Source: https://str.com/data-insights-blog/tale-two-occupancies-total-room-inventory-vs-str-standard

Occupancy has long been one of the key hotel performance metrics measured by STR. Reported on both a monthly and weekly basis, occupancy is easily calculated by dividing rooms sold (demand) by rooms available (supply), providing a straightforward representation of the percentage of rooms occupied during a given time period.

However, even this traditional metric has not escaped the impacts of COVID-19. Voluntary and mandated hotel closures caused a fundamental shift in the way we record and report supply, and thus, a new hotel occupancy metric was born.

The status quo

In normal times, and in alignment with USALI guidelines, STR records hotel supply as the property’s total number of rooms multiplied by the number of days in the month. While the latter half of this equation changes each month, the former rarely does—the total number of rooms cannot be altered monthly. Hotel openings, permanent or seasonal closures, and extended renovations are among the exceptions to this rule.

Using this STR Standard methodology allows for a consistent, stable benchmark that captures true market supply changes.

COVID-19 considerations

From early in 2020, staggering numbers of temporary hotel closures followed in the wake of COVID-19’s spread. Some closures were government mandated, while others were voluntary and a result of drastically reduced demand or safety considerations.

Following its standard methodology, STR removed these closed rooms from supply.

A new methodology

The STR Standard methodology measures occupancy of all the open hotels in a market; it effectively tracks realized demand against realized supply and excludes temporarily closed rooms that could not be booked.

This metric does not measure the total potential occupancy of a market, that is, the number of rooms demanded as a percentage of the total number of rooms existing in a market. For this metric, STR introduced Total-Room-Inventory methodology. This methodology takes realized demand and divides it by the total number of rooms in a market regardless of operational status (a.k.a. total room inventory).

Ins and outs of occupancy

The result is that STR can report two occupancy numbers for any given market: occupancy, which utilizes the STR Standard methodology, and Total-Room-Inventory occupancy, which utilizes this new methodology.

Until all temporarily closed properties in a market have reopened, TRI occupancy will be less than occupancy, because its base (supply) is bigger. The size of the delta between these two occupancy measures can indicate the amount of hotel closures in a market as well as help assess market recovery.

When to use what

While having two occupancy measures may be confusing, each methodology has unique use cases that allow a savvy operator to holistically understand performance in an unprecedented situation.

For example, open properties benchmark performance against STR Standard occupancy, because it allows an apples-to-apples comparison against other open competitors.

Closed properties can use STR Standard occupancy to gauge what their potential performance could be upon reopening and utilize the delta between the two occupancies to keep watch on how much of the market is open as well as a check on overall market demand.

For forecasting purposes, pipeline analyses, to gauge the full impact of the COVID-19 pandemic on a market, and to track recovery, TRI occupancy is the more preferred metric among industry stakeholders.

Inspect before you accept

Standard versus TRI occupancy allows a better view of market recovery. With tourism ramping up in places such as the United States, it is easy to expect a higher-than-2020 occupancy level. When we do see a higher standard occupancy level for a market, it is important to inspect the TRI level before you accept that a market has achieved a phase of recovery.

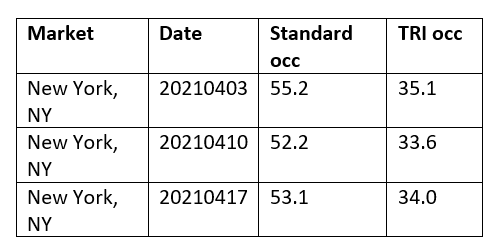

A good market example of “inspect before you accept” is New York City. Standard weekly occupancy in the market throughout April 2021 has shown levels upwards of 50%. At first glance it may be easy to accept this occupancy level, especially given that other major markets across the U.S. have reached levels of 60-70%. However, many New York hotels shut their doors at the beginning of the pandemic, and a year later, a large amount remain closed. With this in mind, we must inspect the TRI occupancy.

When adding in the closed hotels, the market’s occupancy tells a different story. Both methodologies show occupancy increased year over year. When looking at 11-17 April 2021, the 2020 comparable week showed a standard occupancy of 39.1% and a TRI occupancy of 22.0%. So yes, the market is in fact improving. However, if we compare the 2021 week with the 2019 comparable week, we get two different views of hotel industry recovery. Since we know 2019 was not a pandemic-affected year, we can compare both methodologies to the standard occupancy level.

The comparable week in 2019 showed a 92.2% standard occupancy level. When we index the standard 2021 level to the 2019 level, we get 57.6 – meaning the market’s occupancy would have been roughly 58% of what it was in 2019. However, when we index with the TRI occupancy level, we only get 36.9%.

STR uses an index to place each market in one of four categories: depression (index <50), recession (index between 50 and 79.9), recovery (index between 80 and 99.9), and peak (index >=100).

There are two different views of recovery when we look at both methodologies:

Standard occupancy (11-17 April 2021) = Recession

TRI occupancy (11-17 April 2021) = Depression

As we make our way through the recovery process, it is imperative that we are checking all our boxes so we can truly understand how a market is performing.

What’s next

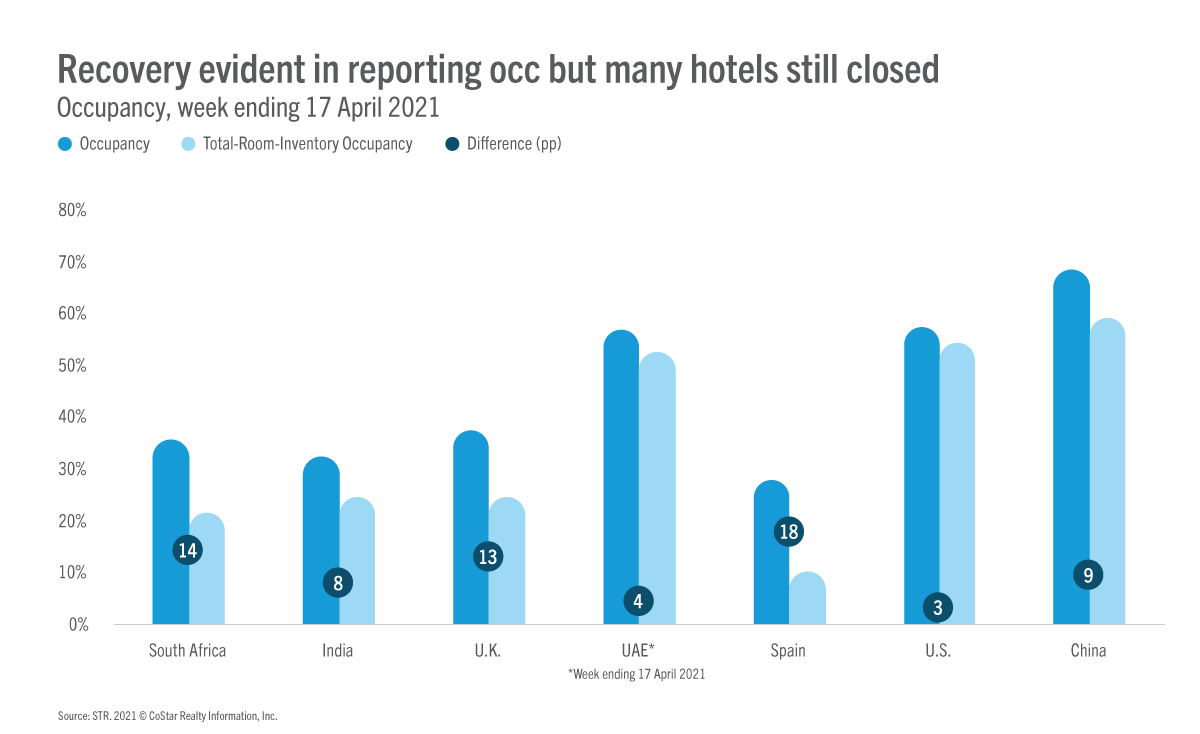

In countries such as the U.S., where large amounts of the population are vaccinated, we will begin to see an increase in domestic travel. With talks of allowing vaccinated visitors in some parts of the world (i.e. European Union), we can expect to see an increase in international demand as well. As temporarily closed hotels reopen or close permanently, TRI occupancy and STR Standard occupancy will converge once again into one metric. This is evident in the U.S. and UAE, where the difference between occupancy types is less than five percentage points.

STR will continue to use both occupancy metrics to analyze and interpret COVID-19 impacts and recovery.

To learn more about the data behind this article and what STR has to offer, visit https://str.com/.

Sign up to receive our stories in your inbox.

Data is changing the speed of business. Investors, Corporations, and Governments are buying new, differentiated data to gain visibility make better decisions. Don't fall behind. Let us help.

Sign up to receive our stories in your inbox.

Data is changing the speed of business. Investors, Corporations, and Governments are buying new, differentiated data to gain visibility make better decisions. Don't fall behind. Let us help.