In June 2020, 7.1% of home mortgages were in some stage of delinquency (30 days or more past due, including those in foreclosure)[1], slightly lower than the May 2020 rate of 7.3%, but a 3.1-percentage point increase from June 2019, according to the latest CoreLogic Loan Performance Insights Report.

The share of mortgages that were 30 to 59 days past due – considered early-stage delinquencies – was 1.8% in June 2020, down from 2.1% in June 2019. The share of mortgages 60 to 89 days past due was 1.8% in June 2020, up from 0.6% in June 2019 and down from 2.8% in May 2020.

Delinquencies progressed to the next stage in June with the serious delinquency rate – defined as 90 days or more past due, including loans in foreclosure – increasing to 2.3%, up from 1.3% in June 2019 and from 1.5% in May 2020. June’s number represented the highest rate since February 2015. The increase in the serious delinquency rate was driven by an increase in the share of mortgages 90 to 119 days past day, which increased to its highest level in more than 21 years[2]. The foreclosure inventory rate – the share of mortgages in some stage of the foreclosure process – remained low at 0.3% in June 2020, down from 0.4% from June 2019.

In addition to delinquency rates, CoreLogic tracks the rate at which mortgages transition from one stage of delinquency to the next, such as going from current to 30 days past due (Figure 1). The share of mortgages that transitioned from current to 30 days past due dropped back to 1.8% in June 2020 – a decrease from 3% in May 2020.

![]()

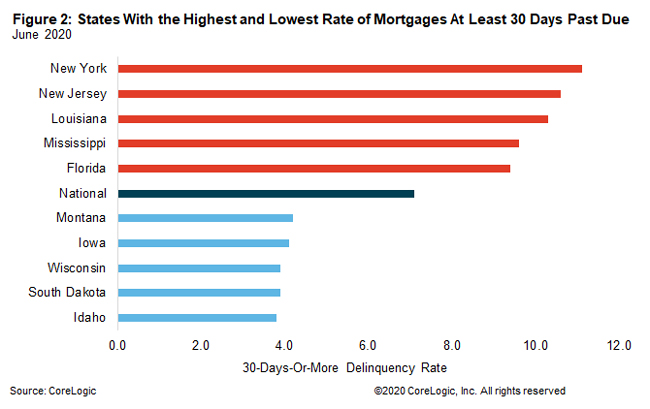

Figure 2 shows the states with the highest and lowest share of mortgages 30 days or more delinquent. In June 2020, that rate was highest in New York at 11.1% and lowest in Idaho at 3.8%. All U.S. states posted annual gains in their overall delinquency rate in June 2020. The states that logged the largest annual increases were Nevada (+5.7 percentage points), New Jersey (+5.5 percentage points), New York (+5.2 percentage points) and Hawaii (+5.1 percentage points).

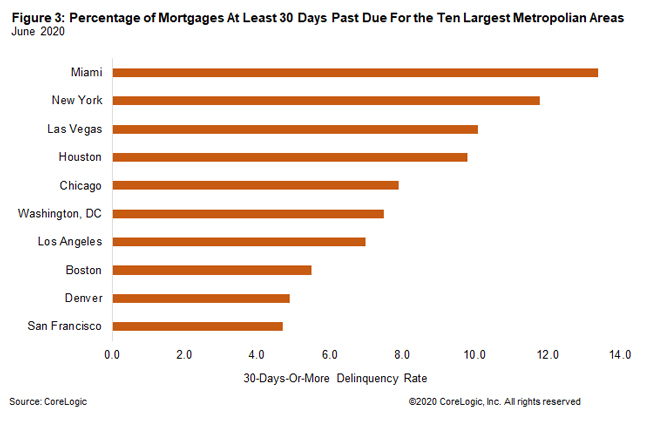

Figure 3 shows the 30-plus-day past-due rate for June 2020 for 10 large metropolitan areas.[3] Miami had the highest rate at 13.4% and San Francisco had the lowest rate at 4.7%. Miami’s rate increased 8.1 percentage points from a year earlier. Outside of the largest 10, all but two metros recorded an increase in the overall delinquency rate, with tourist destinations such as Kahului, Hawaii and Las Vegas, Nevada, as well as oil-dependent Odessa, Texas and Midland, Texas, showing the largest gains.

© 2020 CoreLogic, Inc. All rights reserved.

[1] Data in this report is provided by TrueStandings Servicing. https://www.corelogic.com/products/truestandings-servicing.aspx. The CARES Act provided forbearance for borrowers with federally backed mortgage loans who were economically impacted by the pandemic. Borrowers in a forbearance program who have missed a mortgage payment are included in the CoreLogic delinquency statistics, even if the loan servicer has not reported the loan as delinquent to credit repositories.

[2] The data in this report date back to January 1999.

[3] Metropolitan areas used in this report are the ten most populous Metropolitan Statistical Areas. The report uses Metropolitan Divisions where available.

To learn more about the data behind this article and what CoreLogic has to offer, visit https://www.corelogic.com/.

Sign up to receive our stories in your inbox.

Data is changing the speed of business. Investors, Corporations, and Governments are buying new, differentiated data to gain visibility make better decisions. Don't fall behind. Let us help.

Sign up to receive our stories in your inbox.

Data is changing the speed of business. Investors, Corporations, and Governments are buying new, differentiated data to gain visibility make better decisions. Don't fall behind. Let us help.