This week global scheduled airline capacity – that is, the number of seats being flown by airlines around the world – remains only 85% of where it was in the same week in 2019. Not only has there been no growth for three years, but the industry is still a significant way behind where it was. And this is an industry that had become accustomed to average annual capacity growth of 3.5% over more than 20 years.

Here at OAG we provide data for global capacity on a weekly basis and it would be easy to draw the conclusion on the basis of current figures that the industry continues to be severely challenged by the events of the past few years.

However, the third quarter earnings results for many airlines demonstrate that it’s not all bad. Many airlines were profitable in the last quarter and some even announced record profits. So, what is going on? How do we account for the difference between capacity and profit?

Results Are In, Fares Are Up

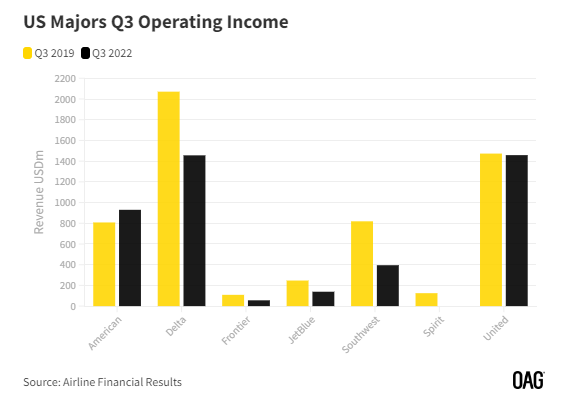

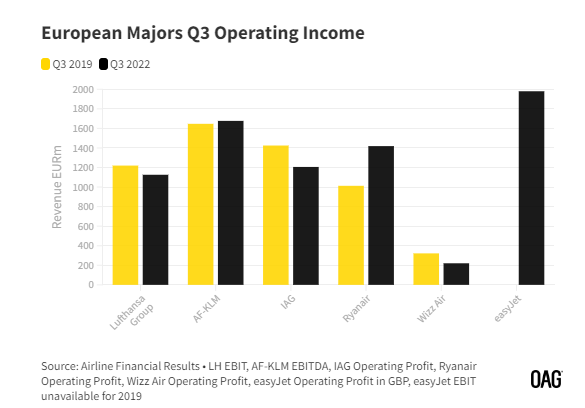

The charts below summarise the third quarter results for some of the largest airlines in the USA and Europe. Many have exceeded their performance in Q3 of 2019. In Asia, Singapore Airlines recorded its highest ever quarterly operating profit.

Of course, the most recent quarter is often the best performing; demand for travel is highest through the July-September period as the large travel markets in North America and Europe take to the skies for their annual holidays. But demand itself doesn’t make an airline profitable.

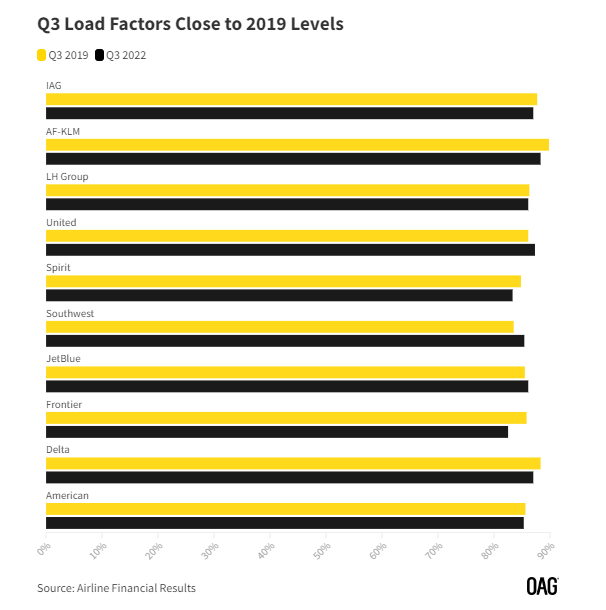

A key performance indicator for airlines is load factor, a measure of how full the aircraft are with fare-paying passengers. The higher the proportion of seats that are filled the better the economics of flying, and potentially the more profitable an airline may be. While load factors have certainly returned to pre-pandemic levels, it’s not clear that they are actually higher than before the pandemic.

The primary reason for improved profitability has been that fares have been higher. There has been anecdotal evidence all summer that fares were much higher than they’ve been, and with the financial results we can see just how much higher.

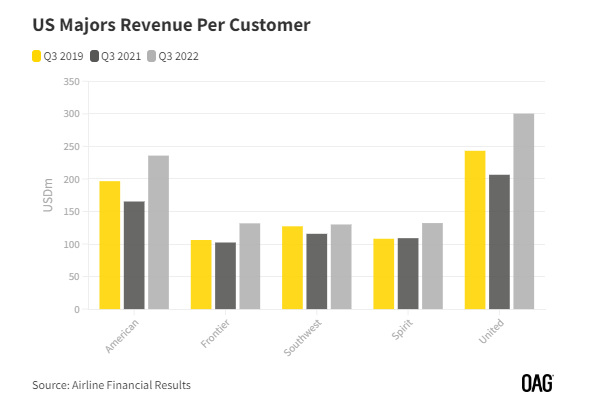

Revenue per passenger at American Airlines is 20% more than back in 2019, and the figures for Frontier, Spirit and United Airlines are even higher. So, with aircraft loads back at pre-pandemic levels but fares substantially higher, airlines can finally make some money.

All About Capacity

Fare levels are not the whole story though. Most airlines have sophisticated yield and revenue management systems which aim to achieve the highest fare possible for each seat. But this certainly hasn’t always ensured they are profitable in the past. The difference in the current environment is capacity.

All too often in the past we have talked about an industry with a problem of over-capacity, or over-supply. Airlines add capacity to gain market share. They add capacity because orders for new aircraft made at the peak of the economic cycle are delivered a few years later. New capacity comes into markets when start-up airlines start operating. Although airlines have known there is a problem of over-capacity, in reality it’s been much harder for individual airlines to exercise capacity discipline. The result has been a surfeit of seats, a rush to sell seats through lowered fares and consequently sub-optimal yields.

What is different in the present situation is that airlines have been resource constrained for much of the year. Issues that many of the industry have seen, rightly, as challenges - such as the difficulty of hiring sufficient numbers of staff - mean that their ability to operate at the scale they hoped for has been constrained. The upside of this enforced capacity discipline, when combined with the pent-up demand still evident in the market, is that airlines have been able to raise fares.

2023 Prospects

How long can this continue? Will airlines have learned from what has happened with capacity and report improved results through 2023 as well?

As we near the end of 2022, the prospect of global recession looms. This in itself will likely reduce demand for air travel as consumers feel the pinch on their disposable income and businesses tighten their belts. This will make replicating the third quarter results harder but as we’ve seen, it’s all about balancing supply and demand and achieving a price that more than covers costs. Lower demand on its own does not necessarily mean the return to profitability is over. What matters may be what happens to capacity.

At the moment, global airline capacity for the Winter 2022/23 season looks like being 9% less than in the Winter 2019/20 season. So, there is no rush to recovery compared to 2019 levels, but this does represent more capacity relative to 2019 than we’ve seen in the last quarter. The temptation for airlines as they get resourcing issues under control is to keep adding capacity as they can. In some ways the continued focus on where we are, relative to 2019, is part of the problem. If instead, we were more focussed on the coming winter having 23% more seats available than last winter we would be quicker to realize when we have returned to the old ways of over-capacity.

To learn more about the data behind this article and what OAG has to offer, visit https://www.oag.com/.

Sign up to receive our stories in your inbox.

Data is changing the speed of business. Investors, Corporations, and Governments are buying new, differentiated data to gain visibility make better decisions. Don't fall behind. Let us help.

Sign up to receive our stories in your inbox.

Data is changing the speed of business. Investors, Corporations, and Governments are buying new, differentiated data to gain visibility make better decisions. Don't fall behind. Let us help.