Loan Performance Insights Report Highlights: January 2022

In January 2022, 3.3% of home mortgages were in some stage of delinquency (30 days or more past due, including those in foreclosure), which was a 2.3-percentage point decrease from January 2021 according to the latest CoreLogic Loan Performance Insights Report . This is the lowest recorded overall delinquency rate in the U.S. since at least January 1999.

Overall Delinquency Rates

The share of mortgages that were 30 to 59 days past due — considered early-stage delinquencies — was 1.2% in January 2022, down from 1.3% in January 2021. The share of mortgages 60 to 89 days past due was 0.3% in January 2022, down from 0.5% in January 2021.

The serious delinquency rate — defined as 90 days or more past due, including loans in foreclosure — was 1.8% in January, down from 3.8% in January 2021. While the foreclosure rate declined to 0.2% from 0.3% January 2021, the expiration of moratoriums in some states caused the number of foreclosures to rise from December 2021. Nevertheless, the January 2022 foreclosure rate was flat from December and is still the lowest recorded since at least 1999.

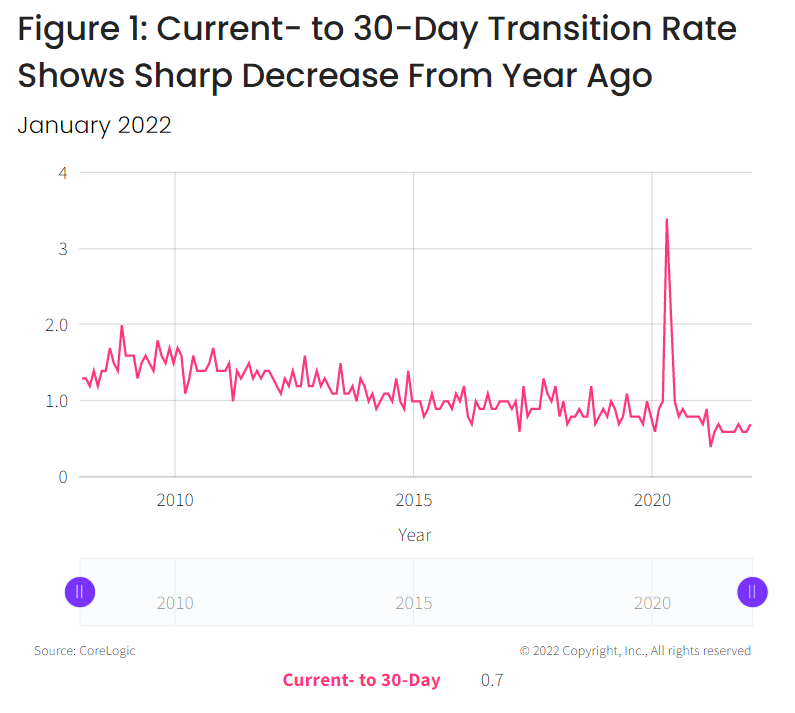

Stage of Delinquency: Rate of Transition

In addition to delinquency rates, CoreLogic tracks the rate at which mortgages transition from one stage of delinquency to the next, such as going from current to 30 days past due (Figure 1).

The share of mortgages that transitioned from current to 30 days past due was 0.7% in January 2022 — unchanged since January 2021. Low transition rates indicate that while the rate of mortgages in any stage of delinquency remained elevated, fewer borrowers slipped into delinquency than at the peak of delinquency rates in 2020.

State and Metro Level Delinquencies

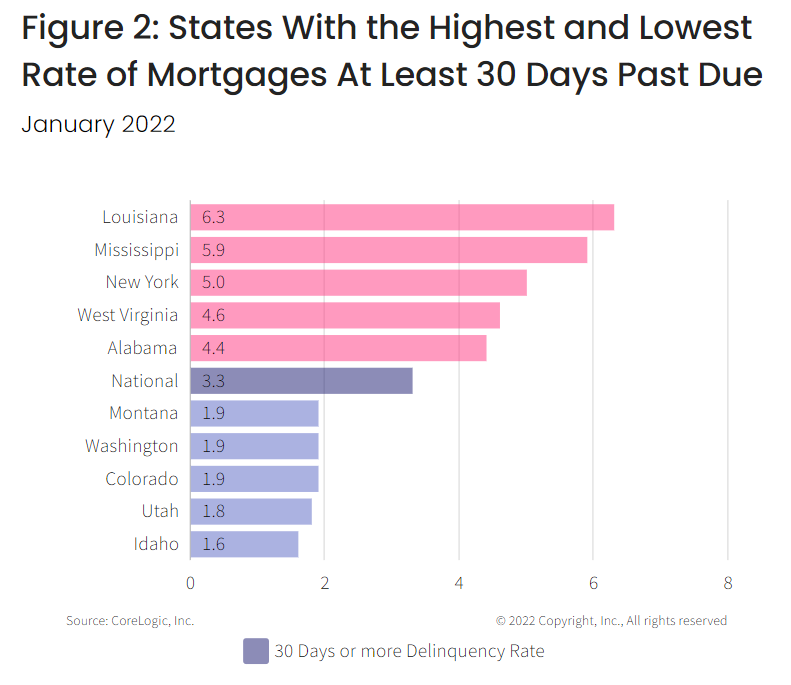

All states posted annual decreases in their overall delinquency rates in January 2022 as the employment picture improved across the country compared to a year earlier. Figure 2 shows the states with the highest and lowest share of mortgages 30 days or more delinquent. In January 2022, that rate was highest in Louisiana at 6.3% and lowest in Idaho at 1.6%. Idaho has had one of the strongest job recoveries in the U.S. and Louisiana has had one of the weakest. As of January 2022, Idaho had recovered all the jobs lost in March and April 2020 while Louisiana had only recovered 68% of jobs lost.

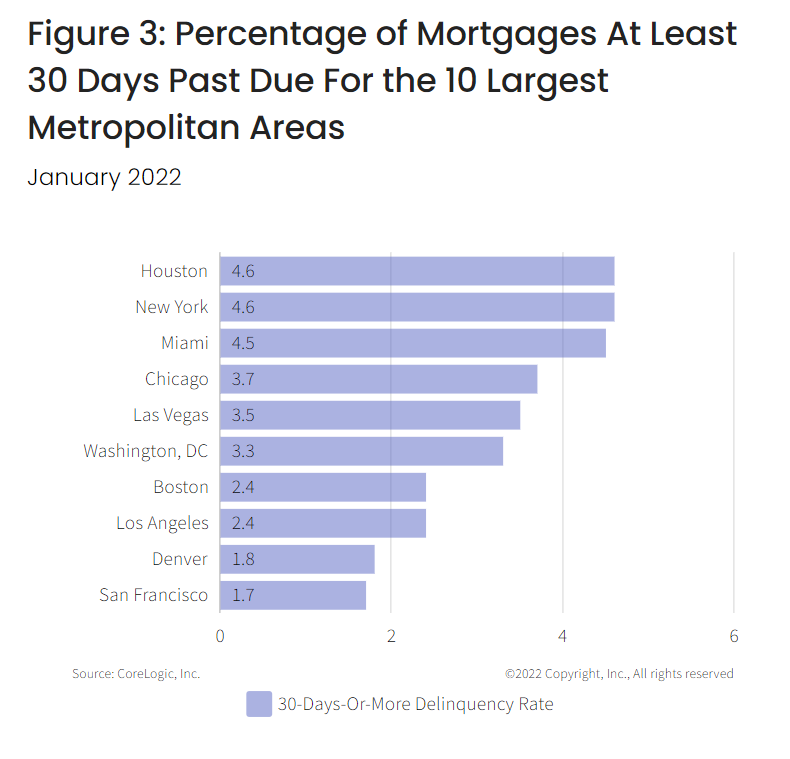

Figure 3 shows the 30-plus-day past-due rate for January 2022 for 10 large metropolitan areas. New York and Houston tied for the highest rate at 4.6%, and San Francisco had the lowest rate at 1.7%. Miami’s rate decreased 4.6 percentage points from a year earlier. Outside of the largest 10, all metros recorded a decrease in the overall delinquency rate. Nevertheless, elevated overall delinquency rates remain in some metros, including Pine Bluff, Arkansas (9.2%); Odessa, Texas (8.8%) and Vineland-Bridgeton, New Jersey (8.6%).

The nation’s overall mortgage delinquency rate reached a historic low in January, marking the 10th consecutive month of year-over-year declines. This trend can be attributed to two familiar factors: escalating home prices and a strong job market. U.S. home prices continue to reach new highs, posting 20% year-over-year growth in February. Meanwhile, the latest U.S. jobs report shows that the country added an average of 562,000 positions per month in the first quarter of 2022.

To learn more about the data behind this article and what CoreLogic has to offer, visit https://www.corelogic.com/.

Sign up to receive our stories in your inbox.

Data is changing the speed of business. Investors, Corporations, and Governments are buying new, differentiated data to gain visibility make better decisions. Don't fall behind. Let us help.

Sign up to receive our stories in your inbox.

Data is changing the speed of business. Investors, Corporations, and Governments are buying new, differentiated data to gain visibility make better decisions. Don't fall behind. Let us help.