Like the malls they anchor, department stores were being eulogized long before the COVID pandemic hit American retail. But whereas many malls bounced back already in the summer of 2021, many department store brands continued to struggle to return to pre-pandemic foot traffic levels. Now, with two years of pandemic life behind us, we dove into foot traffic to leading high-end and mid-range department store chains to understand how the “new normal” looks for this critical retail sector.

High-End Department Stores Leading the Pack

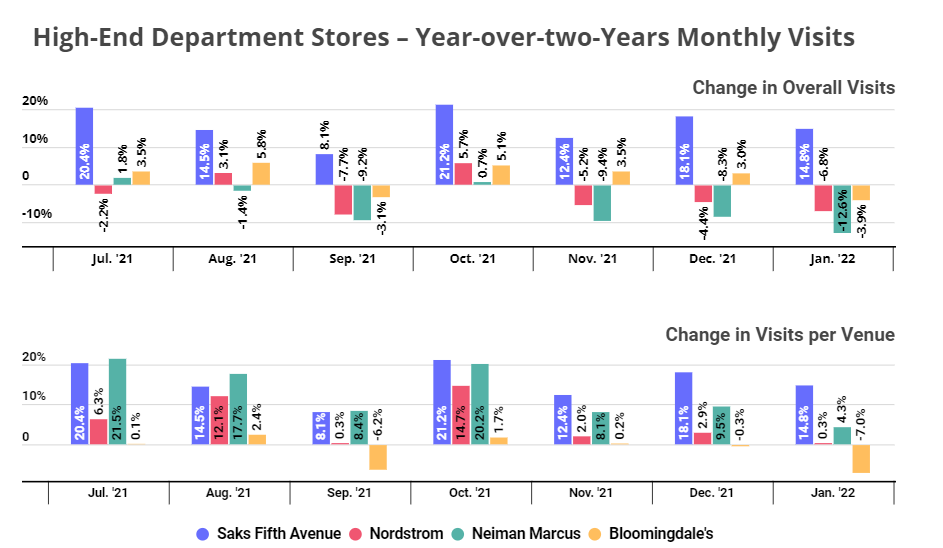

Visits to luxury stores have been strong in recent months, and the demand for quality goods is boosting visits to Saks Fifth Avenue, Nordstrom, Neiman Marcus, and Bloomingdale’s.

Saks Fifth Avenue, whose store fleet has stayed relatively consistent throughout the pandemic, has also seen the largest increase in foot traffic over the past seven months, with January visits up 14.8% compared to January 2020. Nordstrom, which permanently closed over 10% of its full-line stores due to the impact of COVID, has seen Yo2Y growth in its visits-per-venue metrics every month since July ‘21, ending the year strong with a 2.9% Yo2Y growth in December visits-per-venue.

Neiman Marcus, which entered bankruptcy in May 2020 – from which it emerged in September of the same year – has also closed several locations, and re-focussed its strategy on catering to Neiman’s luxury-oriented core customer base. The result is an impressive jump in its visit-per-venue numbers, with holiday season Yo2Y visits-per-venue numbers of 12.4% and 18.1% for November and December, respectively.

Bloomingdale’s did see a slight drop in visits-per-venue compared to its overall visit numbers, likely due to its slight store fleet expansion through a new store the retailer opened just before the pandemic hit and the new Bloomie’s, small-format concept opened in August. But its overall visit numbers have been strong, with overall Yo2Y holiday visits up 3.5% and 3.0% in November and December, respectively.

Given their recent visit performance, luxury department stores are well positioned to thrive in 2022.

Right-Sizing Easing Recovery for Mid-Range Brands

The visit recovery has been slightly more challenging for mid-range department store chains. Macy’s, Kohl’s, JCPenney, and Dillard’s have all seen their 2021 monthly visits continue to lag behind 2019 foot traffic levels, although the retailers who consolidated their store fleet have managed to soften the blow.

In February 2020, before the COVID outbreak hit American retail, Macy’s announced its plans to close 125 stores over the following three years. So far, the strategy seems to be working, and the company’s visits-per-venue numbers are significantly stronger than its Yo2Y overall foot traffic metrics. The company is planning on implementing the remaining 60 planned closures in 2022, so expect its visits-per-venue numbers to climb even further as Macy’s continues to optimize its fleet. This optimization trend is especially noteworthy as it indicates that Macy’s rightsizing strategy is enabling the brand to better maximize the reach of each location.

Kohl’s is one of the few department store chains that has not closed a significant number of stores in recent years, and so its visits per venue trend track its overall Yo2Y visit numbers pretty closely. But the company has announced plans to expand its collaboration with Sephora, and as Kohl’s locations with Sephora shops-in-shop are consistently outperforming those without, adding Sephora shops to more Kohl’s locations may well drive up foot traffic numbers across the chain.

Like Neiman Marcus, JCPenney entered bankruptcy in May 2020, and the company exited bankruptcy in December 2020 with significantly fewer stores and plans to permanently close around a third of the stores it operated pre-pandemic. Now, foot traffic data from the past seven months shows that the brand is close to optimizing its store fleet: December visits-per-venue were down just 5.5% Yo2Y.

Dillard’s has also permanently closed several stores – turning some of the shuttered locations into Dillard’s Clearance Centers – so its Yo2Y visits-per-venue metrics are stronger than its overall Yo2Y visit numbers, with December visits-per-venue down just 1.5% compared to December 2019. And since Dillard’s is the only mid-range department store analyzed that actually saw Yo2Y growth in overall monthly visits in 2021, with July and October Yo2Y visits up 2.4% and 2.9%, respectively, there is ample reason for optimism going into 2022.

While a COVID defined January did no brand in the sector any favors, the latest data does show that the picture for mid-range department stores is far rosier than it might have seemed.

Brick and Mortar Apparel Visits Recovering Slowly

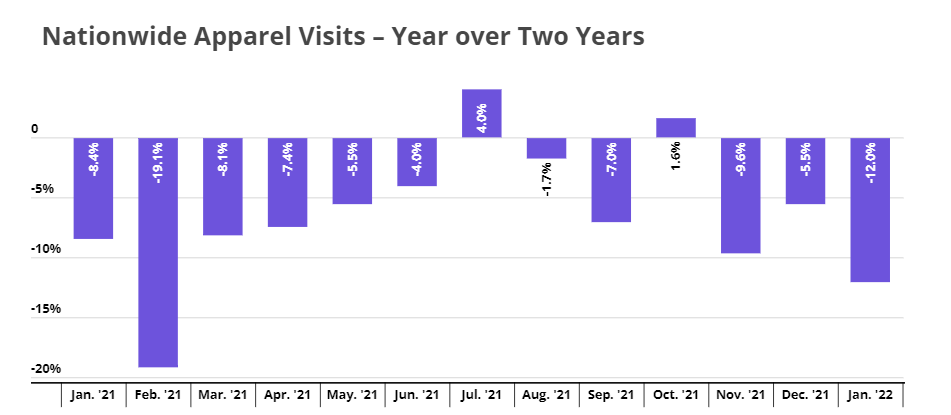

Before writing off department store brands that are slower to recover, some context is critical. The pandemic hit overall apparel visits hard, and recovery for the sector has been slow.

Comparing nationwide monthly apparel visits in 2021 to nationwide apparel visits two years prior shows how closely the apparel recovery is correlated to the COVID situation. Apparel visits finally reached Yo2Y growth in July – but then the Delta wave and apparel visits came crashing down again in late August and September. Visits recovered in October, but the declining importance of Black Friday hurt November foot traffic while the Omicron surge kept visits low in December and January.

The silver lining from the data is that apparel visits do seem to recover every time the COVID situation stabilizes. This means that there is serious potential for a full apparel recovery once this pandemic subsides – which means that the department store brands that are currently struggling may still make a comeback in 2022.

To learn more about the data behind this article and what Placer has to offer, visit https://www.placer.ai/.

Sign up to receive our stories in your inbox.

Data is changing the speed of business. Investors, Corporations, and Governments are buying new, differentiated data to gain visibility make better decisions. Don't fall behind. Let us help.

Sign up to receive our stories in your inbox.

Data is changing the speed of business. Investors, Corporations, and Governments are buying new, differentiated data to gain visibility make better decisions. Don't fall behind. Let us help.