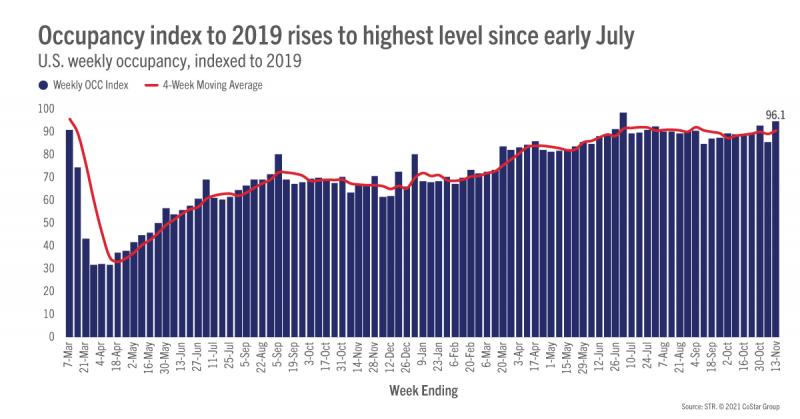

The U.S. hotel industry saw its largest week-over-week demand gain since early October with 704,000 more room nights sold for the week ending 13 November 2021. Weekly demand has increased in 21 of the past 33 weeks and the most recent week’s gain was the 10th largest in that span. With the increase, occupancy advanced to 61.6%, up 1.9 percentage points from the previous week. Compared with 2019, occupancy indexed at 96, which was the highest level since early July. Average daily rate (ADR) also improved, up 1.3% week on week, to a level that was three percent higher than what it was in 2019. As a result, revenue per available room (RevPAR) strengthened by 4.5% in the week and reached its best 2019 comparison since August.

Most of the demand growth (89%) came from weekdays, which saw the largest gain since the week after Labor Day. Demand increased the most on Sunday and Monday with Tuesday also producing large improvements. Strong growth was also seen on Thursday. While those days led the week’s performance, weekday occupancy remained lower than weekends (57% versus 73%). The 2019 occupancy index for weekdays sat at 90 with the weekend at 111, meaning that weekend occupancy was 11 percent higher this year than in 2019.

In the Top 25 Markets, progress was seen Monday through Wednesday, which accounted for nearly half of the weekly demand gain. This indicates that business travel continues to strengthen even as the year draws to a close. Top 25 occupancy on those three days reached 59%, the highest since late summer, with Phoenix leading the pack at 73%. New York City followed Phoenix with a 3-day weekday occupancy of 68%, which is the highest the market has seen since the week before the first lockdown. NYC’s complete weekday (Sunday-Thursday) occupancy hit 69%, and its weekend level topped 87%, which were both pandemic-era highs that contributed to a full week average of 74%.

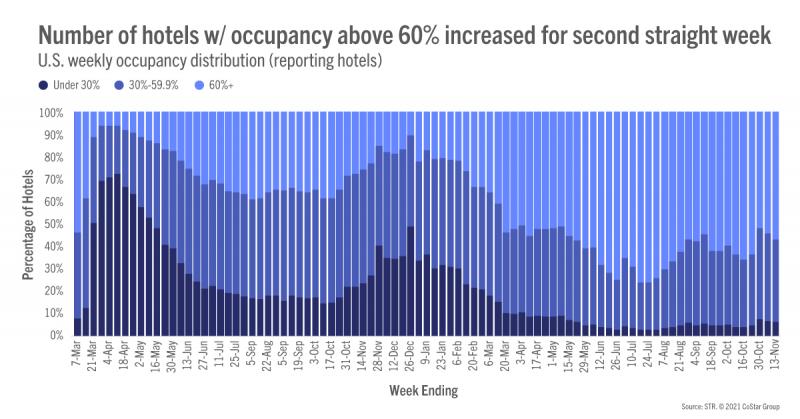

More than half of reporting hotels had occupancy above 60%. In the Top 25 Markets, nearly two-thirds of hotels were at or above that level. In NYC, more than three-quarters of hotels reported occupancy above 70% with 22% at 90%+, the most of the past 20 weeks.

ADR advanced week on week in 54% of all markets with the largest gains observed in destination locations, including Daytona Beach, the Florida Keys, and New Orleans. Eighty percent of markets reported a weekly ADR that was higher than the comparable week of 2019. On an inflation-adjusted basis (real), 57% of all markets had a higher ADR than in the same week of 2019. Overall, weekly real ADR countrywide was 96% of the 2019 level, similar to what was seen in the summer.

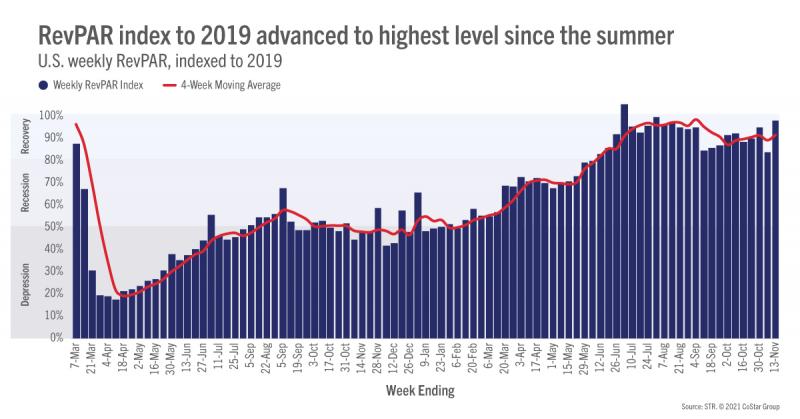

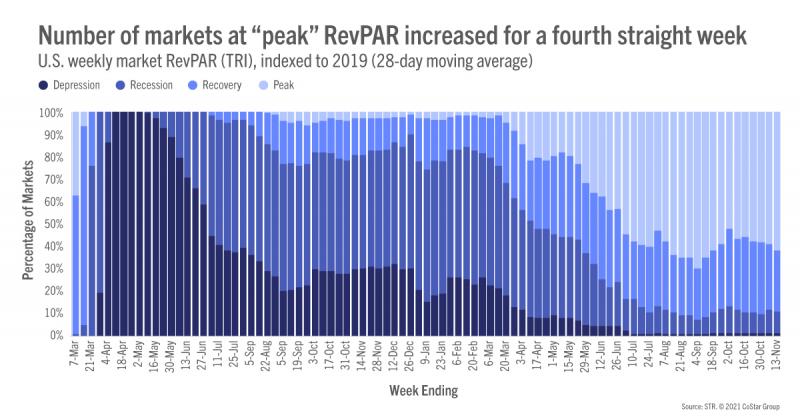

Weekly RevPAR indexed to 2019 increased to 99, which was among the highest values of the year. Real RevPAR indexed to 2019 stood at 93 for the week. Thus, both measures keep the industry in STR’s “recovery” category given that the indices are above 80 but below 100. On a 28-day moving total basis, the 2019 RevPAR index was 92 with 62% of markets at “peak” (RevPAR indexed to 2019 above 100). Adjusting for inflation, 49% of markets were at “peak” RevPAR with another 34% in “recovery.” San Francisco and San Jose remain the only two markets in the “depression” category (RevPAR indexed to 2019 below 50). Both markets, however, are improving.

Outside of the U.S.

Global occupancy, excluding the U.S. and on a total-room-inventory basis (TRI), remained in the doldrums at 40%, down nearly a percentage point from the previous week. ADR also fell after rising in the previous three weeks. China saw occupancy fall another three percentage points to 34%, its lowest level since mid-August. The U.K. continued to see the highest occupancy level (62%) of the 10 largest countries based on hotel supply, but its level declined for a second consecutive week albeit at a lower rate than in the previous week.

Europe is facing some challenges as COVID cases increase again, resulting in new travel restrictions. Occupancy has dropped over the past three weeks, falling to 42% in the latest week of reporting. At present, most of the restrictions center on the unvaccinated but that is changing. Austria announced a national lockdown beginning Monday, 22 November and lasting for a minimum of 10 days with the possibility of an extension. The Netherlands instituted a three-week semi-lockdown with curfews. Those actions are already appearing in lower forward bookings as measured in Forward STAR. Germany has cancelled some of its Christmas markets, with more cancellations likely. The list of affected countries is expected to increase but we believe most markets are more resilient today than several months ago because of vaccination rates. Moscow, where new restrictions were put in place then relaxed, saw occupancy return quickly.

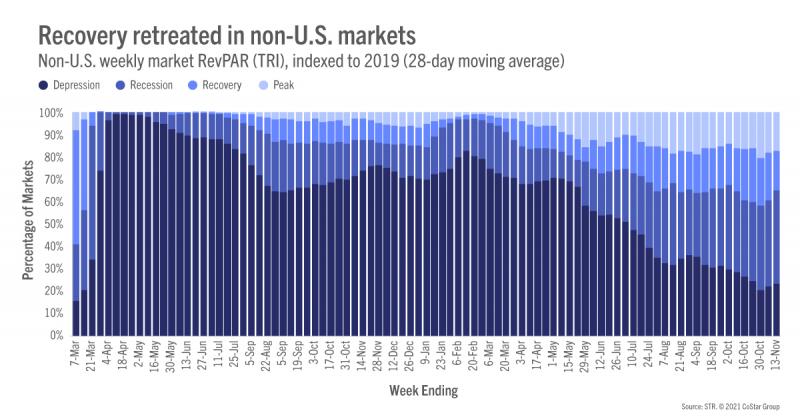

Any new disruptions will inflict more pain on the markets that were already further from recovery. Twenty-three percent of non-U.S. markets remain in “depression” and another 42% are in recession (RevPAR indexed to 2019 between 50 and 80) on a 28-day basis.

To learn more about the data behind this article and what STR has to offer, visit https://str.com/.

Sign up to receive our stories in your inbox.

Data is changing the speed of business. Investors, Corporations, and Governments are buying new, differentiated data to gain visibility make better decisions. Don't fall behind. Let us help.

Sign up to receive our stories in your inbox.

Data is changing the speed of business. Investors, Corporations, and Governments are buying new, differentiated data to gain visibility make better decisions. Don't fall behind. Let us help.