U.S. Single-Family Rents Up 7.5% Year Over Year in June

Overall Single-Family Rent Growth

U.S. single-family rent growth increased 7.5% in June 2021, the fastest year-over-year increase since at least January 2005[1], according to the CoreLogic Single-Family Rent Index (SFRI). The index measures rent changes among single-family rental homes, including condominiums, using a repeat-rent analysis to measure the same rental properties over time. The June 2021 increase was more than five times the June 2020 increase, and while the index slowed to a post-pandemic low last June, rent growth is running well above pre-pandemic levels when compared with 2019.

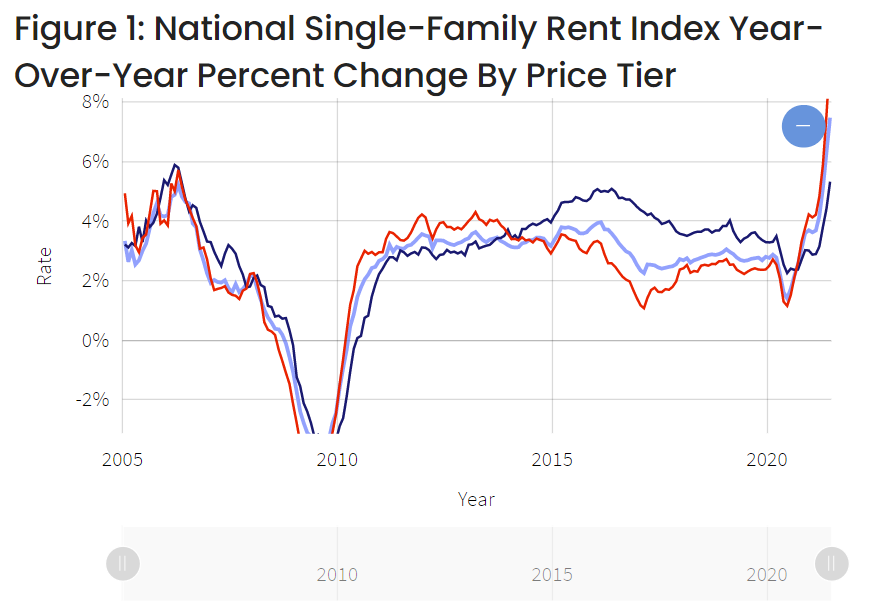

Single-Family Rent Growth by Price Tier

An uneven U.S. job recovery, sometimes called a “K-shaped” recovery, is reflected in the rent price growth of the low- and high-price rent tiers, with the increase in lower-priced rentals lagging behind that of higher-priced rentals. The low-price tier is defined as properties with rent prices less than 75% of the region’s median rent, and the high-price tier is defined as properties with rent prices greater than 125% of a region’s median rent (Figure 1).

Rent prices for the low-price tier, increased 5.3% year over year in June 2021, up from 2.3% in June 2020. Meanwhile, high-price rentals increased 9.6% in June 2021, up from a gain of 1.2% in June 2020. This was the fastest increase in low-price rents since May 2006, and the fastest increase in high-price rents in the history of the SFRI.

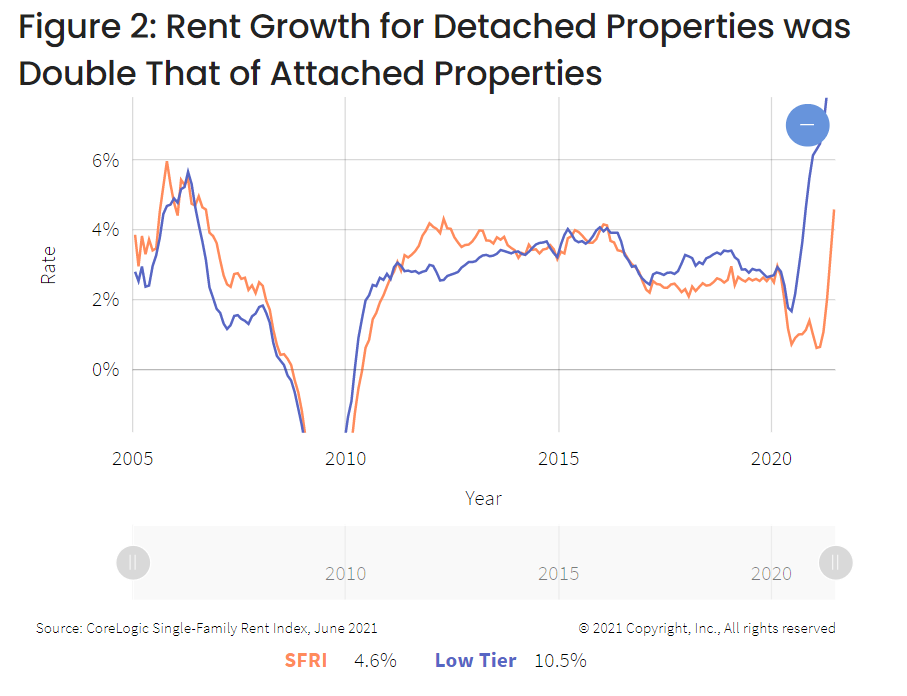

Single-Family Rent Growth by Property Type

Differences in rent growth by property type emerged after the pandemic as renters sought out standalone properties in lower density areas (Figure 2). The detached property type tier is defined as properties with a free-standing residential building, and the attached property type tier is defined as a single-family dwelling that is attached to other single-family dwellings, which includes duplexes, triplexes, quadplexes, townhouses, row-houses, condos and co-ops.

Detached homes are overwhelmingly preferred by would-be homebuyers who have been either priced out of the market or unable to find a home in today’s supply-constrained market, which has pushed rent up for these homes. Annual rent growth for detached rentals was 10.5% in June, compared with just 4.6% for attached rentals.

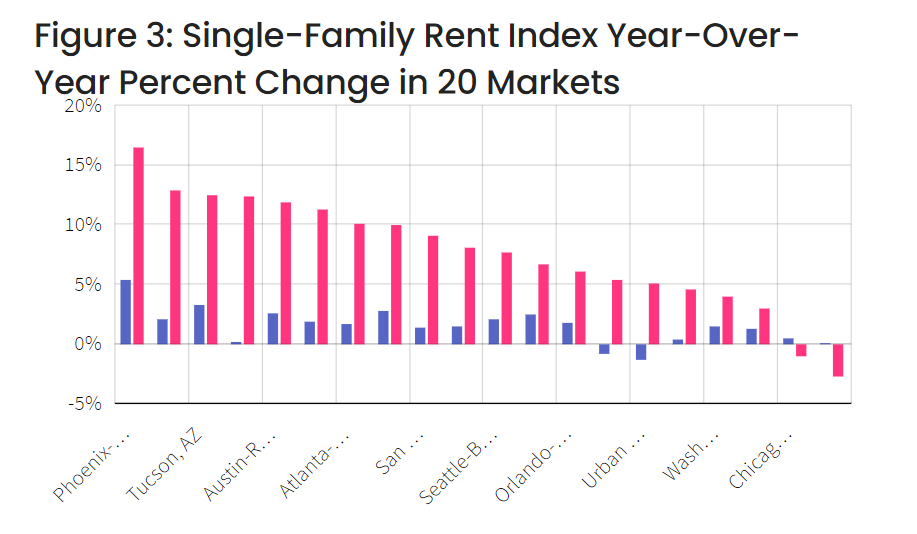

Metro-Level Results

Figure 3 shows the year-over-year change in the rental index for 20 large metropolitan areas in June 2021. Among the 20 metro areas shown, Phoenix stood out with the highest year-over-year rent growth in June as it has for most of the last three years, with an increase of 16.5%, followed by Las Vegas, Nevada (+12.9%) and Tucson, Arizona (+12.5%). Two metro areas experienced annual declines in rent prices: Boston (-2.7%) and Chicago (-1%).

Boston and Chicago were also the only two of the 20 metros shown in Figure 3 to have lower rent growth than a year ago, with Boston showing a deceleration of 2.8 percentage points and Chicago showing a deceleration of 1.5 percentage points from June 2020.

The slowdown in Boston rent growth might be attributed to college students choosing to forgo large monthly rental payments. Median rent in Boston was $2,800, 1.7 times national median monthly rent. For Chicago, there were large differences in rents of attached versus detached properties. While rent prices of detached rentals in Chicago increased by 6.8%, attached rentals experienced a decrease of 2.2%.

Single-family rents rose by more than five times the rate from a year earlier in June 2021. Strong job and income growth, as well as fierce competition for for-sale housing, is fueling demand for single-family rentals. As space and affordability remain top priorities for renters, we can expect to see a similar trend as in the for-sale market — increased migration to less dense and lower cost areas.

To learn more about the data behind this article and what CoreLogic has to offer, visit https://www.corelogic.com/.

Sign up to receive our stories in your inbox.

Data is changing the speed of business. Investors, Corporations, and Governments are buying new, differentiated data to gain visibility make better decisions. Don't fall behind. Let us help.

Sign up to receive our stories in your inbox.

Data is changing the speed of business. Investors, Corporations, and Governments are buying new, differentiated data to gain visibility make better decisions. Don't fall behind. Let us help.