Offline beauty visits came roaring back as restrictions on brick and mortar retail began to lift in spring 2021. Since then, foot traffic has remained impressively strong. As the sector heads into a critical holiday season, we dove into the data for Ulta, Sephora, and Sally Beauty to find out how the leading beauty retailers are performing in their owned stores and in their new collaborations with Target and Kohl’s.

Visits Significantly Higher Than in 2019

Brick and mortar beauty stores suffered a double blow over the pandemic. In-store shopping accounted for over 80% of beauty-product purchases before the pandemic, which took a hit as non-essential businesses closed and consumers could no longer go to stores to discover new products. And since everyone was mostly at home – or wearing masks when out and about – the demand for makeup plummeted.

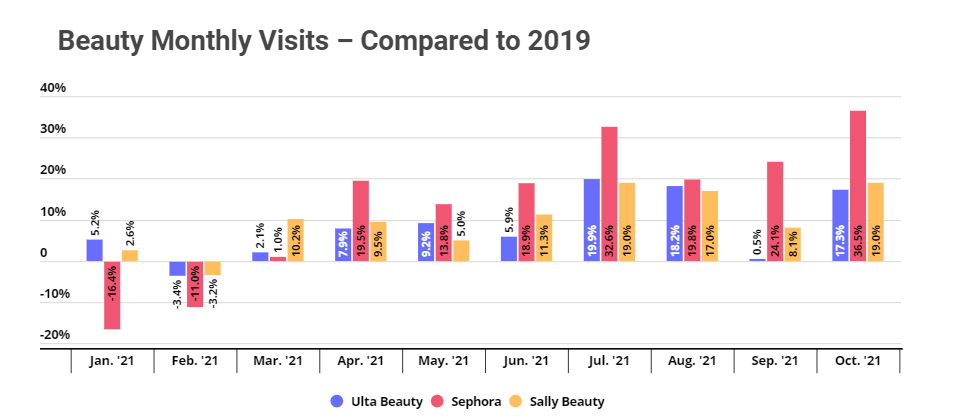

Now, the pent-up demand is leading to soaring foot traffic. Consumers who were waiting to experience a product’s scent, texture, and packaging before purchasing – or just waiting for a reason to primp again – have been visiting leading beauty retailers significantly more often than they did in 2019. Even in October, which is not a typically strong month for retailers in general, year-over-two-year visits were up by 17.3%, 36.5%, and 19.0% for Ulta Beauty, Sephora, and Sally Beauty, respectively.

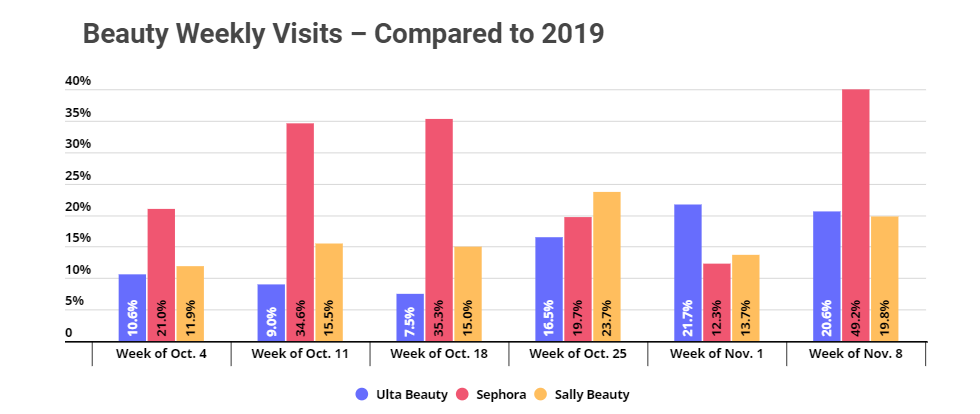

Looking at weekly visits confirms that the year-over-two-year rise in beauty visits shows no sign of slowing down, with visits for the week of November 8th were up 20.6%, 49.2%, and 19.8% for Ulta, Sephora, and Sally, respectively. Of course, the increases should be seen in the context of relatively low October-November 2019 visits due to regular seasonality, which is absent this year as consumers and retailers extend the holiday shopping season. Still, the rise in visits is massive enough to indicate that the demand for offline beauty is significantly higher than it was in 2019, and that the leading beauty brands are extremely well positioned going into 2022.

Assessing Ulta at Target and Sephora at Kohl’s

Both Ulta and Sephora launched important collaborations this past August – Ulta with Target and Sephora with Kohl’s. We compared the overall visit trends at Target and Kohl’s with the visits for the Ulta at Target and Sephora at Kohl’s locations opened in August (excluding the shops-in-shop locations that were opened in September and beyond) to understand how these collaborations are affecting foot traffic at the host brand.

Ulta at Target

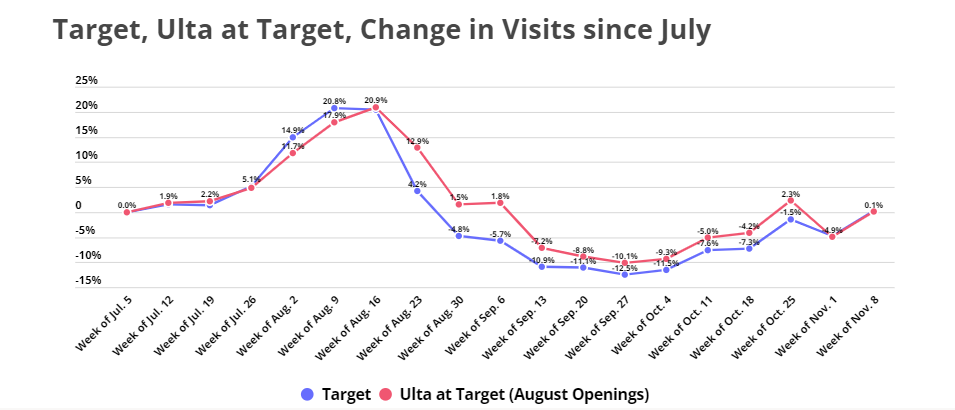

The first four Ulta shops-in-shop opened on August 6th, and the second batch of shops-in-shop opened towards the end of the month. Taking the first full week of July as a baseline, the graph below shows that the Ulta at Target collaboration appears to have yielded consistent increase in visits to Target locations with Ulta shops-in-shop.

Overall Target visit trends and visit trends to the Target locations slated to receive Ulta shops-in-shop were in line with each other throughout July. In August, Target overall visit growth even outperformed growth at the future Ulta at Target locations. But beginning the week of August 23rd – the same week that the second batch of Ulta at Target shops opened – Ulta at Target locations began to pull ahead of Target nationwide in terms of visit growth, and stayed ahead through the beginning of November.

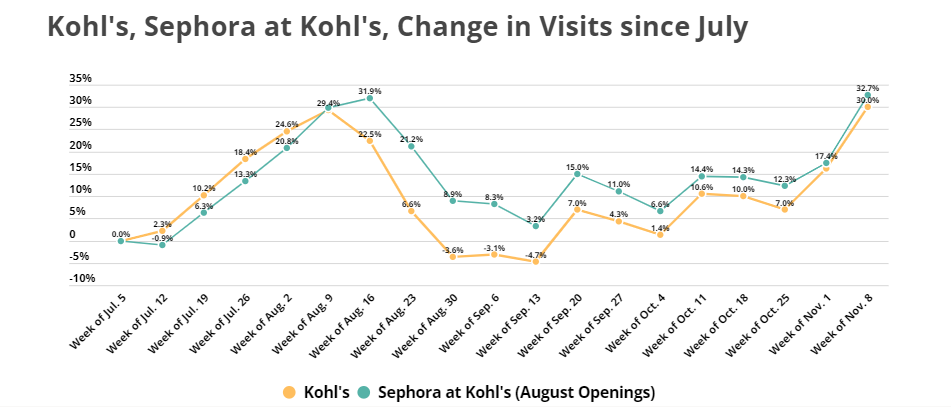

Sephora at Kohl’s

Kohl’s beauty partnership has also boosted visits for the host brand. Using the visits for the week of July 5 through 11 as a baseline shows that visits in July through mid-August grew more for nationwide Kohl’s than for Kohl’s locations slated to receive Sephora shops-in-shop. But beginning mid-August, when the first Sephora shops-in-shops opened, visits to the Sephora at Kohl’s locations shot ahead, and foot traffic to Sephora at Kohl’s continued outperforming Kohl’s nationwide through early November.

And the levelling off of Ulta at Target and Sephora at Kohl’s visit growth in early November does not necessarily mean that the excitement around these collaborations has waned. Instead, given the early start of this year’s holiday season, it is likely that the holiday-shopping related surge in overall visits is outshining the increase in visits stemming from the beauty collaborations.

What is clear, however, is the power of these collaborations to drive visit growth to stores in September and early October, a time that is not typically considered a strong retail season. As retailers continue to look for creative ways to reimagine the 21st century brick and mortar store, the rising trend of shops-in-shop seems to offer a lot of promise.

To learn more about the data behind this article and what Placer has to offer, visit https://www.placer.ai/.

Sign up to receive our stories in your inbox.

Data is changing the speed of business. Investors, Corporations, and Governments are buying new, differentiated data to gain visibility make better decisions. Don't fall behind. Let us help.

Sign up to receive our stories in your inbox.

Data is changing the speed of business. Investors, Corporations, and Governments are buying new, differentiated data to gain visibility make better decisions. Don't fall behind. Let us help.