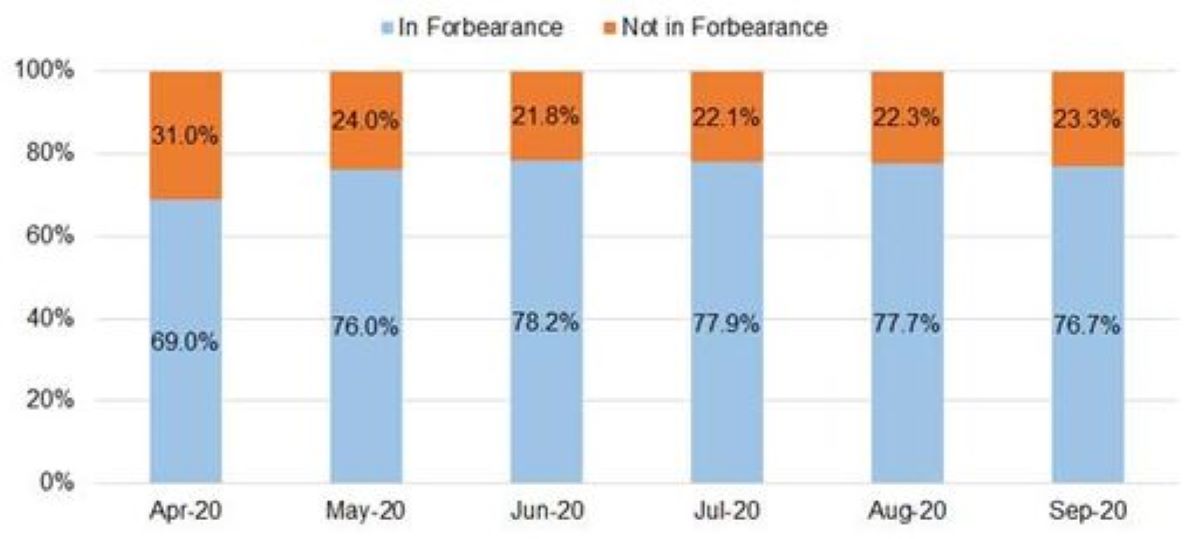

Six months after the CARES Act was signed into law on March 27, 2020, mortgage forbearances remain elevated as millions of Americans sought payment relief after the onset of the COVID-19 pandemic. Beginning in April, forborne loans falling behind payment have become a significant presence in recorded mortgage delinquencies (Figure 1), representing over two-thirds of all delinquent loans.

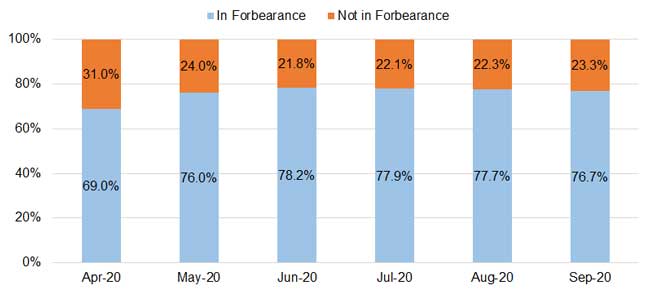

With the economy and jobs recovering in the third quarter, forbearance-related delinquencies began to show signs of small improvement, as some borrowers were able to resume payment or exit forbearance by refinancing existing mortgage under record low interest rates. In addition, the ongoing economic recovery has also sent the forbearance rate to a 6-month low (Figure 2). As a percentage of month-end servicing portfolio, loans in forbearance dropped steadily through Q3, down to 8% from their peak level of 9.8%.

Figure 1: Pandemic Delinquent Loan Pool

Figure 2: Forborne Loans in Overall Servicing Portfolio

However, as shown in Figure 2, among those that remain in forbearance, many loans have fallen further behind payment. The share of 90+-day nonpayment forborne loans in the overall servicing portfolio rose to 4.5% in August and drifted slightly lower to 4.2% in September.

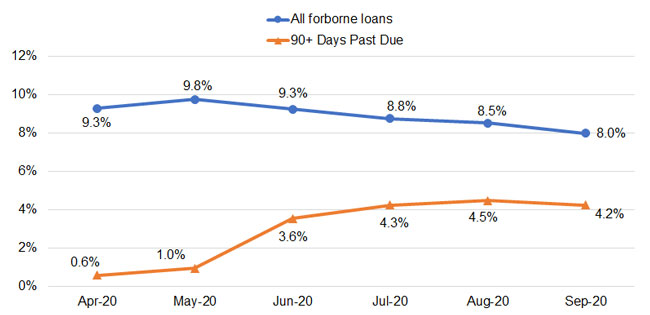

In fact, a distributional analysis of forborne loans’ payment status reveals that nearly more than one third (39.1%) of all forborne loans are now 150+ days behind payment, while as many as 1-in-4 (25.5%) are in nonpayment since April or 180+ days past due. See Figure 3. Rising share of 150+-day or 180+-day nonpayment means that many borrowers currently in forbearance have reached the initial six-month forbearance period. And under the FHFA’s forbearance policy, these borrowers will need to contact their servicers to request an extension for a continued stay in forbearance for up to six additional months. The CARES Act mandates that borrowers of federally or GSE-backed loans receive up to 12-month of payment forbearance.

Figure 3: Distribution of Payment Status of Forborne Loans

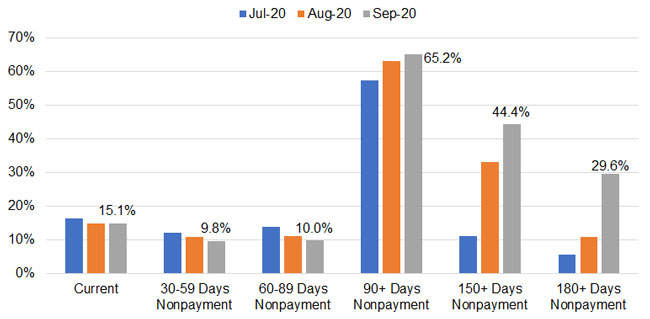

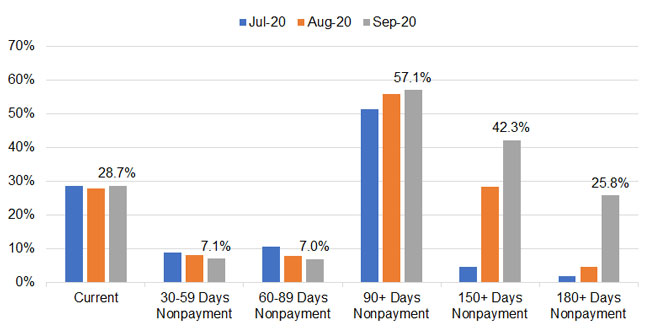

Disaggregating the loans by investor types, Figures 4 through 6 show that as of September, nearly two-thirds (65.2%) of federally-insured forborne loans and more than one half of GSE-backed forborne loans (57.1%) have been in nonpayment for at least 90 days.

Figure 4: Federally-Insured-Loans

Figure 5: GSE-Backed Loans

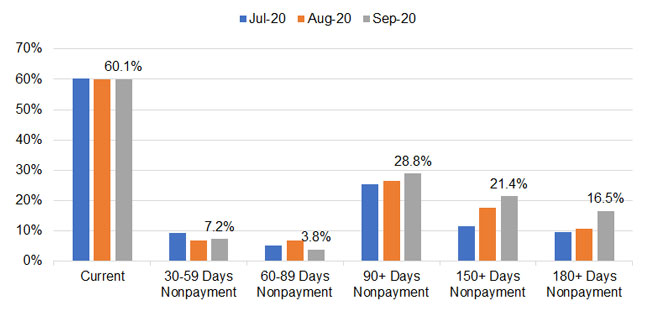

Figure 6: Private MBS or Portfolio Loans

Federally-insured loans also have a higher rate of 150+- and 180+-day nonpayment : as of September, close to 1-in-2 (44.4%) are in nonpayment since May and 29.6% in nonpayment since April; among GSE-backed forborne loans, the 150+- and 180+-day nonpayment rates are 42.3% and 25.8% respectively. In contrast, the majority of private MBS or portfolio loans (60.1%) are current on payment throughout the third quarter and the 90+-, 150+-, or 180+-day nonpayment rates are only a half of federally-insured or GSE-backed loans. According to the CFPB, many servicers of non-federally or non-GSE-backed loans offer the same forbearance options as those covered under the CARES Act.

It remains to be seen in the coming months how many of the forbearances in nonpayment for at least three months - currently at 54.8% of the overall forbearance loan pool - will need an extended stay. The extension rate will likely vary among different loan types. Based on the 150+-day and 180+-day nonpayment rates, an extension rate ranging from 30% to 44% could be expected for federally-backed forborne loan pool. Likewise, for the GSE-backed loan pool, the upcoming extension rate could range from 26% to 42%. Overall, an estimated 1.3 million loans are likely to soon enter the second 6-month forbearance phase

To learn more about the data behind this article and what CoreLogic has to offer, visit https://www.corelogic.com/.

Sign up to receive our stories in your inbox.

Data is changing the speed of business. Investors, Corporations, and Governments are buying new, differentiated data to gain visibility make better decisions. Don't fall behind. Let us help.

Sign up to receive our stories in your inbox.

Data is changing the speed of business. Investors, Corporations, and Governments are buying new, differentiated data to gain visibility make better decisions. Don't fall behind. Let us help.