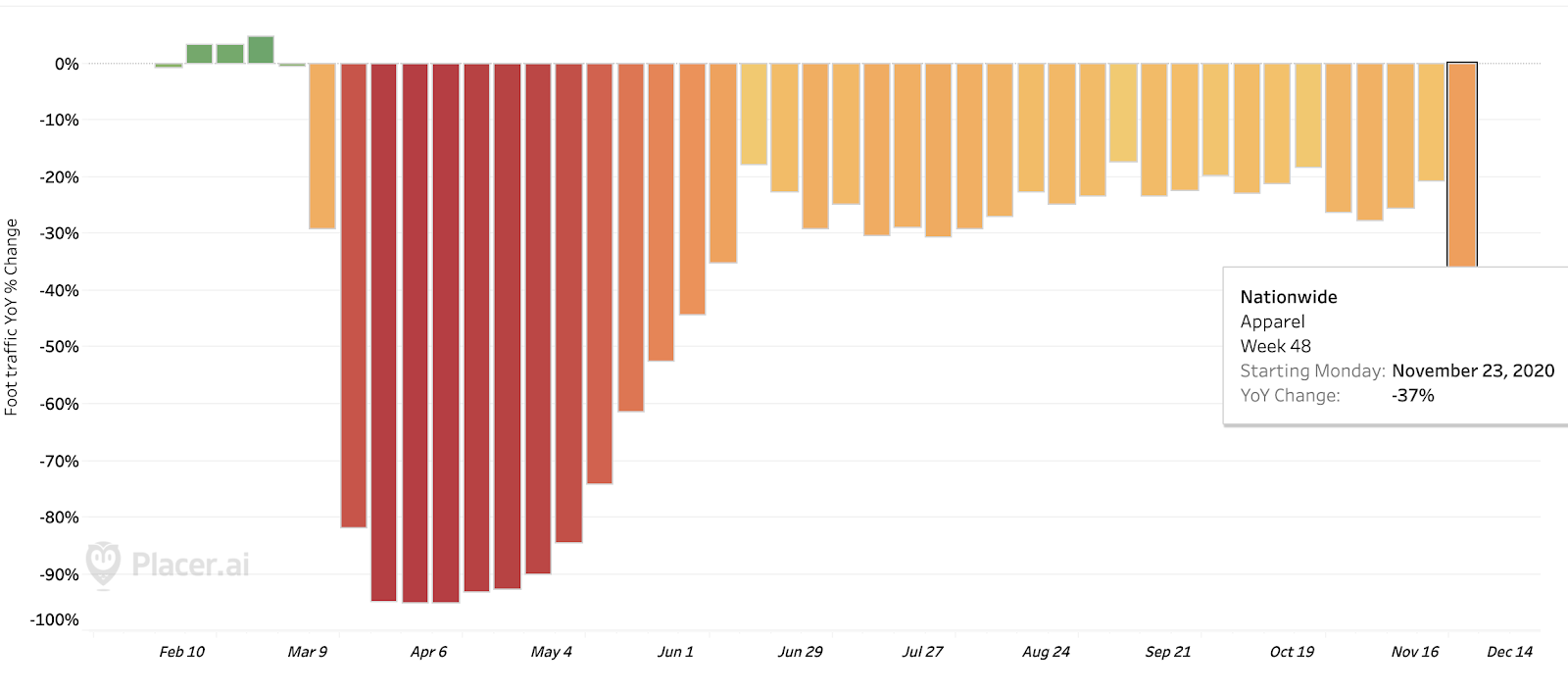

There are few sectors that have felt the brunt of the pandemic’s retail impact like the wider apparel sector. After seeing a rapid recovery in the early weeks following springtime lockdowns, the category stagnated with visits down around 25-30% year over year for most weeks since the summer. And while there were signs that the wider sector was rebounding more sharply into the holiday season, that momentum was cut off by a resurgence of COVID cases which impacted nationwide mall visits.

But, how did some of the top players in the apparel sector perform on Black Friday’s key holiday weekend? We dove into the data to break it down with a look towards the rest of the holiday season.

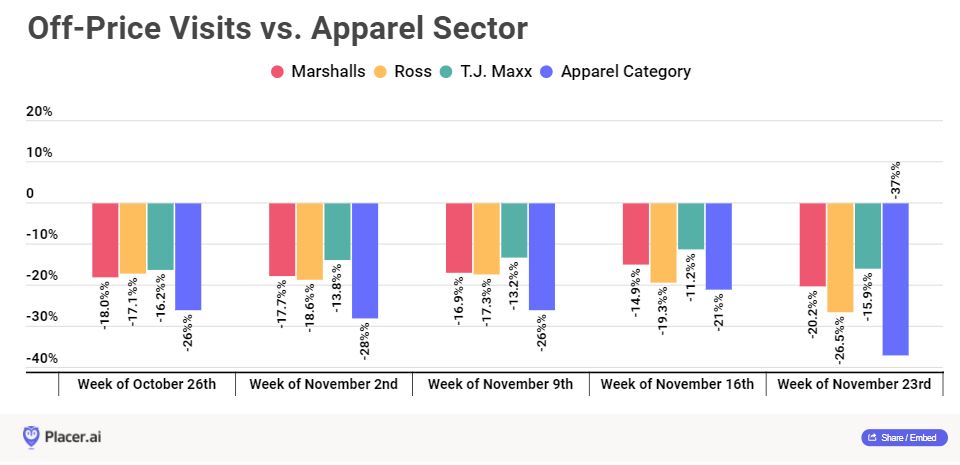

Breaking Down Off-Price’s Relative Success

While there are clearly commonalities between sub-sectors, the apparel sector is not a monolith with a single trend guiding the entire space’s performance. And indeed, some players have stood out for their strength in the face of the current challenges. Looking at three of the top off-price apparel brands, Marshalls, Ross, and T.J. Maxx, shows all three outperforming the wider category significantly over recent weeks continuing a trend seen from the early days of retail re-openings.

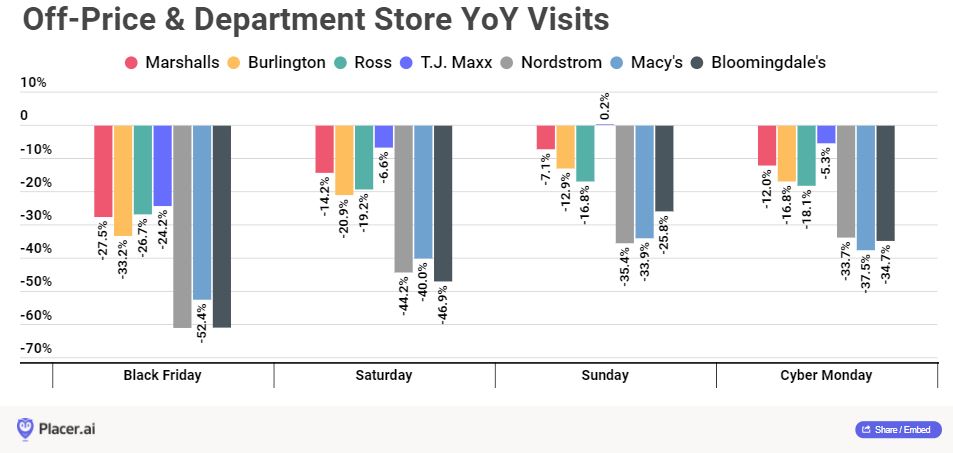

And this trend carried into Black Friday weekend where key off-price brands saw far stronger performances than department store counterparts. Four of the top off-price brands saw average year-over-year declines of 27.9% on Black Friday, with year-over-year drops of 15.2%, 9.2% and 13.0% respectively on the Saturday, Sunday and Monday that followed. This included T.J. Maxx seeing year-over-year growth, however slight, on that Sunday. On the other hand, three top department store brands saw an average year-over-year decline of 58.0% on Black Friday, with the Saturday, Sunday and Monday that followed seeing declines of 43.7%, 31.7% and 35.3% respectively.

But this gap could just be a result of differences in orientation. Off-price, as a sector, is clearly focused on outdoor centers and has a value approach that aligns perfectly with the current environment, seeing a far smaller dependence on Black Friday weekend compared with other retailers.

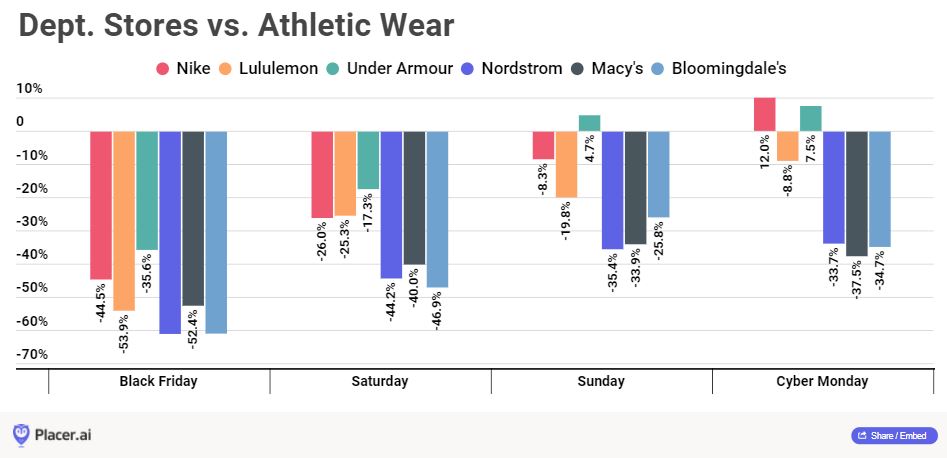

But it wasn’t just this one sector that outperformed department stores. Analyzing the same brands against leaders in athletic apparel and athleisure space saw a similarly significant gap, even though the latter is also heavily dependent on mall traffic. Instead of seeing year-over-year visits gaps of 30% and more like the department store players, these brands saw exceptional performances post-Black Friday, especially considering the context. After watching visits drop 44.5% year over year on Black Friday, Nike saw visits down just 26.0% and 8.3% on the Saturday and Sunday that followed before watching visits rise 12.0% on Cyber Monday. Under Armour saw two days of visit growth with Sunday and Monday seeing traffic that was 4.7% and 6.5% higher respectively than the equivalent days in 2019. And while Lululemon did not see in-store traffic grow compared to 2019, it did see visit rates that were far closer to ‘normal’ than those experienced by department chains, a strong offline performance considering the current obstacles the brand faces.

This leads to a very clear conclusion that it isn’t just the location of these brands within indoor malls or a value orientation holding back their performance, but a fundamental challenge in how they approach customers especially in this environment.

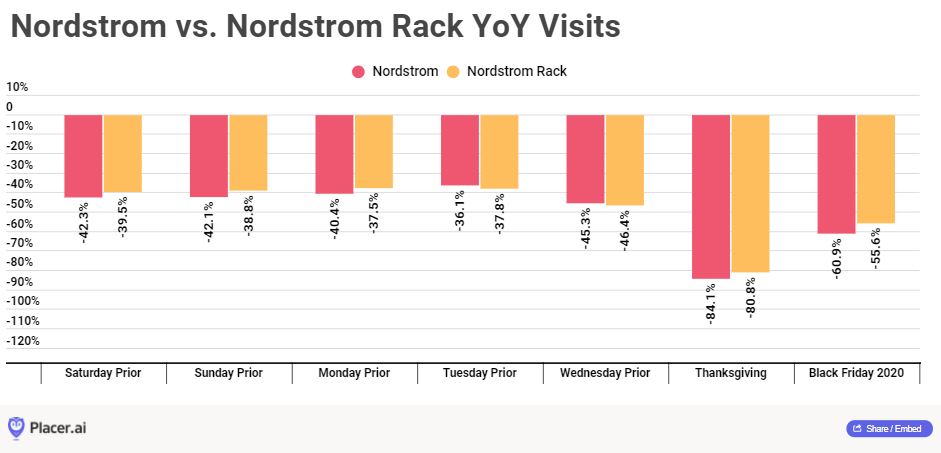

And that flaw goes beyond price. For even when we analyze Nordstorm against Nordstrom Rack we see very similar visitation patterns even though the latter offers significantly more value.

What Does Kohl’s ‘Get’?

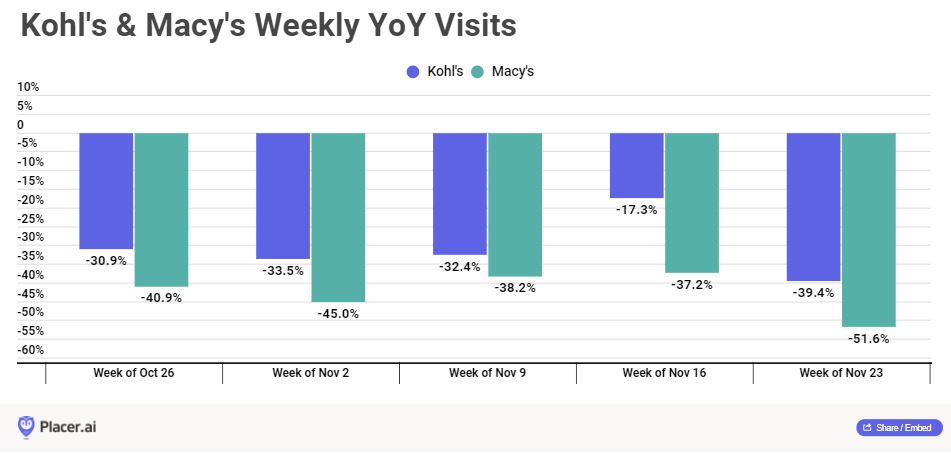

If it isn’t just price, and it isn’t just location, then what is the challenge holding back some brands while others succeed? Analyzing Kohl’s and Macy’s visit trends over recent weeks could give a very strong hint. While the former has seen average year-over-year visit gaps of 30.7% for the six weeks from October 26th through the week beginning November 23rd, Macy’s saw an average visit gap of 42.6%.

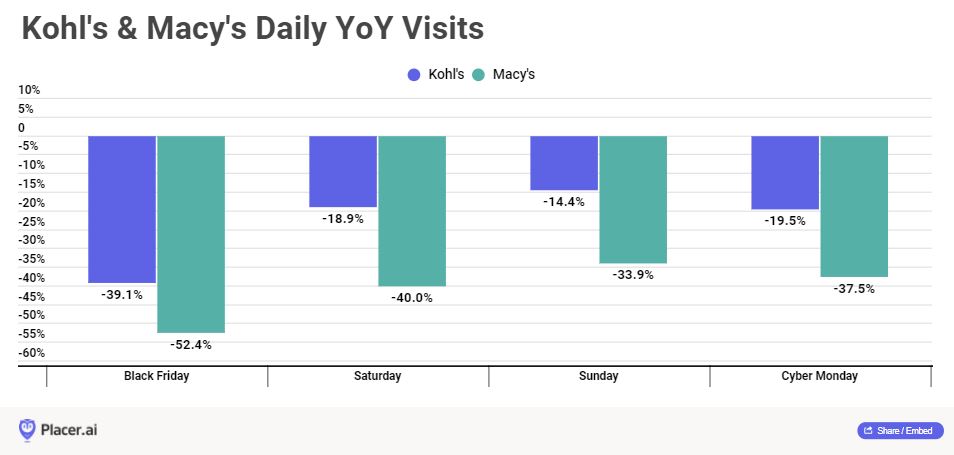

On Black Friday weekend, the differences were similarly large with Kohl’s following a 39.1% year over year Black Friday visit decline, with an average visit gap of 17.6% over the next three days. For Macy’s that split was a 52.4% Black Friday decline and an average visit gap of 37.1% over the next three days. Kohl’s, while clearly benefiting from outdoor locations, is also seeing benefits from its investment in creative partnerships like accepting returns from Amazon or a newly announced concept with Sephora.

Key Takeaways

And this leads to the conclusion that the key to understanding the varying success rates of different sub segments is actually a combination of a few elements. One is the fundamental importance of location. In the very near term, outdoor oriented brands are at a significant advantage, but that could easily shift based on new trends that could arise as early as next year. Instead, the better way of looking at location is emphasizing those who have a more diversified approach. Whether it be the states or regions where different chains have locations or their orientation towards indoor malls, outdoor shopping centers or outlet malls, a more diversified approach will likely allow these brands to succeed in the face of any number of challenges. This diversification may come in the form of rightsizing, new store format concepts or innovative ideas to tap into new markets and audiences.

The second is the brand. Value is always a benefit, but a luxury value offering has unique advantages of its own and even, we daresay, the desire to target the middle has upside as seen in the performance of the Target’s of the world. The emphasis here must be on brand alignment. Marshalls and T.J. Maxx do off-price well because that’s the core element of their brand promise. Nike and Lululemon can charge more for athletic wear because consumers buy into their offering and the experience it provides. For brands like Macy’s to thrive in the years to come, it needs to double down on the authentic brand and approach that will make it resonate with its audience.

The third is timing. Yes, luck does matter. Macy’s, Nordstrom and brands alike faced a seemingly perfect storm that attacked all of their weaknesses simultaneously. While this will likely push them and other brands to focus on more diversified approaches, it’s problematic to pretend like the current environment is anything that could have been ‘predicted’.

To learn more about the data behind this article and what Placer has to offer, visit https://www.placer.ai/.

Sign up to receive our stories in your inbox.

Data is changing the speed of business. Investors, Corporations, and Governments are buying new, differentiated data to gain visibility make better decisions. Don't fall behind. Let us help.

Sign up to receive our stories in your inbox.

Data is changing the speed of business. Investors, Corporations, and Governments are buying new, differentiated data to gain visibility make better decisions. Don't fall behind. Let us help.