Source: https://insights.consumer-edge.com/2020/10/how-back-to-school-changes-with-no-school-to-go-back-to/

This year’s back-to-school season is unlike any in recent memory. Along with the usual school supply lists of pencils, new clothes, and lunch snacks, this year’s class also has to purchase webcams, masks, and hand sanitizer. Many schools are starting remotely, others have had in-person class dates pushed back, and several have had a later start as administrators scramble to update policies and technology. The best-in-class latency of CE Vision allows companies to track how back-to-school sales are trending almost real-time, giving a view of which industries are seeing a back-to-school boost and allowing for comparison versus competitors. Our unique demographic library allows users to filter comparison metrics for households with children, an important proxy for back-to-school spend.

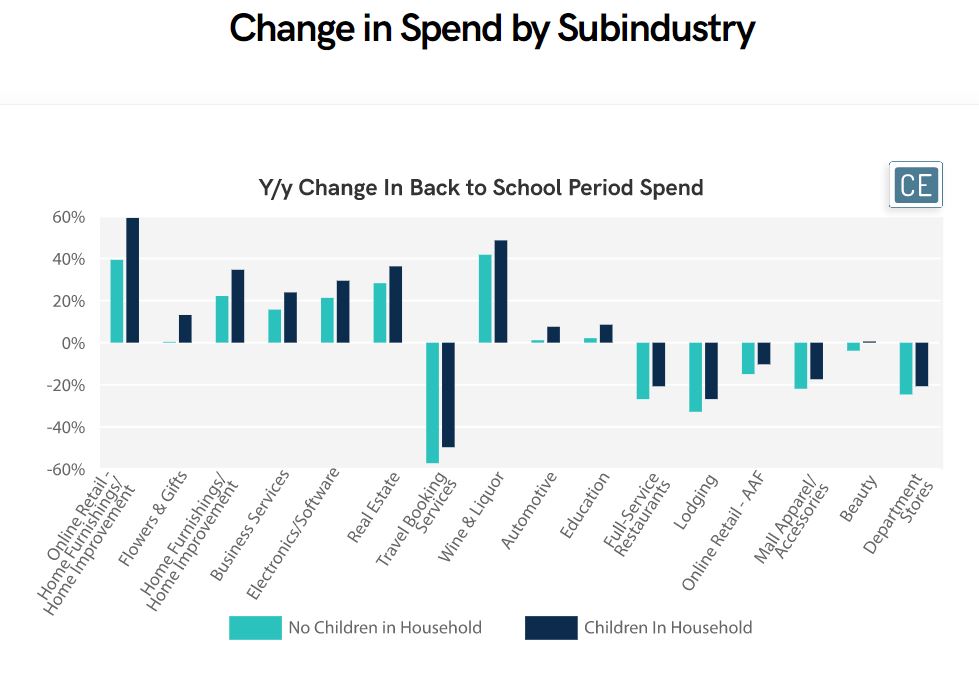

In general, back-to-school growth represents some degree of pent-up demand from spring remote learning arrangements. With many schools across the country announcing initial reopen dates that kept getting pushed back during the spring semester, some parents may have been hesitant to invest in big-ticket items like desks or computer equipment. Online Home Furnishings saw the most dramatic divergence in spend growth from households with children (our proxy for back-to-school shoppers), with sales up 35%, a double-digit gap vs. households without children. Even subindustries seeing y/y declines in spend like Online Apparel, Accessories, and Footwear, Mall Apparel/Accessories, and Department Stores saw a less sharp decline among households with children than among households without children. This implies that back-to-school is still going to be an important driver for those subindustries, even if just for kids to look good on Zoom classes.

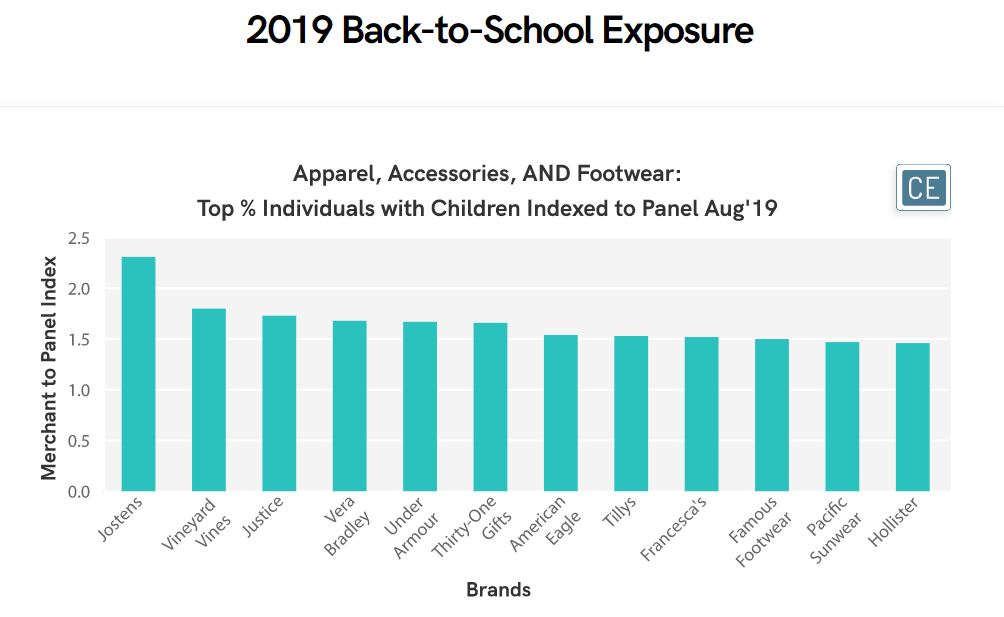

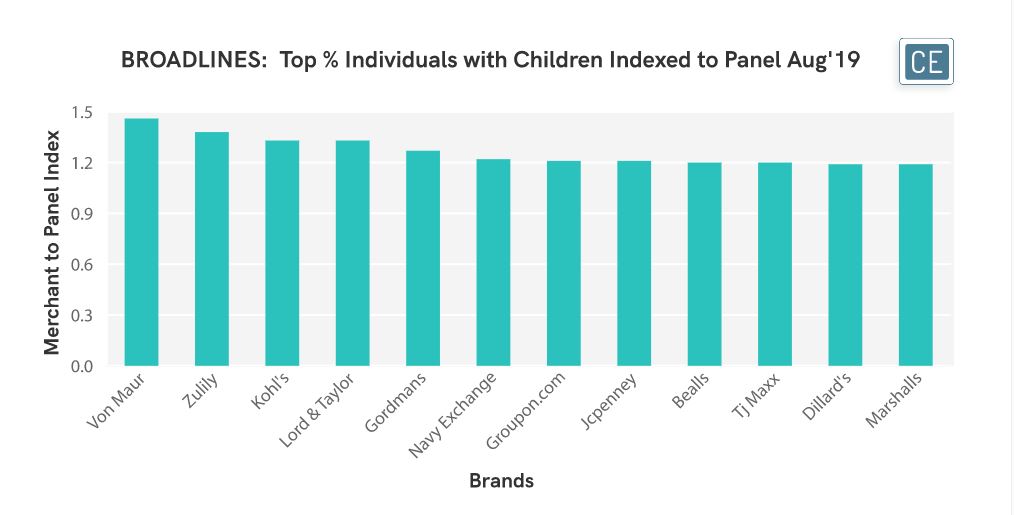

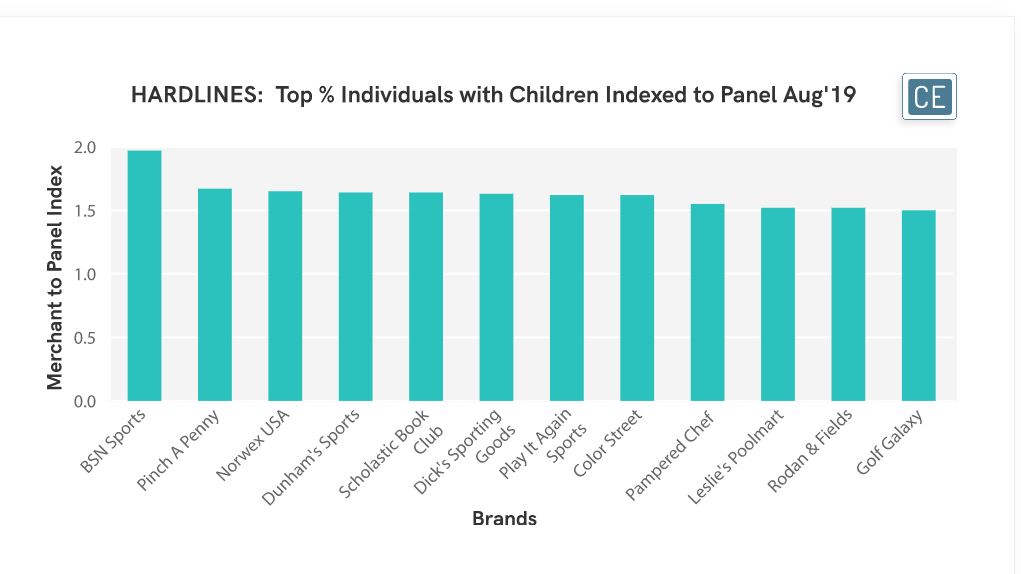

An important question is not only how back-to-school shopping is changing, but which companies are most exposed to those changes. Among clothing brands, last year Jostens had twice as large a share of its shoppers with children than the panel average, Vineyard Vines had 1.8x, and Justice had 1.7x. In broadlines, department store Von Maur had 1.5x as large a share of its shoppers with children than the panel average, Zulily had 1.4x, and Kohl’s (which has had several back-to-school seasons that outperformed its overall results) had 1.3x. In hardlines, households with children skewed more towards sporting goods for fall teams during back-to-school, with the highest overindex to households with children for BSN at almost twice the panel average, and 1.6x for Dunham’s Sports, Dick’s Sporting Goods, and Play It Again Sports.

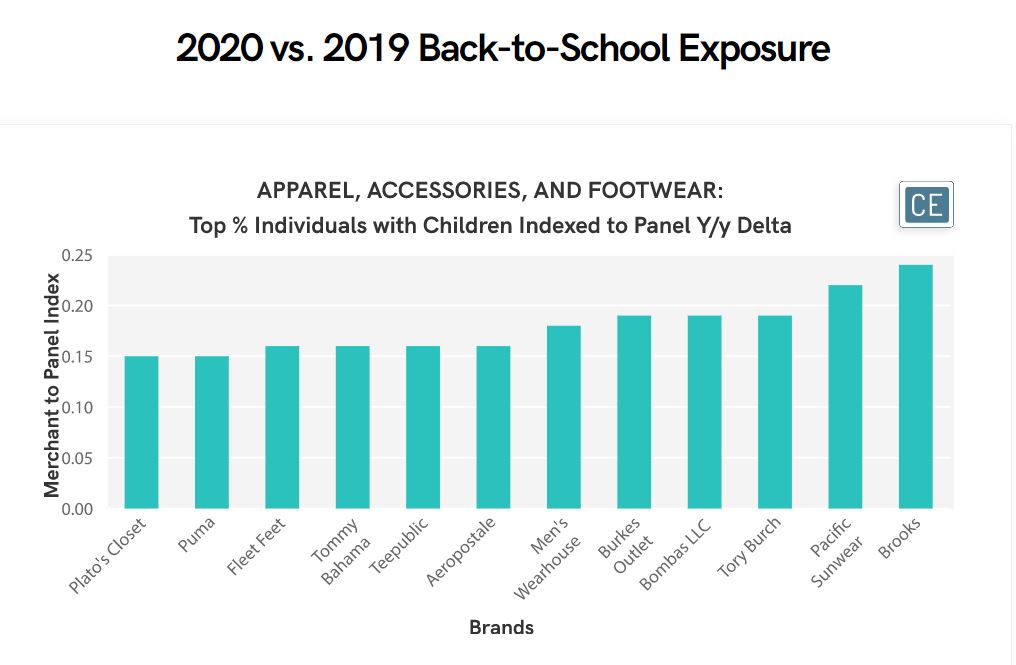

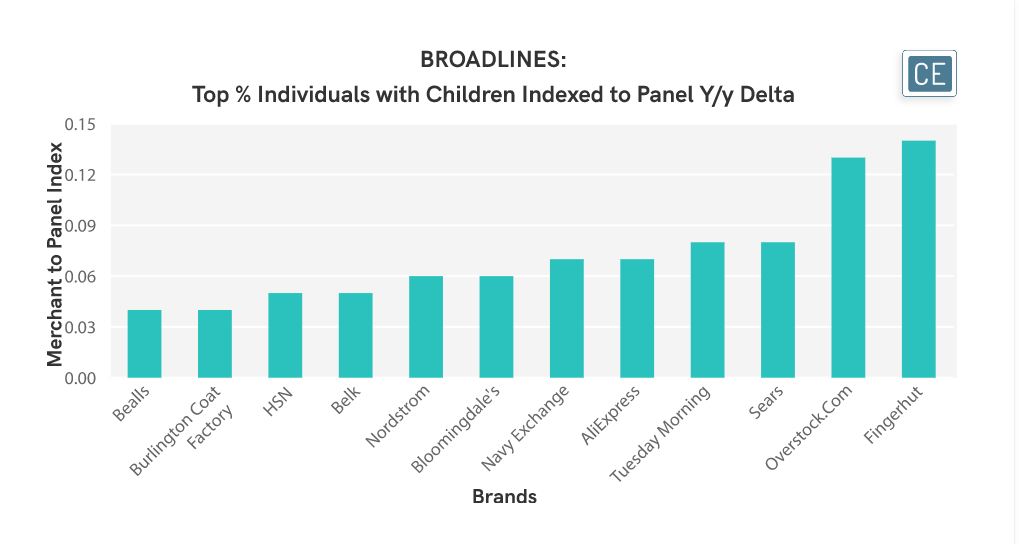

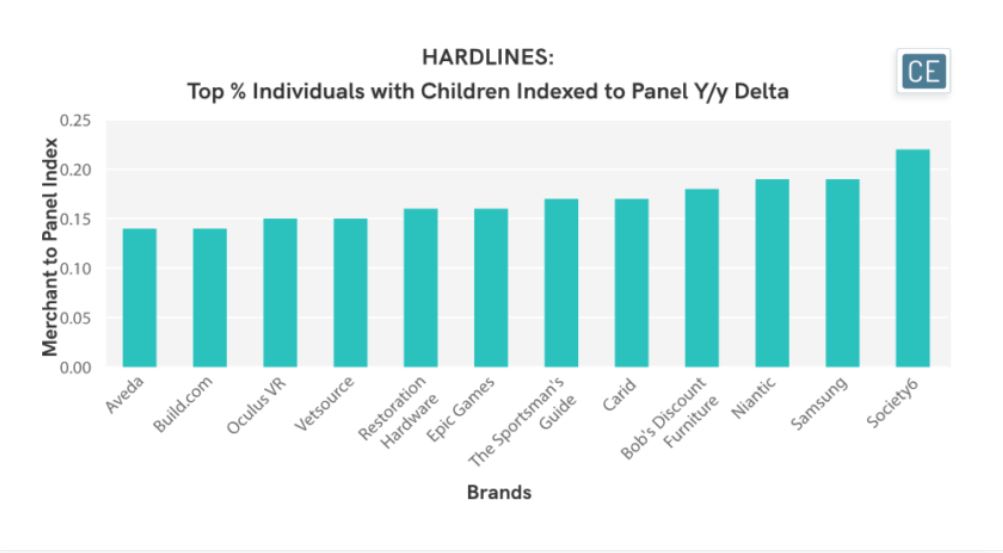

This exposure to back-to-school shoppers changed for many companies in 2020. In apparel, the companies that increased their exposure to back-to-school sales the most due to a higher percentage of shoppers with children were Brooks running shoes (not surprising given the sporting goods skew mentioned earlier) and Pacific Sunwear. In broadlines, the biggest increases in exposure came for discount sites Fingerhut and Overstock.com. In hardlines, there was a shift to more exposure for electronic brands, with Samsung and Niantic showing the largest deltas after housewares brand Society 6

To learn more about the data behind this article and what Consumer Edge Research has to offer, visit www.consumer-edge.com.

Sign up to receive our stories in your inbox.

Data is changing the speed of business. Investors, Corporations, and Governments are buying new, differentiated data to gain visibility make better decisions. Don't fall behind. Let us help.

Sign up to receive our stories in your inbox.

Data is changing the speed of business. Investors, Corporations, and Governments are buying new, differentiated data to gain visibility make better decisions. Don't fall behind. Let us help.