Source: https://www.placer.ai/blog/how-are-mid-range-and-luxury-department-stores-performing-in-2022/

Department stores have been part of the American retail landscape for decades – but their role in consumers’ shopping routines is changing. We dove into foot traffic trends for leading mid-range and luxury brands to see how these iconic retailers are performing in this almost-post COVID world.

Post-COVID Recovery

COVID hit department stores particularly hard – even after non-essential business reopened, many consumers still avoided shopping indoors. By summer 2021, however, many brands, including Macy’s, Dillard’s, and Kohl’s, were nearing – and sometimes exceeding – pre-pandemic levels. But from the Omicron wave in January to the more recent economic headwinds in March and April, the start of 2022 has brought a fresh batch of challenges – and these set-backs have impacted department stores’ recovery.

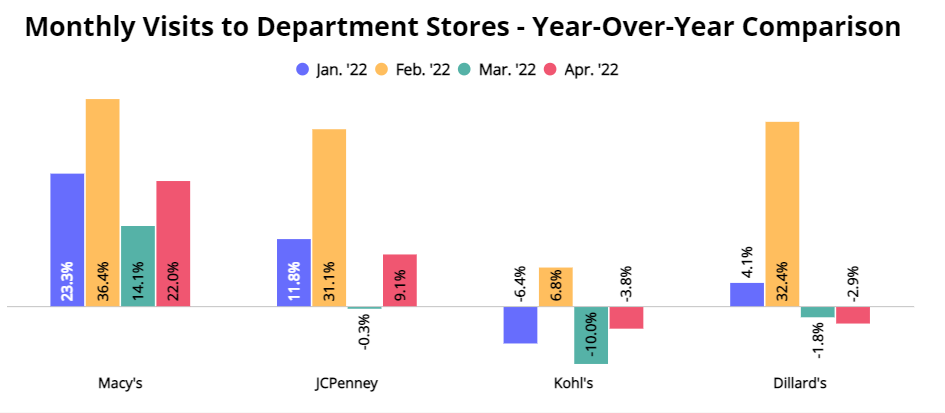

The chart below shows department store monthly foot traffic in the first four months of 2022 compared to the equivalent months in 2021.Year over year (YoY) visits in February 2022 were high for all four brands analyzed – 36.4%, 31.1%, 6.8%, and 32.4% higher for Macy’s, JCPenney, Kohl’s, and Dillard’s, respectively, compared to foot traffic in February 2021.

But with the impact of inflation in March, YoY visits dipped for JCPenney, Kohl’s and Dillard’s, which shows how fragile the department store recovery still is. But as inflation slowed down in April, department store visits climbed again, with Macy’s and JCPenney March foot traffic showing YoY growth and Kohl’s and Dillard’s visit gaps almost fully closed. This indicates that should these wider economic challenges continue to dissipate, the opportunity for department stores could be exceptional heading into a critical summer shopping season.

Department Store Visits Compared to Pre-Pandemic

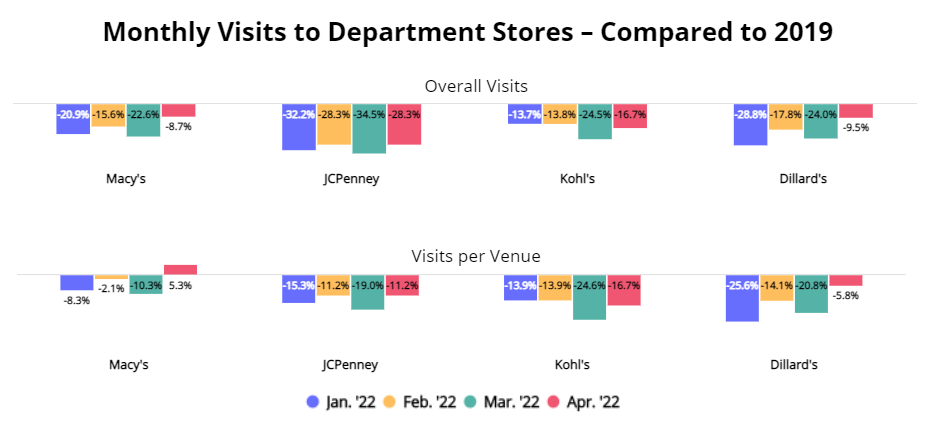

Comparing department store foot traffic to pre-pandemic trends shows just how challenging the past two years have been, and puts into context the impressive nature of the sector’s recovery. Overall visits are down across the board, and while some of the visit decrease is due to store fleet consolidation, foot traffic per remaining store is also lower than it was pre-COVID. While Macy’s year-over-three-year (Yo3Y) visits per venue were up 5.3% in April 2022, the average visits per venue for the other three brands is still catching up to 2019 levels.

These relatively low visits per venue numbers may help explain the move some of these brands are making towards smaller-format stores. Kohl’s recently announced plans to open 100 small-format stores, while Macy’s has already opened several new Market by Macy’s stores designed to give consumers a more curated and less overwhelming department store experience.

Department stores are also doubling down on the “shop-in-shops” concepts, with Kohl’s expanding its Sephora partnership and Macy’s implementing partnerships with Pandora, Toys “R” Us, and even Wetzel’s Pretzels. As department stores continue shifting their focus away from the one-stop-shop concept and towards brand and product discovery, the smaller format stores and shop-in-shops are sure to bring department stores into the post-COVID era.

Luxury Apparel Starts 2022 Off Strong

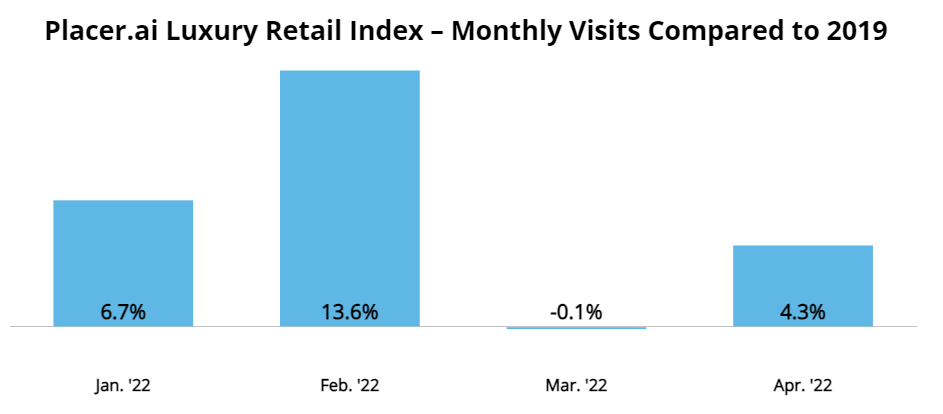

While mid-range department stores continue their recovery trajectory, luxury apparel is thriving. Our Placer.ai luxury retail index that tracks foot traffic trends for brands such as Fendi, Prada, and Chanel indicates that, despite Omicron and inflation, visits to luxury retailers have matched or exceeded pre-pandemic levels every month of 2022 so far.

Strong Recovery For Luxury Department Store Brands

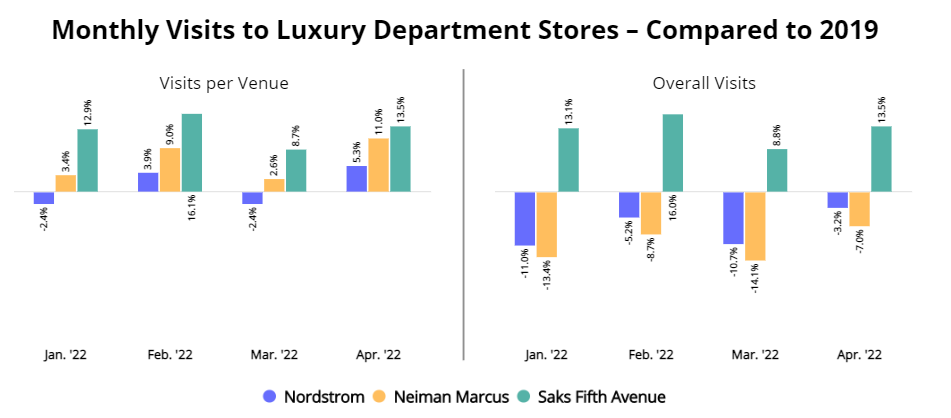

Foot traffic data indicates that luxury department stores are indeed thriving – each in its own way. Like mid-range department stores, several high-end department store brands including Neiman Marcus and Nordstrom have consolidated their store fleet over the past two years. Neiman Marcus came out of bankruptcy several stores lighter, and Nordstrom permanently closed 16 stores due to the impact of COVID. So, while overall foot traffic for these two brands is lower than it was in 2019, Yo3Y visits per venue are higher, with April 2022 visits up 5.3% and 11.0% for Nordstrom and Neiman Marcus, respectively.

And in Q1 2022, the uncontested luxury department store winner was Saks Fifth Avenue. The brand saw significant Yo3Y growth in visits every month so far in 2022, and the strong Q1 could be just the beginning. And following in Nordstrom’s footsteps, Saks recently announced a partnership with Skinney Medspa that will bring botox and other injectables to its Manhattan flagship as a pilot prior to a wider roll-out – which may give the brand a significant boost and help Saks carry its impressive growth streak throughout the rest of 2022.

Department Stores Evolving Along with Their Consumer Base

The past couple of years have been difficult for department stores. Even prior to COVID, the rise of ecommerce and the mall’s increased emphasis on DTC brands and experiential offerings have forced department stores to rethink the playbook that had served them well for so long. But these legacy brands are rising to the challenge.

Mid-range department stores are pivoting towards smaller-store formats to streamline the shopping experience and adding shop-in-shops to give customers a reason to visit in-person. Luxury brands are doubling down on their exclusive allure by consolidating their store fleet and pushing the envelope by expanding their beauty offerings to include non-surgical esthetic procedures. So while some department stores are still recovering from COVID’s impact, it seems that all the brands analyzed here are making the adjustments necessary to continue playing a key role in consumers’ shopping routines for many years to come.

To learn more about the data behind this article and what Placer has to offer, visit https://www.placer.ai/.

Sign up to receive our stories in your inbox.

Data is changing the speed of business. Investors, Corporations, and Governments are buying new, differentiated data to gain visibility make better decisions. Don't fall behind. Let us help.

Sign up to receive our stories in your inbox.

Data is changing the speed of business. Investors, Corporations, and Governments are buying new, differentiated data to gain visibility make better decisions. Don't fall behind. Let us help.