Accumulating Missed Payments Pose Challenges to Affordable Post-Forbearance Resolutions

As the pandemic wears on, the nation’s unemployment rate remains at elevated levels. With unemployment rate at 6.7% at the end of 2020, millions of people have likely been out of work for as long as nine months since April. And without a regular income, many homeowners who sought payment forbearance assistance under the CARES Act are likely to find themselves in an extended stay in forbearance.

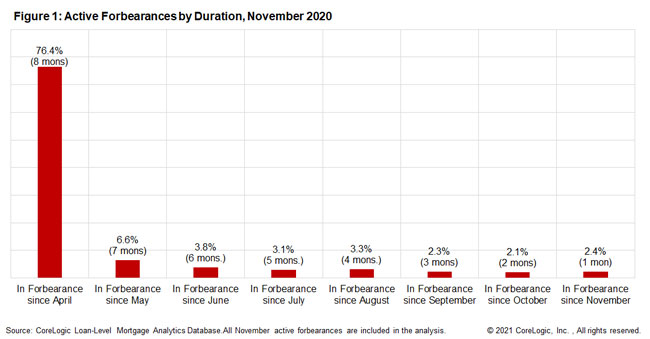

The latest loan performance data shows that as of November, the majority of active forborne loans have been in forbearance since April (Figure 1) – 76.4% since April and another 6.6% since May, for a combined total of 83% in those two months. That means as of November 2020, more than 4-in-5 active forbearances were already in their second 6-month forbearance phase.

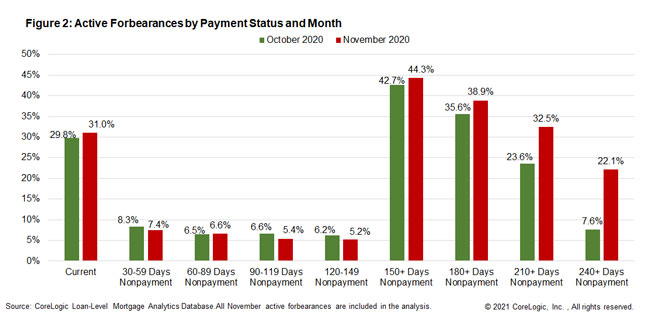

While some homeowners have managed to keep up mortgage payments while in forbearance, many others have fallen further behind the payments (Figure 2).

By the end of November, 38.9% of the loans under active forbearance have missed at least six payments, and nearly 1-in-3 (32.5%) missed at least seven payments. While the 150+ day, 180+ day and 210+ day nonpayment rates all trend higher between October and November, the largest increases are among the loans in 240 or more days past due, up from 7.6% in October to 22.1% in November. (The October number is reflective of loans already in nonpayment prior to enactment of the CARES Act.)

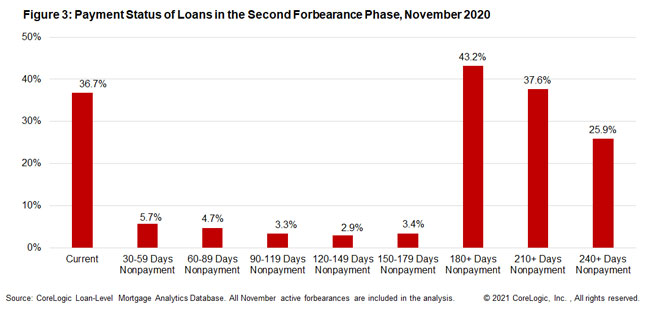

Figure 3 shows various nonpayment rates among loans that have entered the second phase of forbearance. These are the loans that sought forbearance in April or May.

Its relatively bifurcated pattern indicates that the majority of the loans are either current (36.7%) or have missed at least 6 payments (43.2%); more than 1-in-3 (37.6%) have been in nonpayment since May and 1-in-4 (25.9%) in nonpayment since April. It is no surprise the longer the loans stay in forbearance, the more missed payments have accumulated – as homeowners who have experienced more permanent job losses or pay and hour cuts are more likely to apply for a continued stay in forbearance. With the number of missed payments accumulating, greater challenges lay ahead for the struggling homeowners to find an affordable post-forbearance resolution.

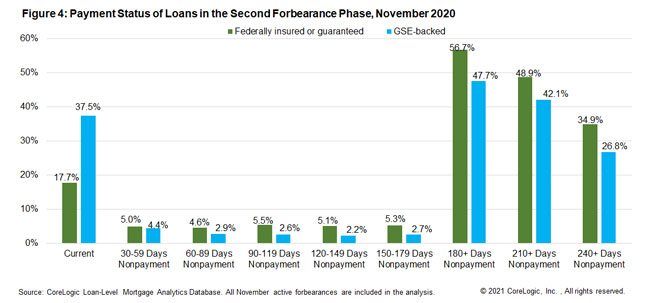

Figures 4 shows various nonpayment rates separately for federally insured or guaranteed loans (FHA, VA and RHS) and for GSE-backed loans that have entered the second six-month stay in forbearance.

For homeowners with a federally insured loan such as an FHA or VA loan, the challenges ahead are even greater. As of November, only 17.7% of the loans under a continued stay in forbearance are current in payment. As many as 56.7% are behind at least six payments, and close to 1-in-2 (48.9%) have been in nonpayment since May and 1-in-3 (34.9%) in nonpayment since April.

Nonpayment rates are also elevated for GSE-backed loans: Nearly 1-in-2 (47.7%) have missed at least six payments, 42.1% at least seven payments, and more than 1-in-4 loans (26.8%) have been in nonpayment since April. Lower nonpayment rates among GSE-backed loans are reflective of conventional loans’ typically much lower delinquency rates than federally insured loans.

During the first quarter of 2021 a majority of active forbearances are already nearing the end of the 12-month forbearance term. With post-holiday spike in coronavirus weighing on the job market recovery, the overhang in severe nonpayment will continue to build up in the months to come, posing challenges to find affordable post-forbearance resolutions──particularly to homeowners who could no longer afford to resume their pre-pandemic monthly payment by either reinstating the mortgages or setting up repayment or deferral plans. To these homeowners, a loan modification that extends the term of maturity or lowers the interest rate, or both, may offer the potential to lower and make the monthly payment more affordable.

To learn more about the data behind this article and what CoreLogic has to offer, visit https://www.corelogic.com/.

Sign up to receive our stories in your inbox.

Data is changing the speed of business. Investors, Corporations, and Governments are buying new, differentiated data to gain visibility make better decisions. Don't fall behind. Let us help.

Sign up to receive our stories in your inbox.

Data is changing the speed of business. Investors, Corporations, and Governments are buying new, differentiated data to gain visibility make better decisions. Don't fall behind. Let us help.