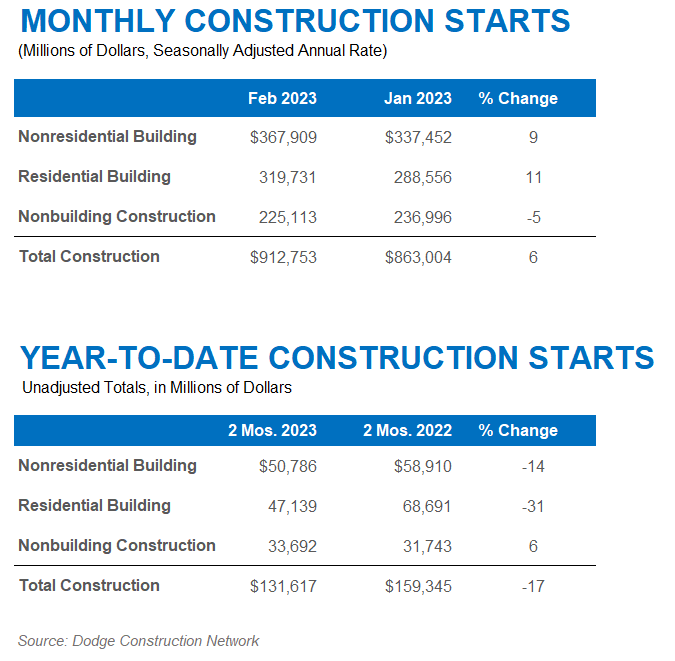

Total construction starts rose 6% in February to a seasonally adjusted annual rate of $912.8 billion, according to Dodge Construction Network. During the month, residential and nonresidential building starts rose 11% and 9% respectively, and nonbuilding starts declined by 5%.

For the first two months of 2023, total construction starts were 17% below that of 2022. On a year-over-year basis, residential starts were down 31%, nonresidential starts were off 14%, while nonbuilding starts gained 6%. For the 12 months ending February 2023, total construction starts were 9% higher than the 12 months ending February 2022. Nonresidential and nonbuilding starts were 27% and 19% higher respectively, while residential starts lost 9%.

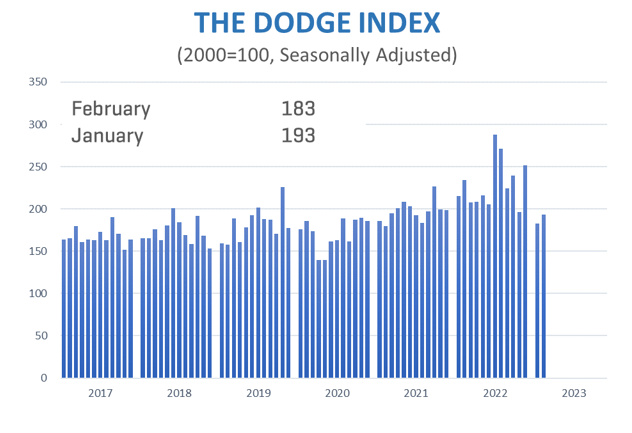

“February construction starts were a mixed bag that led to marginal growth,” said Richard Branch, chief economist for Dodge Construction Network. “Single family units posted a gain for the first time in 13 months, and manufacturing starts continued to be very robust, showing signs of promise early into 2023. However, the downturn in commercial and institutional building starts could very well be the beginning of an anticipated slow-down as the construction sector pulls back in the face of higher interest rates and lagging economic growth. While this ebbing should be comparatively mild, some construction verticals could face extreme stress as the year progresses.”

· Nonbuilding construction starts fell 5% in February to a seasonally adjusted annual rate of $225 billion. This primarily results from a 30% decline in environmental public works starts and a 5% loss in highway and bridge starts. On the plus side, utility/gas plant starts rose 68% and miscellaneous public works starts were up 6%.

For the 12 months ending February 2023, total nonbuilding starts were 19% higher than the 12 months ending February 2022. Utility/gas plant starts rose 23%, and highway bridge starts increased 17%. Environmental public works and miscellaneous nonbuilding starts were up 19% and 18% respectively on a 12-month rolling sum basis.

The largest nonbuilding projects to break ground in February were the $1.2 billion Trumbull Energy Center combined-cycle natural gas plant in Warren, Ohio,

the $540 million Merit SI Gulfstar solar farm in Wharton County, Texas, and the $530 million Mockingbird Solar Center in Brookston, Texas.

● Nonresidential building starts gained 9% in February to a seasonally adjusted annual rate of $368 billion. Driving the gain was a 218% gain in manufacturing starts due to the start of a large EV battery plant in Ohio. Commercial starts decreased 2% in February as office and parking structure starts fell, offsetting increases in retail, hotels and warehouse activity. Institutional starts also fell during the month, following a decline in education and healthcare projects.

For the 12 months ending February 2023, total nonresidential building starts were 27% higher than the 12 months ending February 2022. Manufacturing starts were 91% higher, and both institutional and commercial starts gained 18% on a 12-month rolling sum basis.

The largest nonresidential building projects to break ground in February were the $3.5 billion Honda EV battery plant in Jeffersonville, Ohio, the $1.4 billion expansion of Concourse D at Hartsfield Jackson Airport in Atlanta, Georgia, and the $500 million Apex-1 Sustainable Lithium-Ion battery plant in Hopkinsville, Kentucky.

● Residential building starts rose 11% in February to a seasonally adjusted annual rate of $320 billion. Single family and multifamily starts rose 4% and 22% respectively. For the 12 months ending in February 2023, residential starts were 9% lower than the 12 months ending in February 2022. Single family starts were 20% lower, while multifamily starts were up 18% on a rolling 12 month basis.

The largest multifamily structures to break ground in February were a $350 million mixed-use building in New York, the $215 million Four Season condominium in Washington, DC, and the $140 million Palomar Heights mixed-use building in Escondido, California.

Regionally, total construction starts in February rose in the Northeast, Midwest~~,~~ and South Central regions, but fell in the South Atlantic and West.

To learn more about the data behind this article and what Dodge Analytics has to offer, visit https://www.construction.com/.

Sign up to receive our stories in your inbox.

Data is changing the speed of business. Investors, Corporations, and Governments are buying new, differentiated data to gain visibility make better decisions. Don't fall behind. Let us help.

Sign up to receive our stories in your inbox.

Data is changing the speed of business. Investors, Corporations, and Governments are buying new, differentiated data to gain visibility make better decisions. Don't fall behind. Let us help.