April marked an important month for retail recovery, but one sector that may be less thrilled to see the coming spring is home improvement. The brands in the space have seen incredible strength throughout the pandemic, with Q1 marking another strong quarter.

Yet, unlike most sectors that will benefit from 2020 weakness to emphasize 2021 strength, home improvement leaders will be compared to their unique peak during the pandemic. These brands will be tested to see if 2020’s success was a ‘lightning in a bottle’ moment or the beginning of a much larger and ongoing trend.

The Rise Continues (For Most)

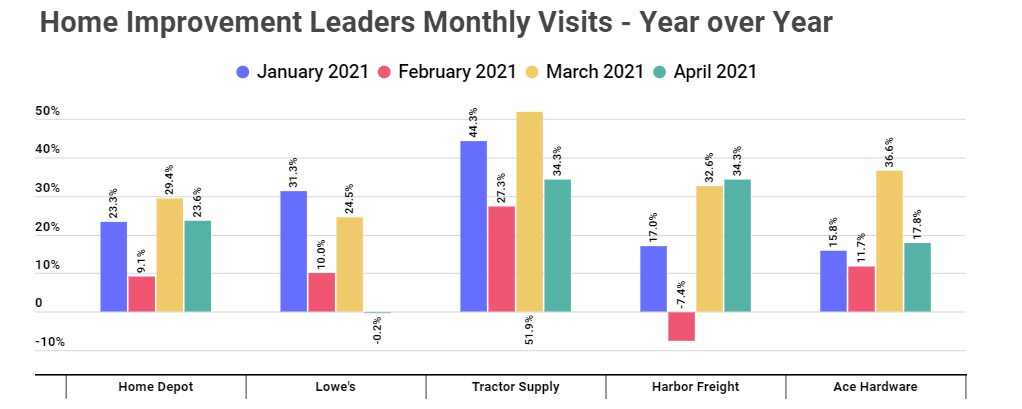

Over a year ago in April 2020, as most of the retail sector suffered through full shutdowns, home improvement leaders leveraged essential retail status to drive strength. The month was especially successful for Lowe’s which saw visits jump 14.4% year over year. However, this peak – driven by the combination of essential retail status, alignment with a normal seasonal peak and an increased interest in improving the home – created a difficult mark to match in 2021.

So while Home Depot, Tractor Supply and Harbor Freight saw year-over-year visit growth of 23.6%, 34.3% and 34.3% respectively, Lowe’s saw a 0.2% year-over-year decline. Notably, this is the first decline Lowe’s has seen since the pandemic began impacting retail in February 2020.

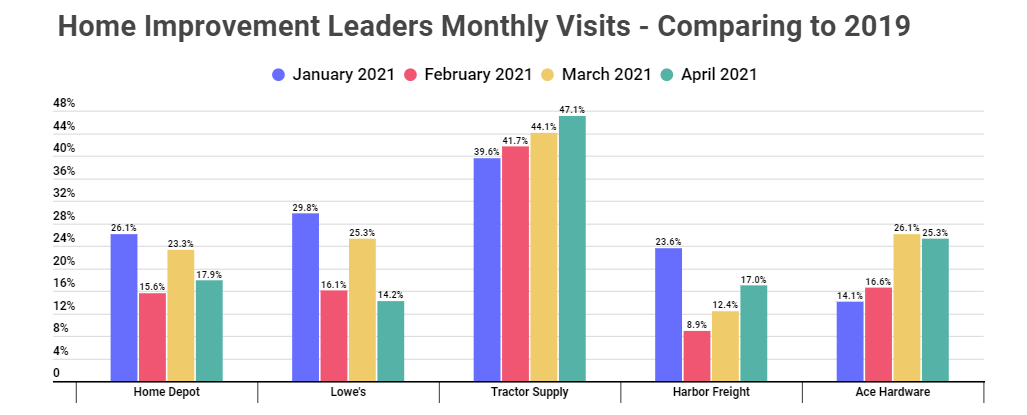

But while Home Depot and others deserve tremendous credit for their continued growth, it’s important to put Lowe’s decline into proper context. While the brand did indeed see visits drop year over year, when comparing April 2021 to April 2019, there was actually a 14.2% increase. Using that same comparison, Home Depot saw 17.9% jump, with Tractor Supply seeing a massive 47.1% increase.

Essentially, all home improvement metrics are going to be weighed against the unique peak experienced last year, allowing the added 2019 comparison to provide wider context. So while a 0.2% visit decline in April for Lowe’s may seem problematic against the backdrop of growth for competitors, it is critical to remember that the month was still exceptionally strong for the brand.

Home Improvement’s Balance of Power

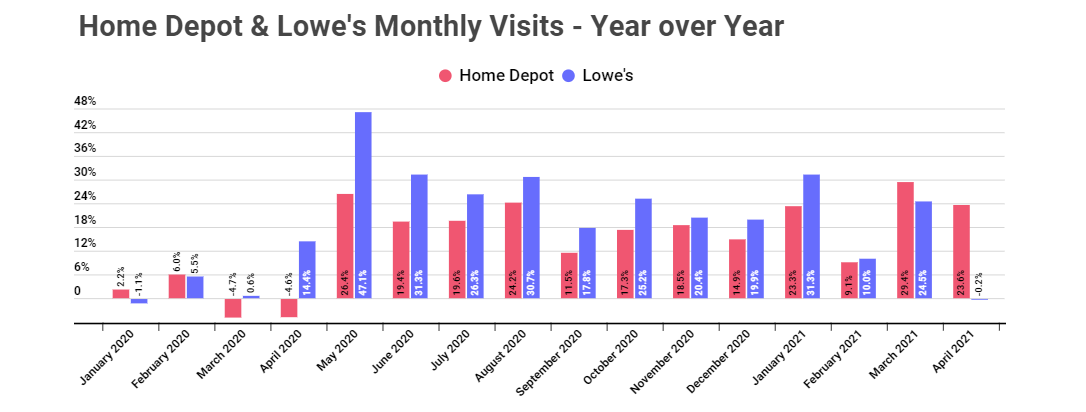

And this becomes all the more critical when comparing Home Depot and Lowe’s directly. In April 2020, Home Depot saw a 4.6% year-over-year visit decline as Lowe’s surged to a 14.4% increase. This, likely driven by regional differences and a slightly stricter approach to shopper counts, gave Home Depot a position to drive bigger growth numbers.

But the real question boils down to how these shifts impacted the overall balance of power in Home Improvement. And while a major change would be more exciting, the reality is that the pandemic’s retail environment was more likely a tide that lifted all home improvement boats.

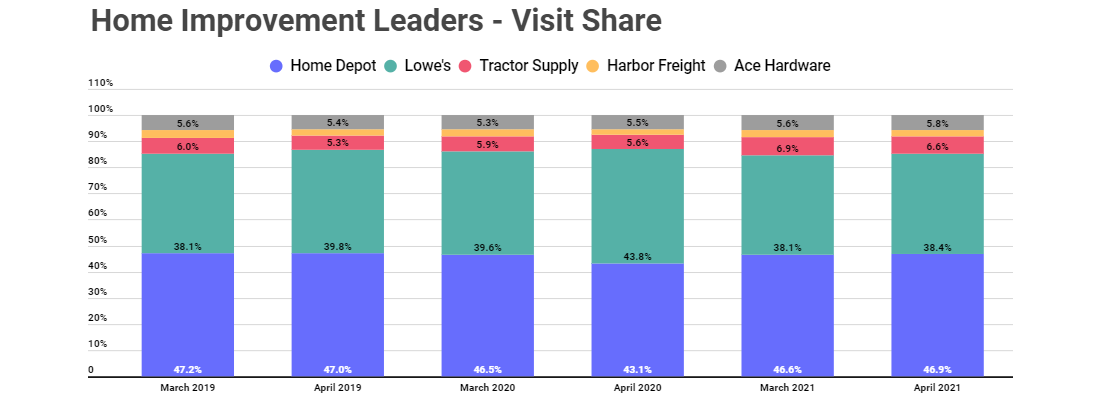

Apart from April 2020, when Lowe’s surpassed Home Depot in overall visit share because of the reasons mentioned above, Home Depot has maintained its visit share lead. In March and April of 2019, Home Depot averaged an 8.2% greater visit share than Lowe’s when looking at a group of five top home improvement retailers, a number that grew slightly to 8.4% in 2021. Tractor Supply also saw its share among the analyzed group grow from 5.7% in 2019 to 6.7% in 2020. But in the end, the players analyzed showed fairly minor shifts in relative positioning while enjoying an overall boost that drove an extended surge for the entire sector.

To learn more about the data behind this article and what Placer has to offer, visit https://www.placer.ai/.

Sign up to receive our stories in your inbox.

Data is changing the speed of business. Investors, Corporations, and Governments are buying new, differentiated data to gain visibility make better decisions. Don't fall behind. Let us help.

Sign up to receive our stories in your inbox.

Data is changing the speed of business. Investors, Corporations, and Governments are buying new, differentiated data to gain visibility make better decisions. Don't fall behind. Let us help.