In late 2020, we discussed our belief that top tier malls would see a very strong recovery in 2021. The pace of the retail rebound was already seeing picking up, and several changes that mall owners had begun instituting years prior were well aligned with how the wider retail space was evolving. From new perspectives on tenant mix to a sharper focus on providing a wider and more holistic shopping experience, there were many reasons for optimism.

And looking back at the performance of top malls in 2021 appears to justify that confidence.

What We Saw in 2021 – A Full Year Perspective

In 2021, visits to the Placer.ai Mall Index, which looks at 100 top tier indoor malls and 100 outdoor malls throughout the country, were up 51.5% year over year, and down just 10.2% compared to 2019.

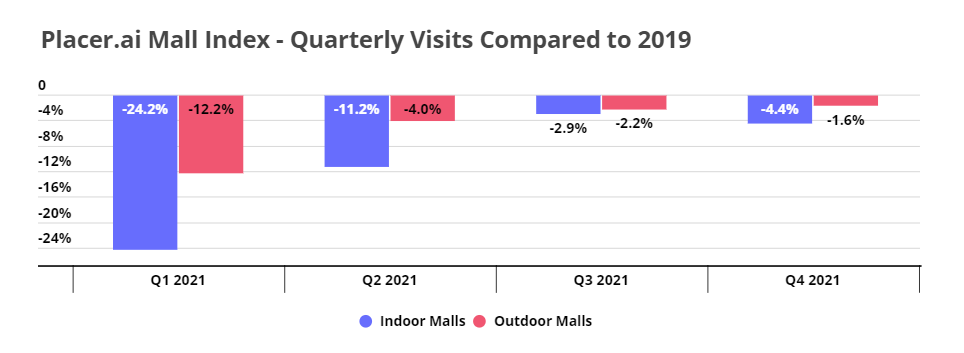

While these numbers are impressive in their own right, the distribution of visits only deepens the feeling that 2021 was an especially – if not surprisingly – strong year for malls. In Q1, visits to indoor malls were down 24.2% compared to the same quarter in 2019, yet by Q2 this number had dropped to 11.2% and by Q3 and Q4 it was down to 2.9% and 4.4%, respectively. This indicates that visitors who had kept away from malls did so because of the wider situation and not due to any shift in consumer sentiment or demand.

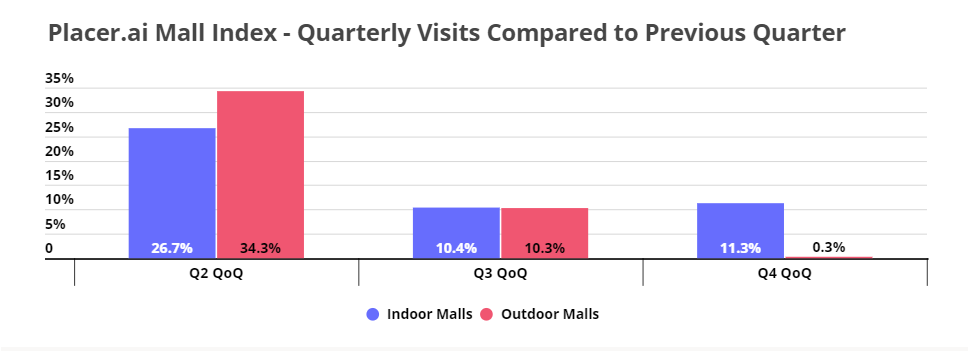

And even the increased gap between Q3 and Q4 requires more context. While the visit gap did increase in the holiday season, much of that was driven by rising COVID cases in November and December and comparisons to an especially strong holiday season in 2019. When looking at visits compared to the prior quarter, every period in 2021 showed growth on the preceding quarter. Even Q4 saw an 11.3% visit increase compared to a summer period that was both especially strong and included the initial surge of pent up demand that followed retail’s wider reopening.

Relative Strength in the Holidays

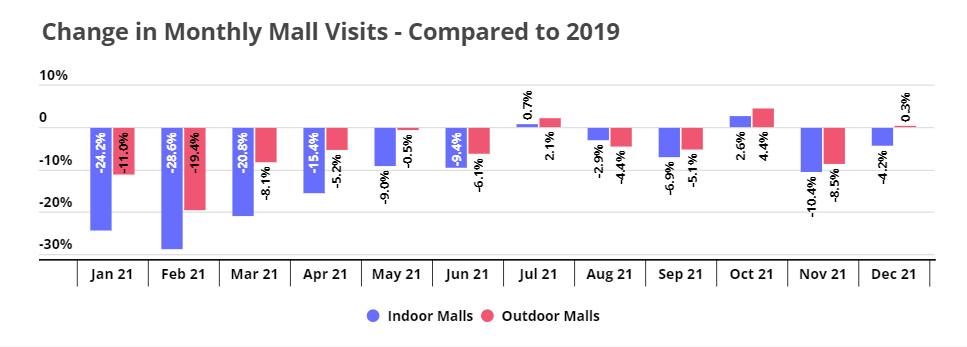

The nature of the recovery – and the potential for even greater heights for indoor malls in 2022 – comes into focus when looking at the monthly visits comparisons. While visits were up significantly year over year every month in 2021, the heights of the recovery compared to 2019 really began in the summer. After seeing monthly visits down around 9% compared to 2019 in May and June, the summer Back-to-School season drove a surge of traffic that saw visit growth of 0.7% for indoor malls in July compared to July 2019. Visits then returned to a decline in August largely because of the latter part of the month when COVID cases rose and visits dropped as a result.

September saw a continuation of the downward trend, but October saw the strongest visit numbers compared to 2019 for the entire year. Visits that month were up 2.6% for indoor malls and 4.4% for outdoor malls when compared to 2019. Declining COVID cases contributed, but a likely force behind the shift was a push by retailers to extend the holiday season earlier than before to account for supply chain challenges, labor shortages and COVID risks.

And this push by retailers to extend the season alongside rising COVID cases in late November likely played a key role in influencing major shopping days like Black Friday and Super Saturday. The result was November visits dropping 10.4% compared to 2019 for indoor malls and 8.5% for outdoor malls. Yet, here too, the rebound was fast and significant. Visits in December were down just 4.2% compared to 2019 for indoor malls and up 0.3% for outdoor malls. While the latter sees less of a spike in traffic in the winter, for indoor malls the limited decline was a significant achievement considering the significant obstacles.

Room for Continued Optimism?

So what does this mean for indoor malls heading into 2022?

The pace and consistency of the recovery indicate that the shifts that major malls made are in line with what customers are looking for. A narrower focus on apparel offers an opportunity to identify tenants that drive visits throughout the week, and creates less direct competition between mall tenants – not to mention the ability to attract exciting new retail concepts like digitally native brands. A heightened focus on dining and entertainment creates a better environment for an extended visit where shoppers take advantage of the full ‘day out’ potential of a mall. And the push for more fitness and co-working spaces fits within a wider push for live, work, play environments that take advantage of nearby office and residential areas.

The data also suggests that there is still room for more in the recovery. The declines on Black Friday and Super Saturday – while likely an indication of a continued trend that diminishes the full magnitude of these days – were likely far more dramatic than they would have been had it not been for the unique confluence of the COVID, supply chain, and labor concern trifecta. Add to that the potential for a heavy return period in January because of an online-centric holiday season, and there are promising signs for the continued progress of the retail recovery and an even stronger 2022.

The conclusion from the data – expect bigger and better things for malls in 2022.

To learn more about the data behind this article and what Placer has to offer, visit https://www.placer.ai/.

Sign up to receive our stories in your inbox.

Data is changing the speed of business. Investors, Corporations, and Governments are buying new, differentiated data to gain visibility make better decisions. Don't fall behind. Let us help.

Sign up to receive our stories in your inbox.

Data is changing the speed of business. Investors, Corporations, and Governments are buying new, differentiated data to gain visibility make better decisions. Don't fall behind. Let us help.