Look for a larger share of cash-out, longer terms, and lower credit scores

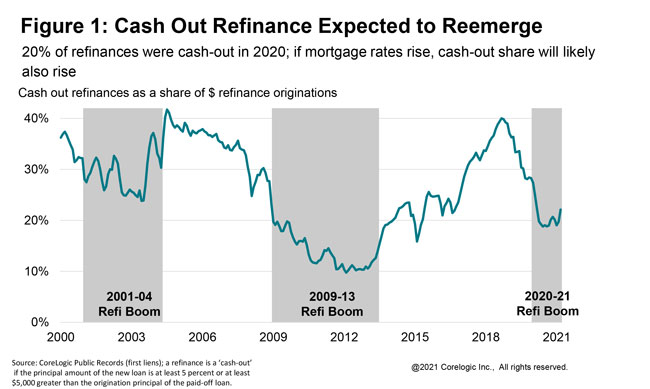

With mortgage rates declining to ever new lows during 2020, the mortgage market had the largest number of originations in 17 years. The volume was driven by no-cash-out refinance: more than one-half of the originations, and 4-in-5 refinance loans, were no-cash-out during 2020.

Interest rates on fixed-rate mortgages were at an all-time low at the beginning of 2021 and have moved higher since then. While forecasts vary, the consensus view among economists is that mortgage rates will rise between one-fourth to three-fourths of a percentage point during the next 12 months. More expensive credit will likely reduce refinance volumes and alter the characteristics of borrowers who do refinance: Look for a larger share of refinance that have cash-out, longer term, and lower credit scores.

When mortgage rates reach new lows, no-cash-out refinance dominates the market as homeowners seek lower payments or shorter terms. When mortgage rates rise and are well above a recent low, the mix of refinance shifts toward more cash-out. Only 20% of refinance loans included cash-out last year. If mortgage rates rise in the coming year, expect the cash-out share to rise as well.

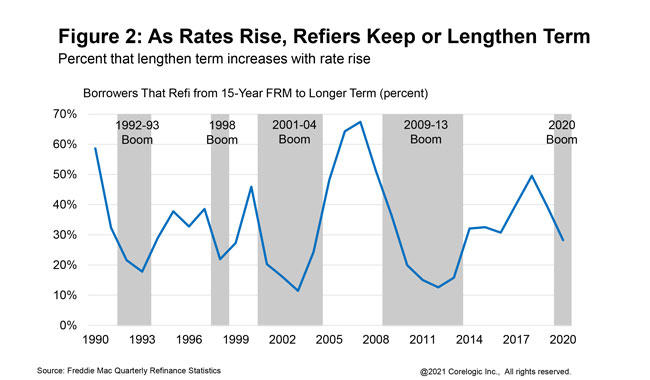

Borrowers who refinance when interest rates have begun to rise also prefer to keep monthly payments low. That is a reason why the average term of refinance mortgages generally increases with higher rates. As an example, a borrower who has a 15-year loan and wants to have a cash-out refinance may opt for a 30-year term in order to keep the monthly mortgage payment as low as possible.

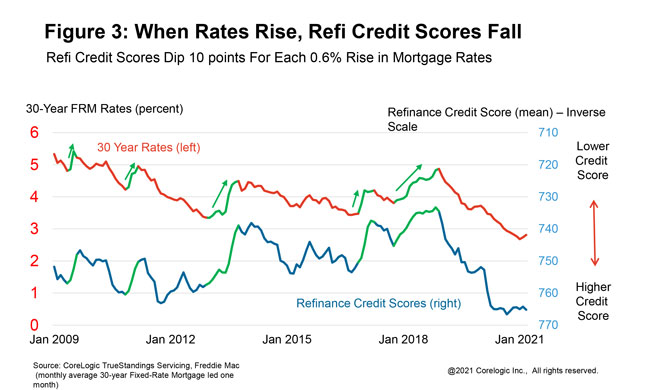

Borrowers with lower credit risk often dominate the applicant pool during a refinance boom. As interest rates rise, applicants with more complex underwriting requirements become more common.

Since 2009 there have been five up-rate cycles with at least a one-half percentage point rise in mortgage rates. In each instance the average credit score of refinance borrowers declined, with an average 10-point dip in credit score for each 0.6-percentage point increase in interest rates.

As mortgage rates gradually move higher in the coming year, expect these same trends to re-emerge among borrowers who apply for a refinance loan: more will want cash-out and a longer term, and more will have blemishes in their credit history.

Summary:

To learn more about the data behind this article and what CoreLogic has to offer, visit https://www.corelogic.com/.

Sign up to receive our stories in your inbox.

Data is changing the speed of business. Investors, Corporations, and Governments are buying new, differentiated data to gain visibility make better decisions. Don't fall behind. Let us help.

Sign up to receive our stories in your inbox.

Data is changing the speed of business. Investors, Corporations, and Governments are buying new, differentiated data to gain visibility make better decisions. Don't fall behind. Let us help.