About the Mall Index: The Index analyzes data from more than 100 top-tier indoor malls, 100 open-air lifestyle centers (not including outlet malls) and 100 outlet malls across the country, in both urban and suburban areas. Placer.ai uses anonymized location information from a panel of 30 million devices and processes the data using industry-leading AI and machine learning capabilities to make estimations about overall visits to specific locations.

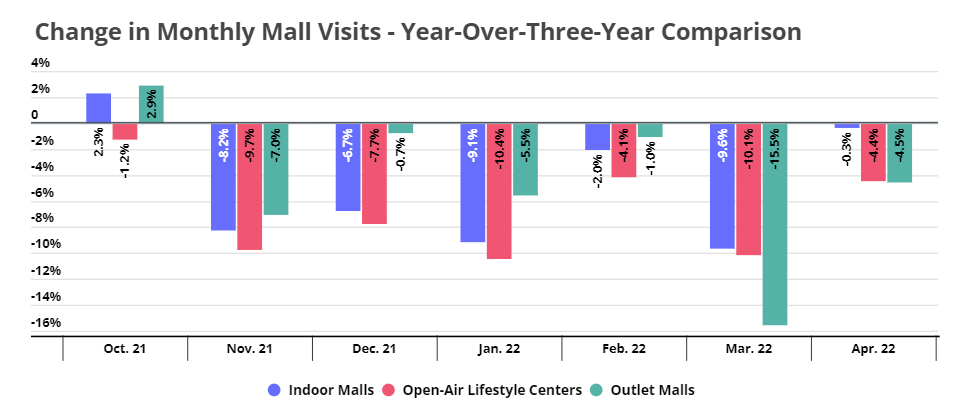

When indoor malls saw a return to growth in October 2021, there was a sense of a turning tide for one of the key institutions in brick and mortar retail. Yet, comparisons to pre-pandemic holiday seasons and the rise of Omicron alongside a myriad of other challenges stunted that development. The traffic declines continued into 2022, driven largely by those same factors.

Yet, already in March, weekly data started showing a shift with visit rates improving amidst a trend of normalizing behaviors.

April’s Step Forward

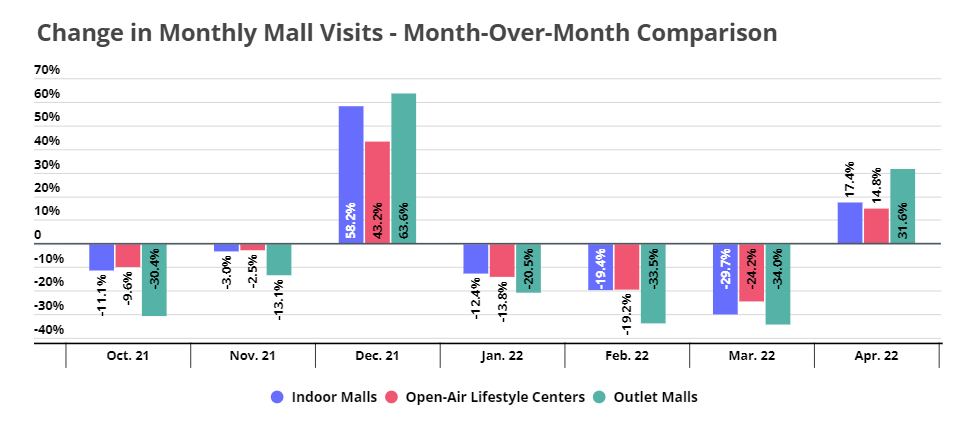

Looking across the Placer.ai Mall Index for top performing indoor malls, open-air lifestyle centers, and outlet malls in April, all formats saw a major decline in the visit gap compared to March. Visits to indoor malls were down just 0.3% compared to the same month in 2019, while open-air and outlet centers saw visit gaps shrink to just 4.4% and 4.5% respectively.

The jump in traffic becomes even more apparent when analyzing visits to these three indexes on a month-over-month basis. April visits rose 17.4% for indoor malls, 14.8% for open-air lifestyle centers and a massive 31.6% for outlet malls compared to March. The Easter holiday clearly provided a boost, but much of the improvement is also related to a growing visit normalization following the initial shock of rising gas prices and increased inflation. The former provides an especially significant impact as it undermines the willingness of a consumer to travel farther for a retail experience.

Data Trending Right Once Again

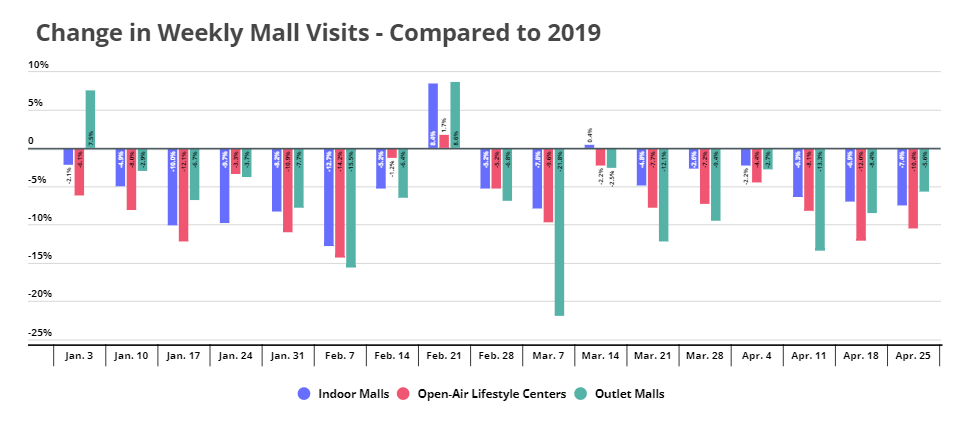

But weekly data also shows that there is room for continued improvement. While April was the strongest month yet in 2022 for indoor malls, open-air centers, and outlet malls, these venues were still feeling the pressure of new challenges when comparing visits to 2019. The improving visit gaps for open air lifestyle centers and outlet malls in the latter part of April shows the potential that the appetite for a longer trip to ensure a value oriented or single-location retail and entertainment experience could be growing once again.

And the timing here is critical. While the relative strength shown in recent months is impressive, especially considering the external pressures, the summer season presents a uniquely powerful opportunity for top tier centers across categories.

Should the wider COVID recovery continue and the impact of some of retail’s newer challenges begin to dissipate, the coming months could see a sharp rise in mall traffic and engagement.

To learn more about the data behind this article and what Placer has to offer, visit https://www.placer.ai/.

Sign up to receive our stories in your inbox.

Data is changing the speed of business. Investors, Corporations, and Governments are buying new, differentiated data to gain visibility make better decisions. Don't fall behind. Let us help.

Sign up to receive our stories in your inbox.

Data is changing the speed of business. Investors, Corporations, and Governments are buying new, differentiated data to gain visibility make better decisions. Don't fall behind. Let us help.