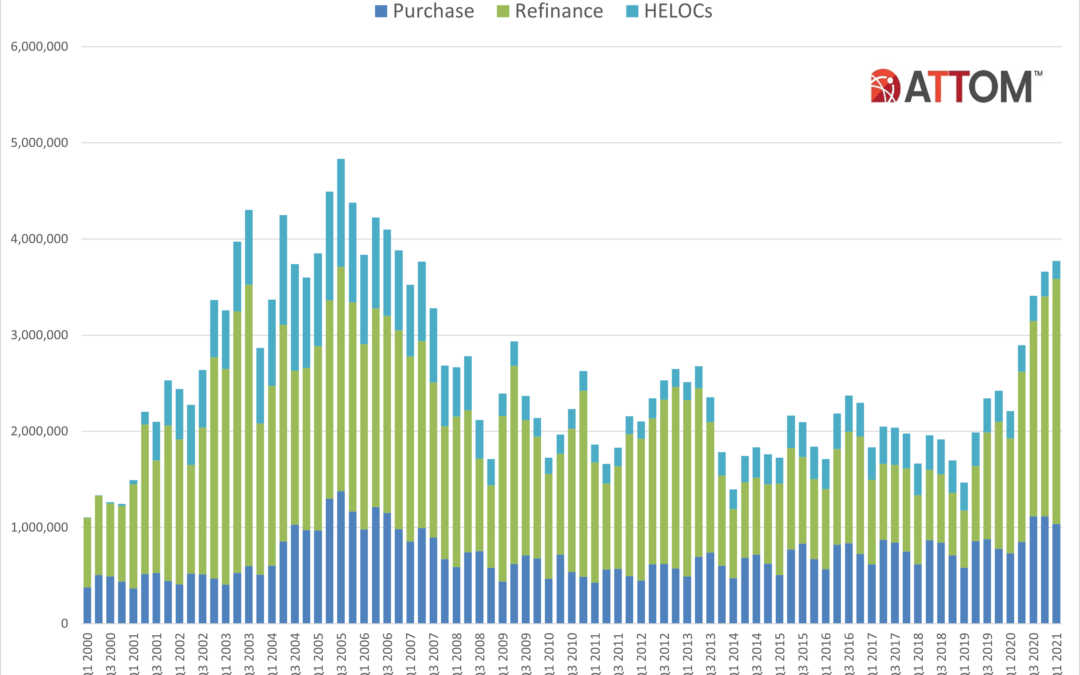

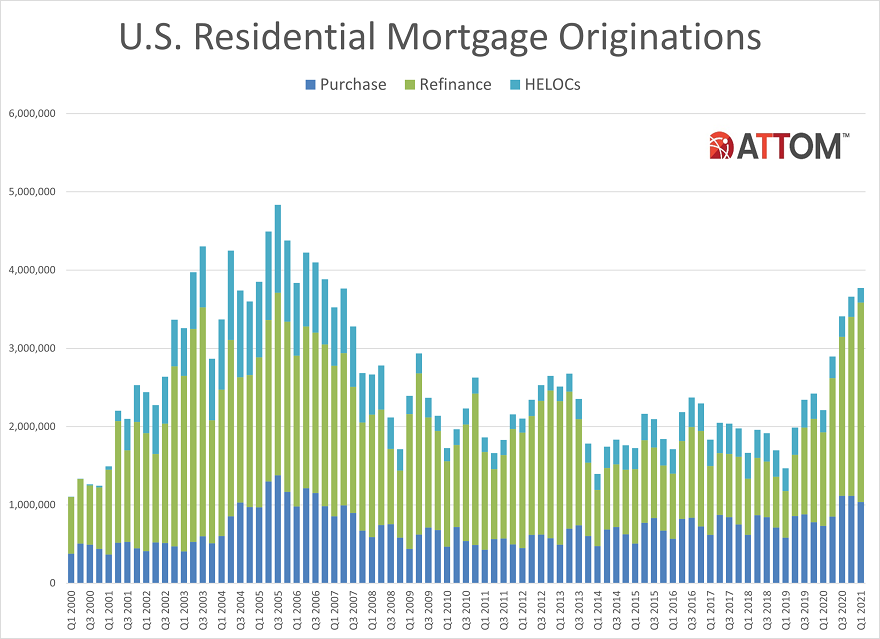

ATTOM Data Solutions, curator of the nation’s premier property database, today released its first-quarter 2021 U.S. Residential Property Mortgage Origination Report, which shows that 3.77 million mortgages secured by residential property (1 to 4 units) were originated in the first quarter of 2021 in the United States. That figure was up 3 percent from the previous quarter and 71 percent from the first quarter of 2020 – to the highest level in more than 14 years. The increase also marked the first time that the total number of home mortgages rose from a fourth-quarter period to a first-quarter period since 2009.

With residential mortgage interest rates remaining around 3 percent for most purchase and refinance loans, lenders issued $1.16 trillion worth of mortgages in the first quarter of 2021 – up 5 percent from the fourth quarter of 2020 and 81 percent from a year ago, to the largest quarterly amount since at least 2000.

The continued increase in mortgage activity during the first quarter of 2021 resulted from the latest jump in refinance mortgages, which outpaced declines in home-purchase lending and home-equity lines of credit. Refinance lending has more than doubled over the past year.

The 2.55 million home mortgages that lenders refinanced in the first quarter of 2021 represented a 12 percent increase over the fourth quarter of 2020 and a 113 percent spike over the first quarter of 2020. The dollar amount of refinance loans rose to $777.5 billion, a 14 percent increase from the previous quarter and a 114 percent jump from a year ago.

Homeowners taking advantage of low interest rates to roll over old mortgages into new ones continued to comprise the majority of home loans in the first quarter of 2021. They accounted for 68 percent of all home loans, up from 62 percent in the fourth quarter of 2020 and 54 percent in the first quarter of 2020, to the highest level since the first quarter of 2013.

That contrasted with home-purchase lending, which decreased 7 percent from fourth quarter of 2020 and home-equity-credit-line activity, which went down 27 percent. Dollar volumes of purchase and HELOC lending also declined, by 6 percent and 34 percent, respectively. While the number of loans issued to buyers dropped less than usual for a first-quarter period, as declines in both purchase-mortgage and HELOC activity fell more in line with what usually happens during the first quarter of the year.

The overall strong home-lending numbers in the first quarter of this year represented yet another measure of how the U.S. housing market has staved off financial damage caused by the ongoing worldwide Coronavirus pandemic. Job losses have hit middle- and upper-income households less than others, leaving them more able to take advantage of low interest rates to buy homes or refinance their mortgages.

“Homeowners lined up to refinance their loans in ever-growing numbers during the first quarter of 2021, making for a highly unusual quarterly increase in total lending activity for that time of year. The home-mortgage industry almost always slows down in Winter, but not this year because of so many homeowners hopping on super-low interest rates to reduce their monthly payments,” said Todd Teta, chief product officer at ATTOM Data Solutions. “Eventually, the refi side of the lending business will ease up after enough homeowners get in on the good deals. But there’s no sign of that happening in the very near future – yet another indicator of how the housing market remains strong amid uncertain economic times connected to the pandemic.”

Refinance mortgage originations up 12 percent from fourth quarter

Lenders issued 2,549,126 residential refinance mortgages in the first quarter of 2021 – the most since the third quarter of 2003. The latest figure was up 11.6 percent from the fourth quarter of 2020 and 113.2 percent from the first quarter of last year. The dollar volume of refinance packages rose to $775.5 billion in the first quarter of 2021, up 13.6 percent from the previous quarter and 114.1 percent from a year ago.

Refinancing activity increased from the fourth quarter of 2020 to the first quarter of 2021 in 166, or 78.7 percent, of the 211 metropolitan statistical areas around the country that had a population greater than 200,000 and at least 1,000 total loans in the first quarter of 2021. Activity rose by at least 10 percent in 114 metro areas (54 percent). The largest quarterly increases were in Jackson, MS (up 92.9 percent); Springfield, MA (up 59.5 percent); Medford, OR (up 57.3 percent); Buffalo, NY (up 55 percent) and Macon, GA (up 53.3 percent).

Other than Buffalo, metro areas with a population of least 1 million that had the biggest increases in refinance activity from the fourth quarter of 2020 to the first quarter of 2021 were Las Vegas, NV (up 37.2 percent); Milwaukee, WI (up 31.8 percent); Atlanta, GA (up 31.3 percent) and Providence, RI (up 31.2 percent).

Counter to the national trend, metro areas with the biggest declines in refinancing loans from the fourth quarter of 2020 to the first quarter of 2020 were Ann Arbor, MI (down 54.5 percent); Syracuse, NY (down 28.5 percent); Pittsburgh, PA (down 23.1 percent); Des Moines, IA (down 21.8 percent) and Lubbock, TX (down 18.8 percent).

Aside from Pittsburgh, metro areas with a population of at least 1 million where refinance mortgages decreased most from the fourth quarter to the first quarter were Houston, TX (down 16.6 percent); St. Louis, MO (down 14.6 percent); San Antonio, TX (down 7.3 percent) and Washington, DC (down 5.8 percent).

Refinance lending represents at least 75 percent of all loans in 20 metro areas

Refinance mortgages accounted for at least three-quarters of all loans in 20 (9.5 percent) of the 211 metro areas with sufficient data.

Metro areas with a population of at least 1 million where refinance loans represented the largest portion of all mortgages in the first quarter of 2021 were Atlanta, GA (85.3 of all mortgages); Detroit, MI (76.3 percent); Boston, MA (75.6 percent); Buffalo, NY (75.6 percent) and Washington, DC (75.6 percent).

Metro areas with a population of at least 1 million where refinance loans represented the smallest portion of all mortgages in the first quarter of 2021 were Oklahoma City, OK (55.2 percent of all mortgages); Miami, FL (58.1 percent); Salt Lake City, UT (60.1 percent); Tampa, FL (60.2 percent) and Las Vegas, NV (61.1 percent).

Purchase originations dip at relatively small pace in first quarter

Lenders originated 1,036,934 purchase mortgages in the first quarter of 2021. While that was down 7.2 percent from the fourth quarter of last year, the decrease represented the second-smallest decline in any fourth-quarter-to-first-quarter period during the past 16 years. Measured year over year, purchase loans were still up 41.7 percent over the first quarter of 2020.

Residential purchase mortgage originations decreased from the fourth quarter of 2020 to the first quarter of 2021 in 126 of the 211 metro areas in the report (59.7 percent). The largest quarterly decreases were in Buffalo, NY (down 65.1 percent); Atlanta, GA (down 56.2 percent); Ann Arbor, MI (down 54.9 percent); Augusta, GA (down 49.4 percent) and Springfield, IL (down 41.7 percent).

Aside from Buffalo and Atlanta, metro areas with a population of at least 1 million and the biggest quarterly decreases in purchase originations in the first quarter of 2021 were St. Louis, MO (down 34.4 percent); Indianapolis, IN (down 33 percent) and Houston, TX (down 31.8 percent).

Counter to the national trend, residential purchase-mortgage lending increased from the fourth quarter of 2020 to the first quarter of 2021 in 85 of the 211 metro areas in the report (40.3 percent). The largest increases were in Sioux Falls, SD (up 168.2 percent); Lake Charles, LA (up 70.2 percent); Honolulu, HI (up 46.4 percent); Gainesville, FL (up 42.5 percent) and Daphne-Fairhope, AL (up 35.9 percent).

Metro areas with a population of at least 1 million where purchase originations increased most in the first quarter of 2021 were Orlando, FL (up 29 percent); Miami, FL (up 24.5 percent); Baltimore, MD (up 24 percent); Tucson, AZ (up 17.3 percent) and Nashville, TN (up 16.5 percent).

Metro areas with a population of at least 1 million where purchase loans represented the largest portion of all mortgages in the first quarter of 2021 were Oklahoma City, OK (40.6 percent of all mortgages); Miami, FL (37.7 percent); Las Vegas, NV (36.1 percent); Jacksonville, FL (35.1 percent) and Tampa, FL (34.9 percent).

Metro areas with a population of at least 1 million where purchase loans represented the smallest portion of all mortgages in the first quarter of 2021 were Buffalo, NY (9.7 percent of all mortgages); Atlanta, GA (12.8 percent); Boston, MA (16.7 percent); Detroit, MI (18.1 percent) and Raleigh, NC (18.5 percent).

HELOC lending down 27 percent from the prior quarter

A total of 187,029 home-equity lines of credit (HELOCs) were originated on residential properties in the first quarter of 2021, down 27 percent from the previous quarter and down 34.2 percent from a year earlier. The latest count marked the lowest point since the first quarter of 2013. The dollar volume of HELOC loans dropped to $37.76 billion, a 33.7 percent decline from the fourth quarter of 2020 to the first quarter of 2021. That was the largest quarterly decrease since at least 2000.

Residential HELOC mortgage originations decreased from the fourth quarter of 2020 to the first quarter of 2021 in 73.7 percent of metropolitan statistical areas analyzed for this report. The largest decreases included Rockford, IL (down 88.9 percent); Shreveport, LA (down 69.7 percent); Ann Arbor, MI (down 67.6 percent); Madison, WI (down 66.8 percent) and Charleston, SC (down 65.2 percent).

Counter to the national trend, residential HELOC mortgage originations stayed the same or increased from the fourth quarter of 2020 to the first quarter of 2021 in 26.3 percent of metro areas analyzed for the report. The biggest increases included Palm Bay, FL (up 129.4 percent); Florence, SC (up 60.5 percent); Reading, PA (up 53.5 percent); Reno, NV (up 41.9 percent) and Gulfport, MI (up 38.6 percent).

FHA loan share dips

Mortgages backed by the Federal Housing Administration (FHA) accounted for 338,214, or 9 percent of all residential property loans originated in the first quarter of 2021. That was down from 10.6 percent in the fourth quarter of 2020 and from 12.6 percent in the first quarter of 2020.

Residential loans backed by the U.S. Department of Veterans Affairs (VA) accounted for 317,605, or 8.4 percent, of all residential property loans originated in the first quarter of 2021, down from 8.5 percent in the previous quarter and 10.1 percent a year ago.

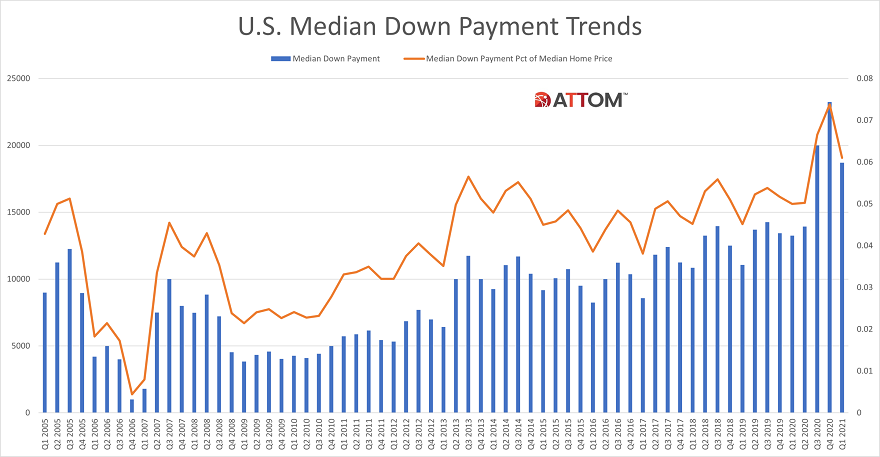

Median down payments and amounts borrowed decrease

The median down payment on single-family houses and condos purchased with financing in the first quarter of 2021 was $18,700, down 19.6 percent from $23,250 in the previous quarter but still up 41.1 percent from $13,250 in the first quarter of 2020. The latest figure marked the first decrease since the first quarter of last year.

The median down payment of $18,700 represented 6.1 percent of the median sales price for homes purchased with financing during the first quarter of 2021, down from 7.4 percent in the previous quarter but up from 5 percent a year earlier.

Among homes purchased in the first quarter of 2021, the median loan amount was $260,587. That was down 4.5 percent from the previous quarter but up 12.9 percent from the first quarter of 2020.

Report methodology

ATTOM Data Solutions analyzed recorded mortgage and deed of trust data for single-family homes, condos, town homes and multi-family properties of two to four units for this report. Each recorded mortgage or deed of trust was counted as a separate loan origination. Dollar volume was calculated by multiplying the total number of loan originations by the average loan amount for those loan originations.

To learn more about the data behind this article and what Attom Data Solutions has to offer, visit https://www.attomdata.com/.

Sign up to receive our stories in your inbox.

Data is changing the speed of business. Investors, Corporations, and Governments are buying new, differentiated data to gain visibility make better decisions. Don't fall behind. Let us help.

Sign up to receive our stories in your inbox.

Data is changing the speed of business. Investors, Corporations, and Governments are buying new, differentiated data to gain visibility make better decisions. Don't fall behind. Let us help.