In an exercise of focused speculation, we kick off 2023 the way we’ve kicked off every year – with a look at the retailers and segments we think are uniquely well positioned for the year to come.

The only rule? They can’t have been on the list a year prior, and there must be at least a few “bold” predictions.

Last year, we correctly broke down the continued dominance of Target, the uniquely strong positioning for beauty leaders like Ulta and Sephora, and the recoveries for grocery leaders like H-E-B and Costco. Less “successful” calls centered around assumptions of strength for the wider department store segment, though some chains did drive impressive results. And our section focusing on chains that could surprise didn’t see the sharp recoveries we could’ve hoped for, though we may just see those returns from a bit later than expected.

So who makes the 2023 list, and how will they fare…

DTC Leaders

The shift of more product oriented companies emphasizing DTC at the expense of wholesale routes was already taking place long before the pandemic, but there’s a confluence of trends that’s making those decisions look increasingly smart.

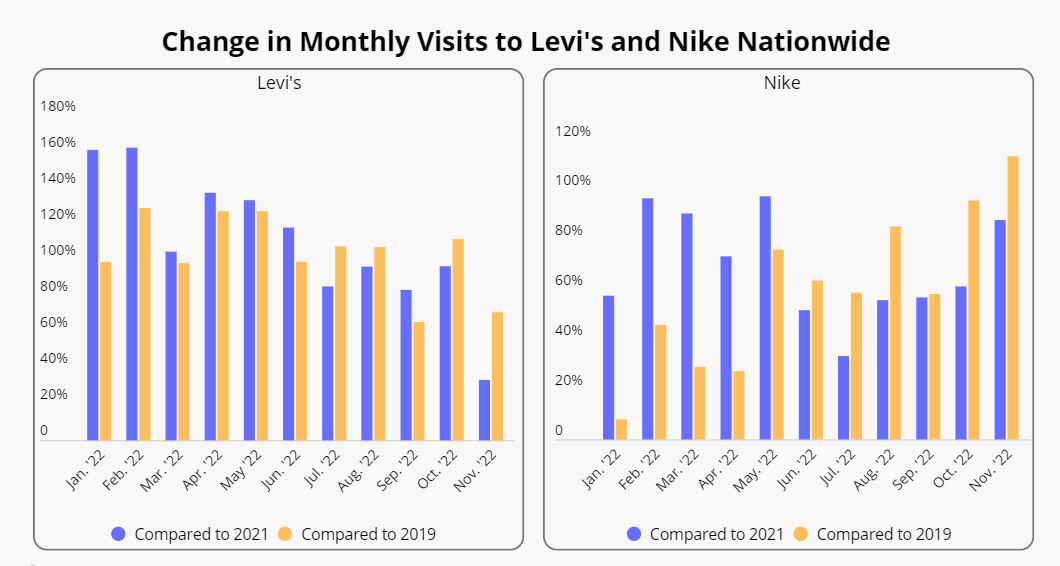

The core is a fundamental shift taking place in valuing stores beyond just sales per square foot metrics. The recognition of the impact on brand, discovery, operations, and even online sales are all driving retailers and product companies to think differently about physical retail spaces. The ability to own the brand experience in these locations and better leverage stores to drive the aforementioned goals is pushing retailers like Levi’s, Ralph Lauren and Nike to expand their retail footprint.

But, there’s also a recognition of the importance of leveraging a diversity of channels together to maximize reach by utilizing wholesale and owned channels together. This holistic perspective enables these product-oriented companies to drive growth and reach while better owning the brand relationships that will become increasingly critical for long term success.

Kings of Experience

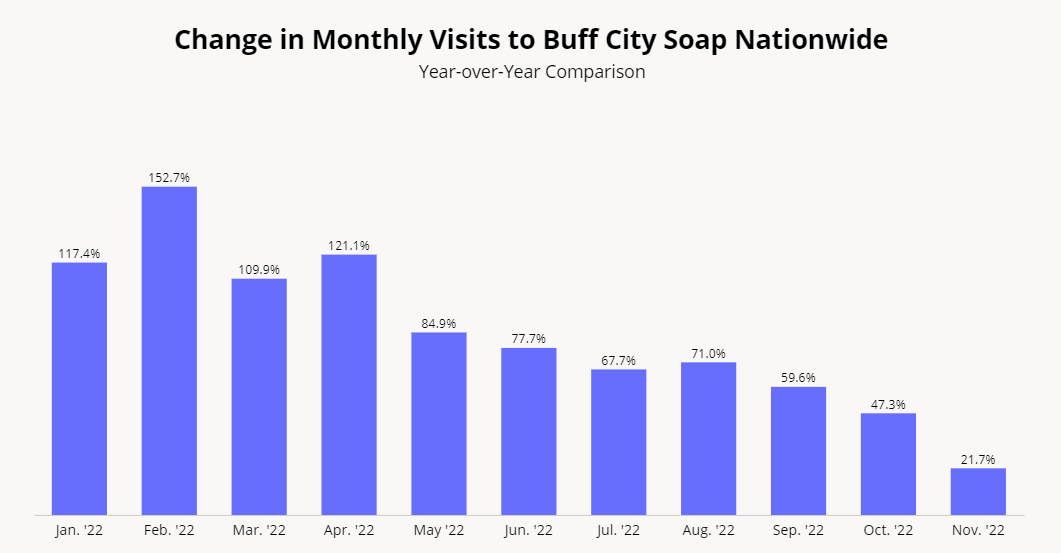

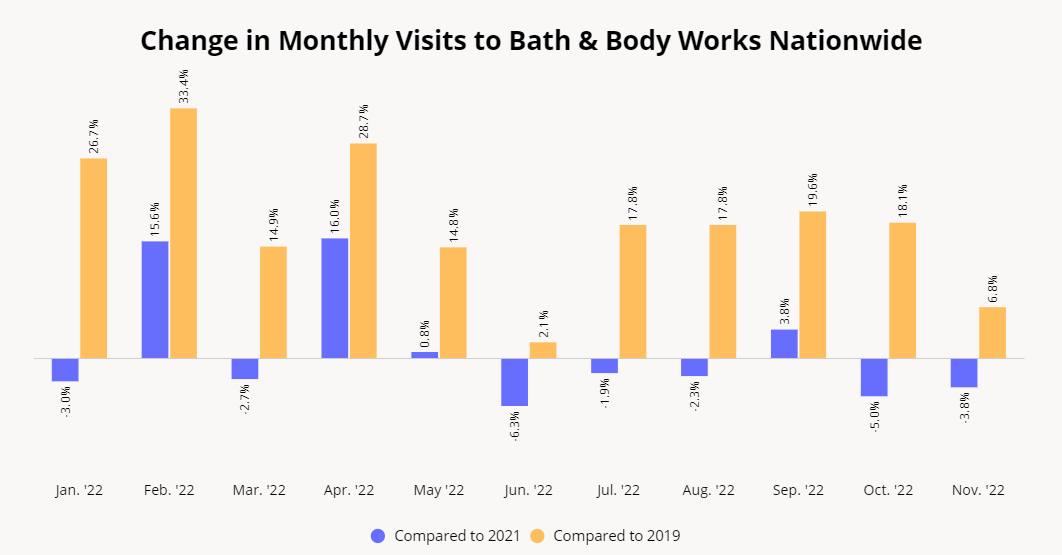

While flashier concepts may grab the headlines, the most important aspect of experiential retail may be effectively turning the regular store visit into a true experience. Bath & Body Works and Buff City Soap both exemplify this concept with the ability to try a myriad of products in the latter case even create new products of your own. Buff City has seen massive monthly year-over-year (YoY) visit growth as a result, while an already strong Bath & Body Works has seen all but three weeks in 2022 drive year-over-three-year (Yo3Y) visit increases through the week beginning December 12th.

The combination of this built-in experiential element along with tremendous trend alignment of self-care and a shift to the home remain major consumer trends should help both brands maintain the strong visit growth they have experienced in the last year.

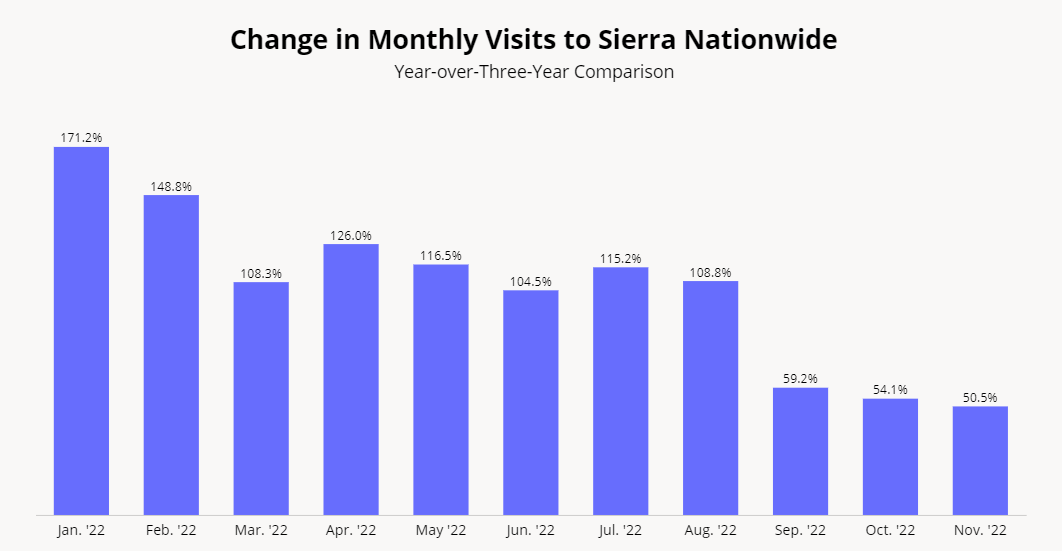

Actively Off-Price: Sierra

Sierra – the off-price outdoors and activewear brand owned by TJX – saw impressive results throughout 2022 and there is little reason to believe that success will dissipate in the new year. Not only did monthly visits grow YoY by more than 50% each month of 2022 through November, but visits per location rates were also up, showing that the expansion of stores was only one factor driving the increased demand.

Considering the continued effects of inflation, and the wider popularity both activewear and outdoors brands are experiencing, the stars could be aligning for another year of strong success.

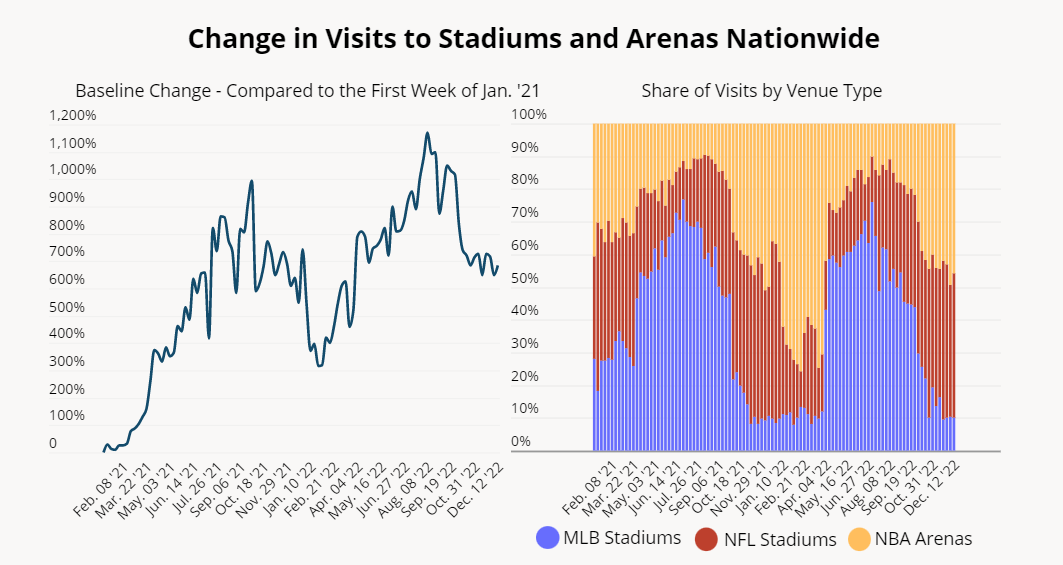

The Stadium Boost

Retail media networks are all the rage, but the implications of this growing importance go far beyond retail locations. The basic driving force behind the role of retail media networks in the brick-and-mortar environment is that a physical visit creates a uniquely powerful opportunity to create a lasting and powerful experience with a brand. And this experience applies just as much to stadiums.

Stadiums are unique for their ability to host events that regularly draw tens of thousands visitors. And the same improvement in location analytics that empower retailers to maximize visits for advertising purposes will also give teams responsible for OOH (out-of-home) advertising at stadiums far more reach. As an example, the ability to better understand who attends professional sports games – and who comes for the pregame tailgates, who focuses on the game itself, or who stays for a post-victory celebration – can help these partnership teams better communicate the unique reach that stadiums provide for experiential pop-ups and more traditional advertising. Not to mention the ability to understand the shifts based on period of the season or even in comparison to other events.

If retail media networks are really coming, and they are, the impact will not end with retail – expect stadiums and other homes to major events to be another major beneficiary.

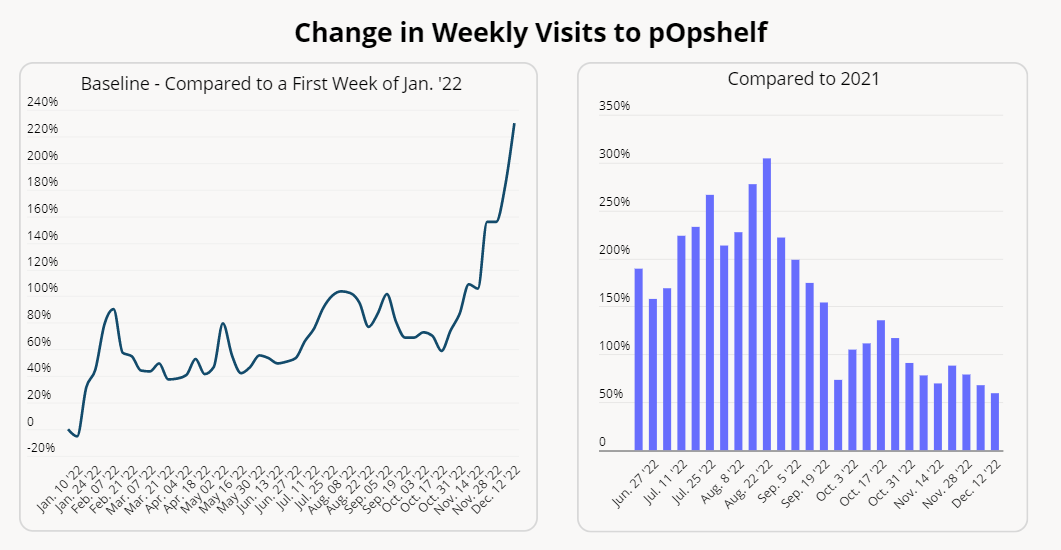

pOpshelf: Value’s Push Up

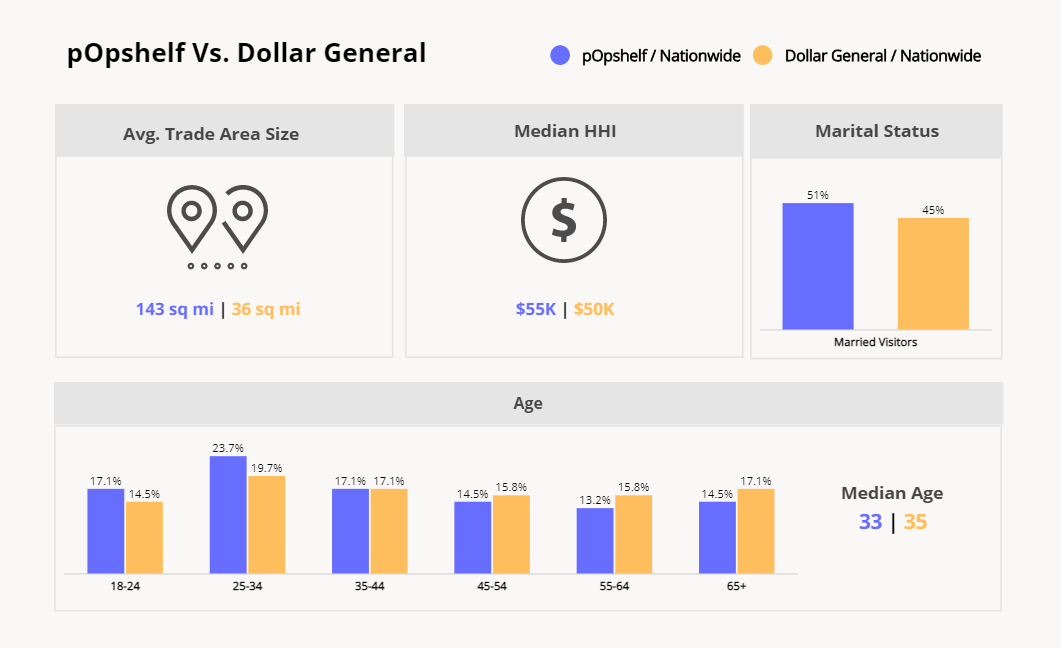

pOpshelf – the new concept from the equally strong Dollar General – has seen a massive expansion in visits as new locations continue to pop up. But the success goes deeper than just a short-term increase driven by new locations – it speaks to a savvy move by a major retailer that understands the need to speak value differently to different audiences.

pOpshelf pulls in a younger and more affluent consumer than Dollar General when looking at median age or household income (HHI), a reality that speaks volumes to the importance of the brand. Shifts like this enable a retailer that has already rapidly expanded to take a tangential step to better attract a new audience. Will there be overlap? Certainly. Does it give the brand the ability to grab visit share in a more upmarket space than it currently operates in? Absolutely. And that may be the key value – expanding the addressable market that the wider Dollar General entity can operate from within, while still staying true to the brand’s core values and business strengths.

Surprises

When looking at surprises, the big question to ask is why should a brand that is currently experiencing challenges surprise? In 2023, there are three primary drivers that demand a deeper look.

Surprises Part I: The Pull Forward of Demand

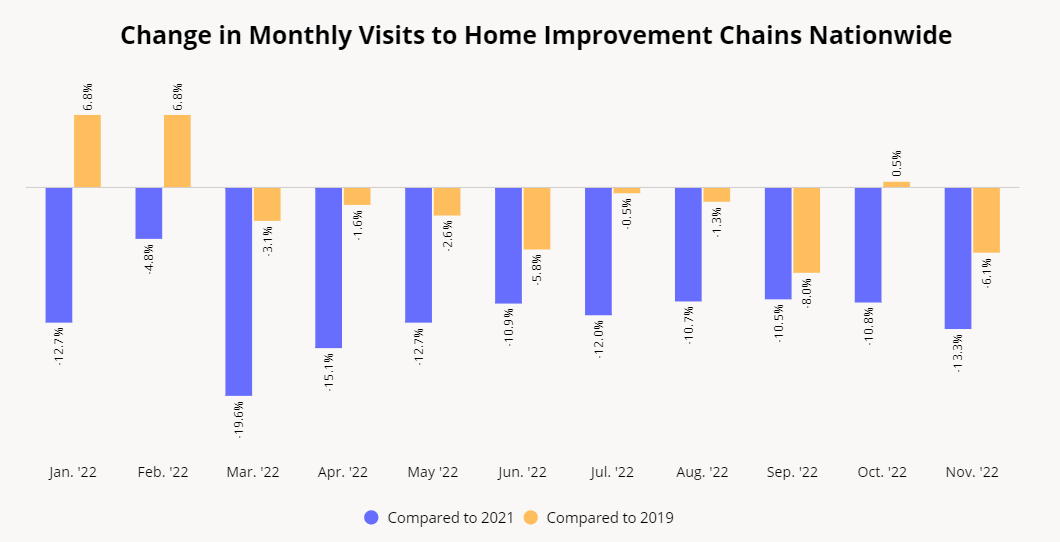

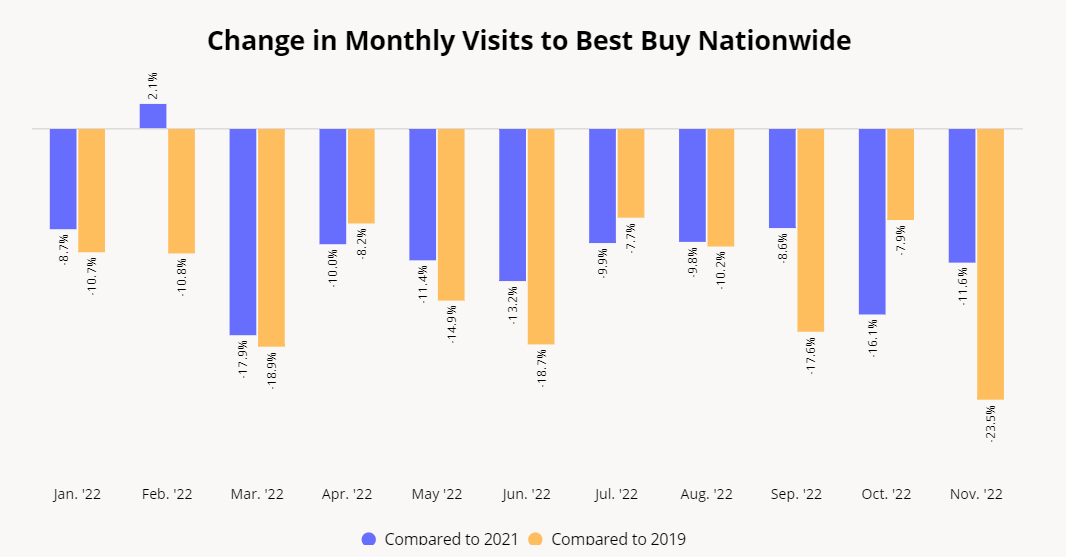

The home improvement segment and the wider consumer electronics space were among the strongest players in retail in the early stages of the pandemic. Both online and offline retail leaders led the way with strong visits and overall performance. But the uniquely beneficial environment driven by the initial stages of work-from-home (WFH), migration shifts, and added savings to spend didn’t just drive a good situation, they drove one that was potentially too good. The result was a pull forward in demand that left many consumers without the need to make new purchases in these spaces in 2022.

But even this shift has a time limit. Home improvement leaders like Home Depot and Lowe’s and consumer electronics stalwart Best Buy were among the strongest retailers pre-pandemic and in the early stages of the pandemic. And the recent challenges in visits likely speak more to the unique heights hit during that time than to any real long-term weakness – especially for chains known so much for strength in strategic decision making. So the most logical expectation is that as the impact of inflation and the pull forward of demand dissipate, the strength should return since the core drivers of the success of both groups remain unchanged.

Surprises Part II: Films and Books

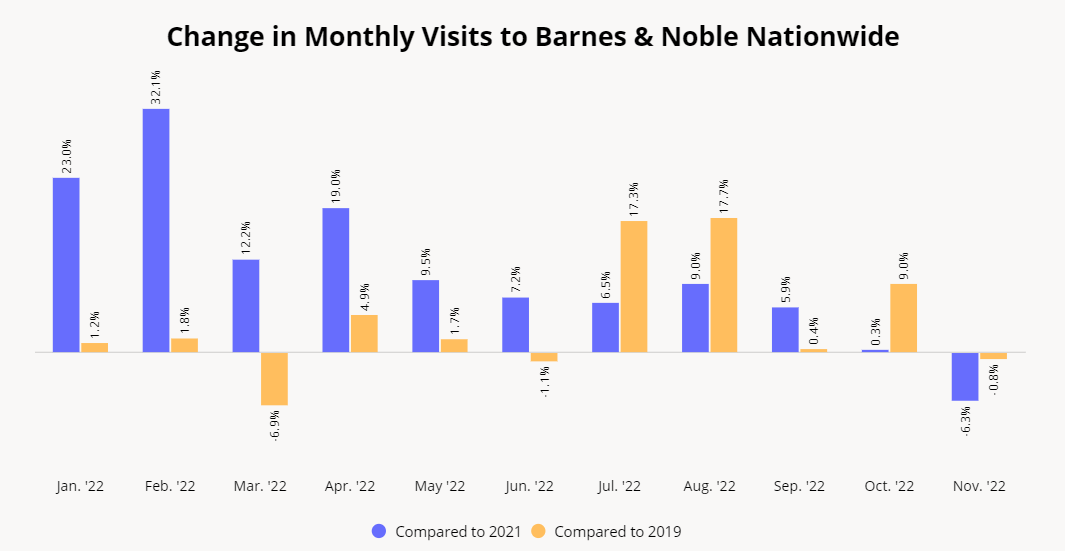

The second group of surprises to watch rests in the entertainment category. Barnes & Noble saw visits up compared to both 2019 and 2021 throughout most of 2022 and the pattern could continue as the retailer’s owner looks to continue to revamp the bookstore by enhancing its offline presence. The combination of strategic shifts to store locations and in-store experiences alongside closures from competitors should give another bump to a segment in search of a comeback.

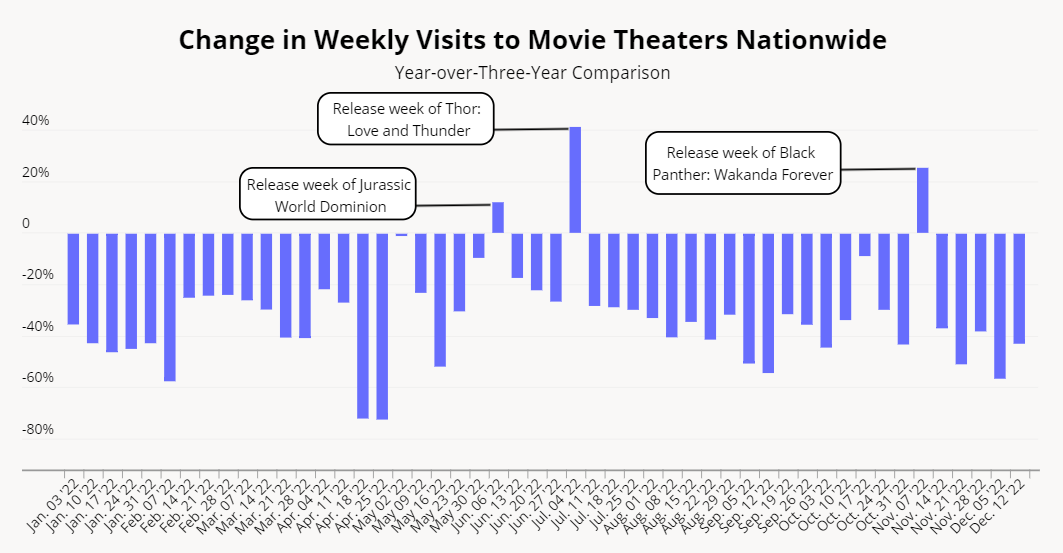

Movie theaters, another sector whose demise was likely prematurely declared, could also be positioned for better days in 2023. While visits were consistently lower than pre-pandemic levels, the drivers of growth were major blockbusters like superhero movies (Black Panther and Thor) and the reboots of major hits (Top Gun: Maverick). And what does 2023 have in store for movie lovers? Nearly a dozen movies that fit the bill with several new releases from Marvel and DC and new updates to the Rocky and Indiana Jones franchises.

Surprises Part III: Shifting Tides for the Formerly Strong

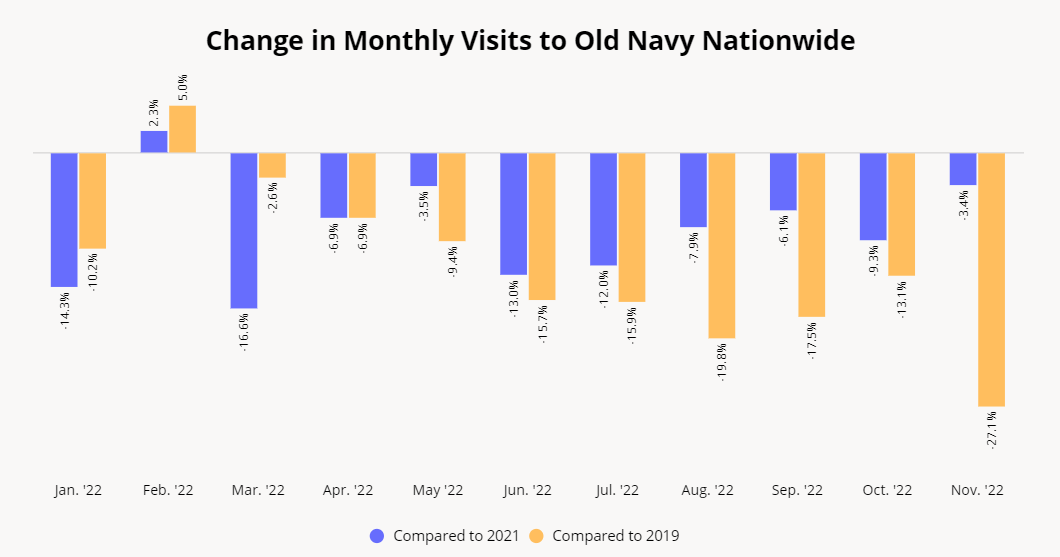

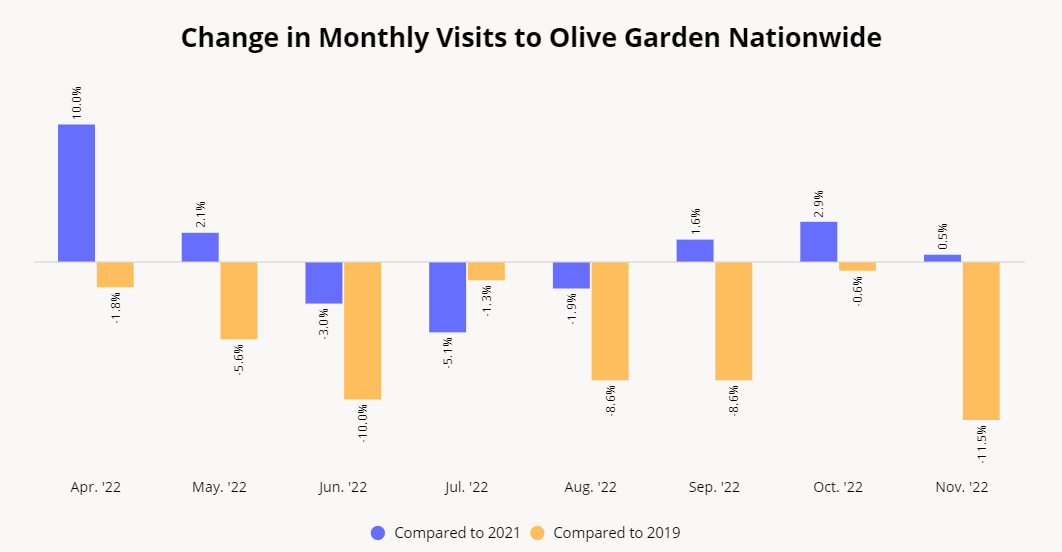

In 2019 the major narrative around Old Navy was a discussion of whether the brand needed to spin off from Gap in order to maintain its strength. In 2019, there was also a discussion of how restaurants were consistently gaining an increased share of food budgets. Both were derailed by the pandemic, but as the impact of inflation and other post-pandemic attributes decline, so should the obstacles to the success of these formerly strong players. Olive Garden has already seen visits bouncing back effectively when the opportunities present themselves, and Old Navy’s challenges – exacerbated by supply chain issues and more – should level out in the coming year. These realities position both brands to recover strongly in the coming year and surpass expectations.

To learn more about the data behind this article and what Placer has to offer, visit https://www.placer.ai/.

Sign up to receive our stories in your inbox.

Data is changing the speed of business. Investors, Corporations, and Governments are buying new, differentiated data to gain visibility make better decisions. Don't fall behind. Let us help.

Sign up to receive our stories in your inbox.

Data is changing the speed of business. Investors, Corporations, and Governments are buying new, differentiated data to gain visibility make better decisions. Don't fall behind. Let us help.