When we last looked at grocery shopping behavior, we noted a few key changes. Visits were shifting from weekends to weekdays and from evenings to mornings. And seemingly, these shifts were driving more time in store, along with a significant shift in visit duration for top brands.

But now with the recovery in full swing, we decided to check back in on key behavioral patterns in grocery to see which trends have had staying power and which have returned to “normalcy”.

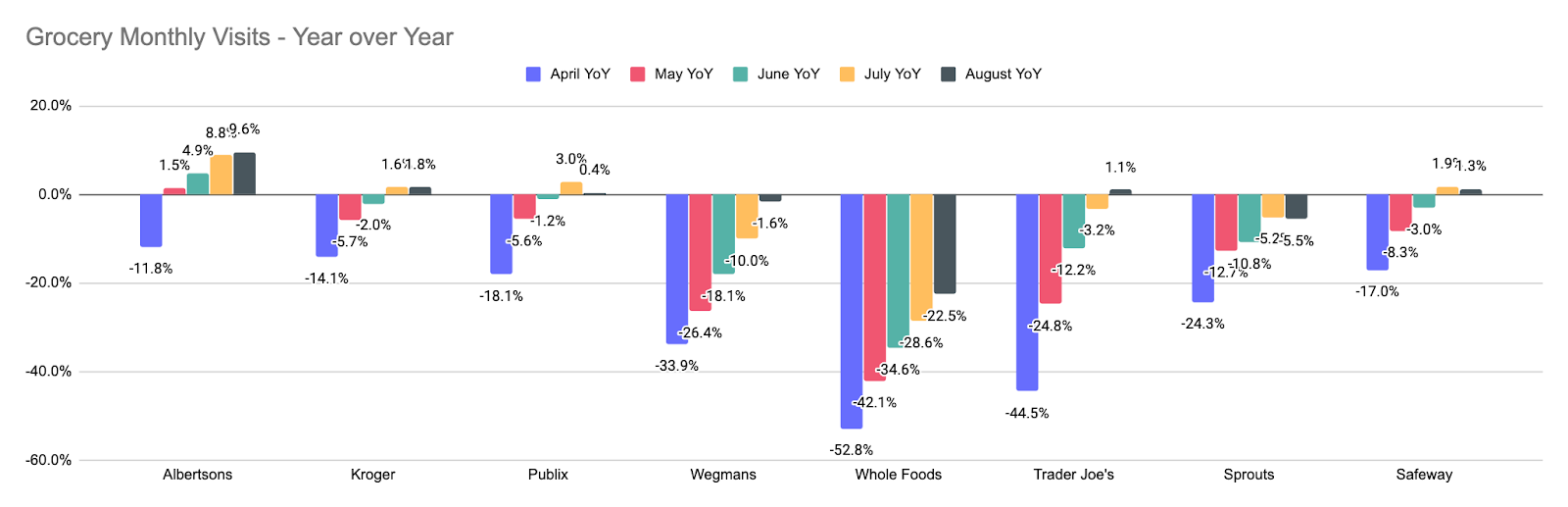

Visits Are Up

The first key metric to analyze is overall visits, and few sectors have seen the same general positive trend as grocery. For the week beginning August 17th, the wider grocery sector was still down 5.3% overall. Yet, much of this was the result of a few outliers that were still seeing significant declines. Instead, the wider picture does look to be very positive for the space. Of the eight brands analyzed, only three saw year-over-year declines in August 2020.

While two of those, Wegmans and Sprouts, were within striking distance of year-over-year growth, Whole Foods was still down 22.5% year over year in August. But critically, even Whole Foods was enjoying a strong recovery that was consistently pulling visit rates higher each month.

And this is a powerful context for a sector that could be well-positioned for the months to come. Periods of economic uncertainty are often defined by a return to grocery, and with traditional supermarket brands already seeing a boost during the pandemic, there is no reason to expect this trend to tail off anytime soon.

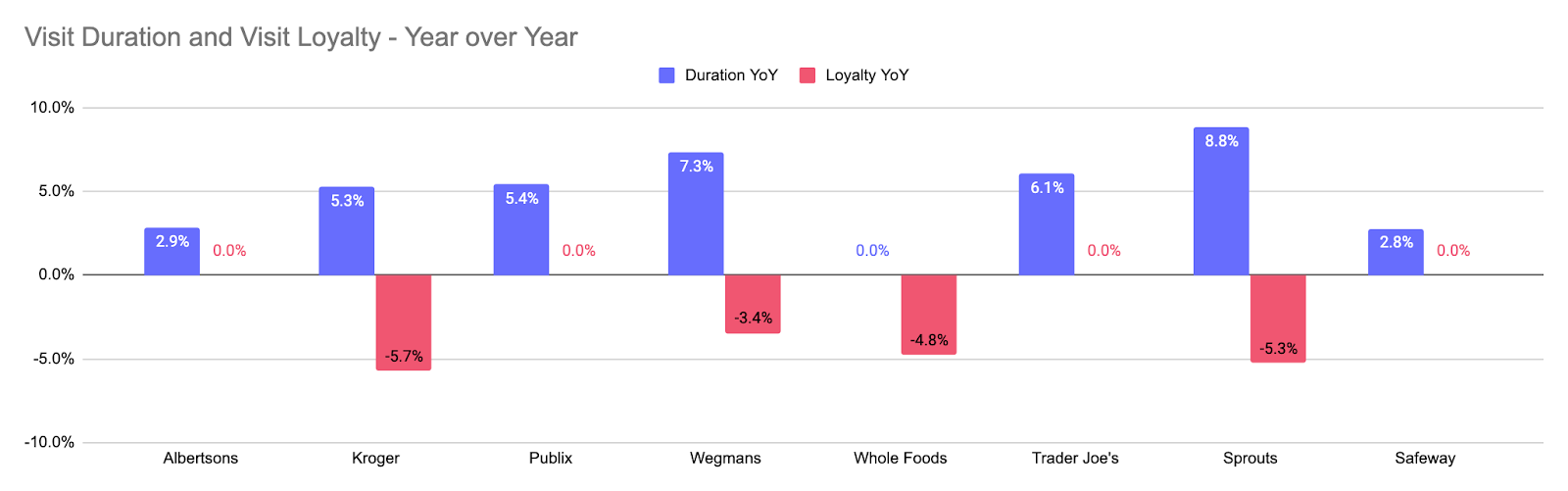

Each Visit Has More Value

It’s not just the visits themselves that should give confidence, but the types of visits as well. Customer loyalty – measured by the number of visits per visitor in July and August 2020 compared to the same period in 2019, either remained stagnant or dropped for all brands analyzed. And while this might normally be seen as a negative, it happened while visit duration – and in many cases overall visits – grew significantly for these same brands. In fact, while loyalty dipped 2.4% year over year for the group, visit length increased 4.8%. This is a hugely significant jump when considering the already long visit duration that supermarkets enjoy.

The conclusion? Mission-driven shopping is pushing visitors to take slightly less trips, but to dedicate more time and buying potential to each visit. With this likely leading to increases in basket size, the combination of growing visit rates and increased time in store could be a potent mix for grocery in the coming months.

When We Shop

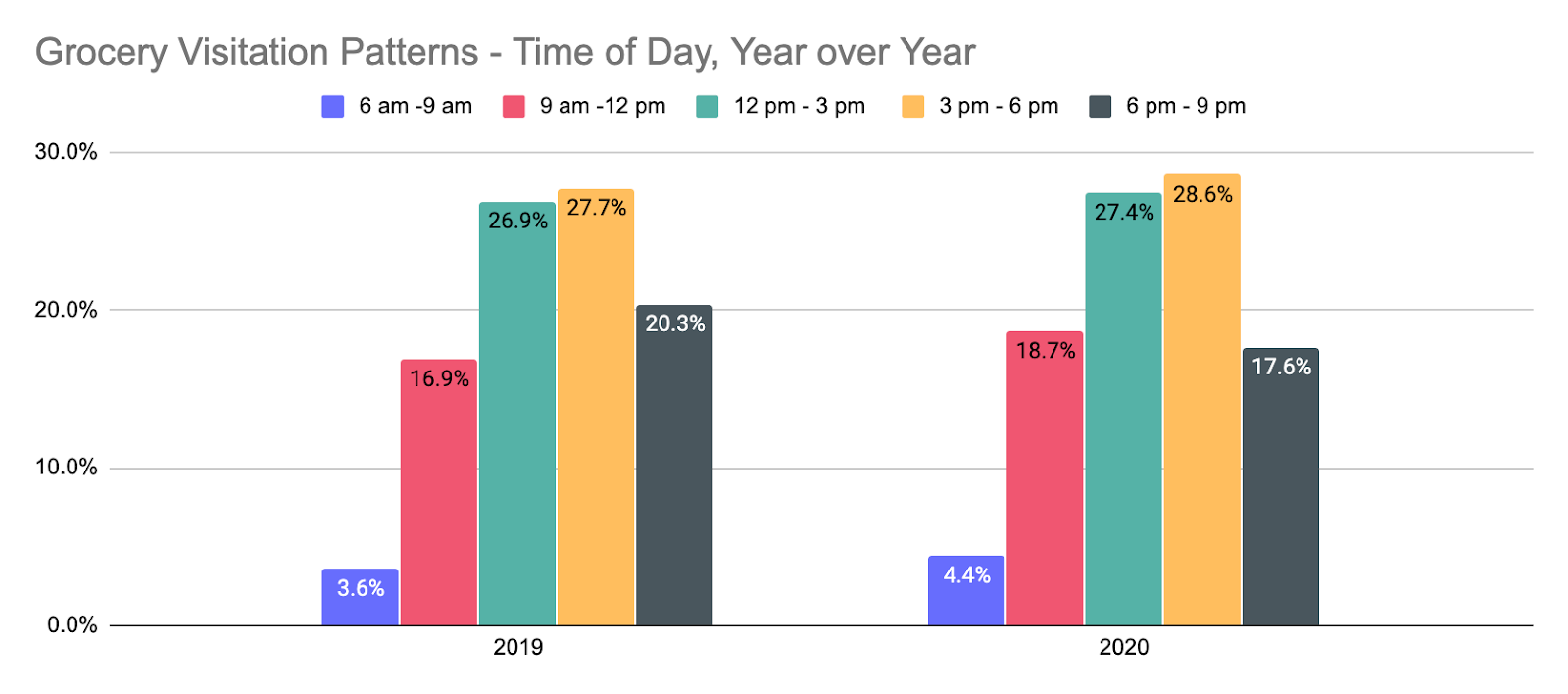

One of the key changes noted in our May analysis was a demonstrable shift of visits from evenings to mornings. And while the difference may not have been as marked in the summer, it was still significant. The percentage of visitors going to grocery stores between 6 am and 9 am, and 9 am and 12 pm, increased significantly between 2019 and 2020. As expected, the biggest drop came from evening visits. This reinforces the point that grocery visitors are showing a clear indication towards morning visits when possible.

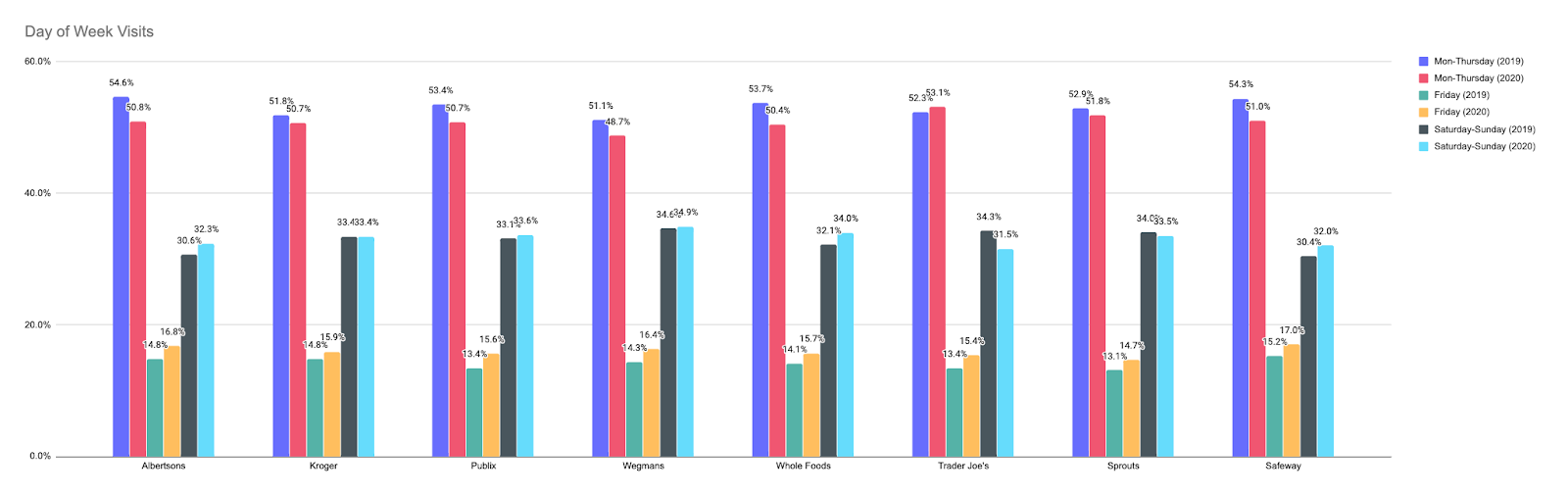

But not all of the changes have lasted. We noted in our last report that Monday through Thursdays saw a lift at the expense of weekends. Yet, it does appear that this shift may have been temporary. Comparing 2019 to 2020, visit rates for Mondays through Thursdays actually dropped in July and August 2020. On the other hand, the biggest gainer wasn’t Saturdays or Sundays, but Fridays. For the group, Friday visits jumped from 14.2% of total visits in 2019, to 15.9% in 2020 – the most significant overall shift.

Why the change here? Maybe summer visits were different in 2020 and weekdays will see a boost once again come September. Maybe Fridays have emerged as a uniquely good day for grocery shopping. Or, maybe there is a slow shift back to normalcy in terms of day of week, while other behavioral changes show more staying power.

Grocery Strength

The biggest takeaway from the latest grocery analysis is that the sector is continuing to show a unique level of strength. Visits are rising as is visit duration even though loyalty metrics are staying stagnant if not dropping. This means for new visitors, likely making more purchases per visit – a recipe for an exceptionally strong period for supermarkets. And with many of these shifts likely to sustain because of an extended period of economic uncertainty, grocery could remain among the most exciting sectors to watch in the months to come.

To learn more about the data behind this article and what Placer has to offer, visit https://www.placer.ai/.

Sign up to receive our stories in your inbox.

Data is changing the speed of business. Investors, Corporations, and Governments are buying new, differentiated data to gain visibility make better decisions. Don't fall behind. Let us help.

Sign up to receive our stories in your inbox.

Data is changing the speed of business. Investors, Corporations, and Governments are buying new, differentiated data to gain visibility make better decisions. Don't fall behind. Let us help.