It was clear from the start of the year that the Anadarko Basin was out of fashion, with completions down 62% Y/Y in March, but Oklahoma operators cut even further in April, down 85% M/M and 94% Y/Y.

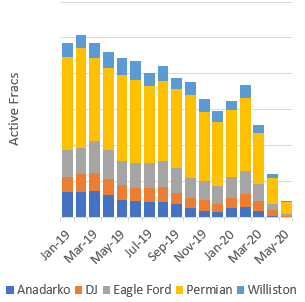

The spectacular decline in well completions is not done yet. Frac activity Kayrros observed in March and early April drove April completions, but active frac spreads continued to decline through April and May, bottoming out in the last week of April, a nearly 80% drop from the last week of March. (Figure 3) We may have seen the end of frac activity declines, however. To some extent that is because activity cannot get any lower in most basins. Only one frac crew is active in each of the Williston, the DJ, and the Anadarko Basins in May.

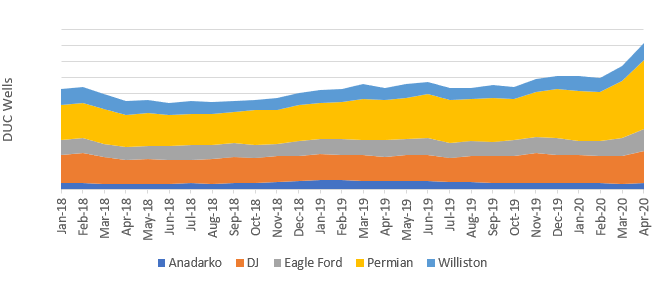

DUC inventories climb dramatically as drilling activity outpaces well completions

Figure 2. Active drilling rigs in the five largest tight oil basins; Figure 3. Active frac spreads in the five largest tight oil basins (Source: Kayrros)

Figure 4. Total active drilling rigs and active frac fleets (% change, normalized to January 3 2020) (Source: Kayrros)

Though operators have cut activity to the bone across the US, the drop in active fracs was much more dramatic than the drop in active rigs. While active fracs have dropped 86% since reaching their 2020 peak in February, active rigs have fallen only 69% over the same period. (Figure 4) This imbalance in activity levels has led to a 32% increase in drilled, uncompleted (DUC) well inventory in March and April, the fastest increase since the beginning of Kayrros data and likely since the beginning of the shale revolution. (Figure 5) Though the gap between drilling and completion activity has narrowed in May, with operators cutting more rigs and active fracs at minimums, DUC inventory continued to increase in May. Operators are now poised, as WTI prices climb toward $40, to resume frac activity and begin drawing down on that inventory. On a sunk cost basis, the vast majority of these DUCs are already economic — at least on paper — to complete today. However, before operators begin to resume completing wells, they will need to resume production on the wells they shut in when prices fell to unprecedented lows back in April. Kayrros is already seeing evidence of that in West Texas crude oil inventory levels.

After operators began shutting in wells in April, Kayrros saw crude oil inventories in West Texas fall to the lowest level since at least 2016, the beginning of the history of satellite measurement of crude storage. Since reaching lows in late May, West Texas stocks have climbed to 6-month highs. (Figure 6) Kayrros began hearing anecdotes from the field that operators were bringing wells back online in early June. This jump in inventories suggest they may have started even earlier. With WTI prices were safely above $30/b, operators decided it was time to begin turning wells back online.

Figure 5. Kayrros Caribbean crude oil storage capacity utilization (Source: Kayrros)

With shut-in wells being turned back online and refinery runs still 4MM b/d below seasonal norms, US inventories have once again resumed builds. Even with the OPEC decision to maintain production cuts and other non-OPEC production still declining, this increase in US production is likely to put pressure on crude oil prices in the short term, even as demand continues to recover. This increase in US supply will be short-lived, however. Without a substantial increase in drilling and completion activity, US crude production will soon resume declines. Assuming global demand recovers to normal levels — admittedly a significant assumption with COVID-19 still spreading in many parts of the world — even increased OPEC output will not be enough to balance the oil market. The crude price curve will shift to backwardation as inventories resume draws and US producers will be called back to work to help fill the global decline wedge.

To learn more about the data behind this article and what Kayrros has to offer, visit https://www.kayrros.com/.

Sign up to receive our stories in your inbox.

Data is changing the speed of business. Investors, Corporations, and Governments are buying new, differentiated data to gain visibility make better decisions. Don't fall behind. Let us help.

Sign up to receive our stories in your inbox.

Data is changing the speed of business. Investors, Corporations, and Governments are buying new, differentiated data to gain visibility make better decisions. Don't fall behind. Let us help.