The world of offline retail has been dominated by two key names – Walmart and Target. The strength of these retailers has centered around a unique ability to build a powerful and sustainable brand relationship.

And while the entire retail ecosystem took a hit during the pandemic, these giants included, the recovery has presented an opportunity to really compare the environments they operate in.

Recovering Trends

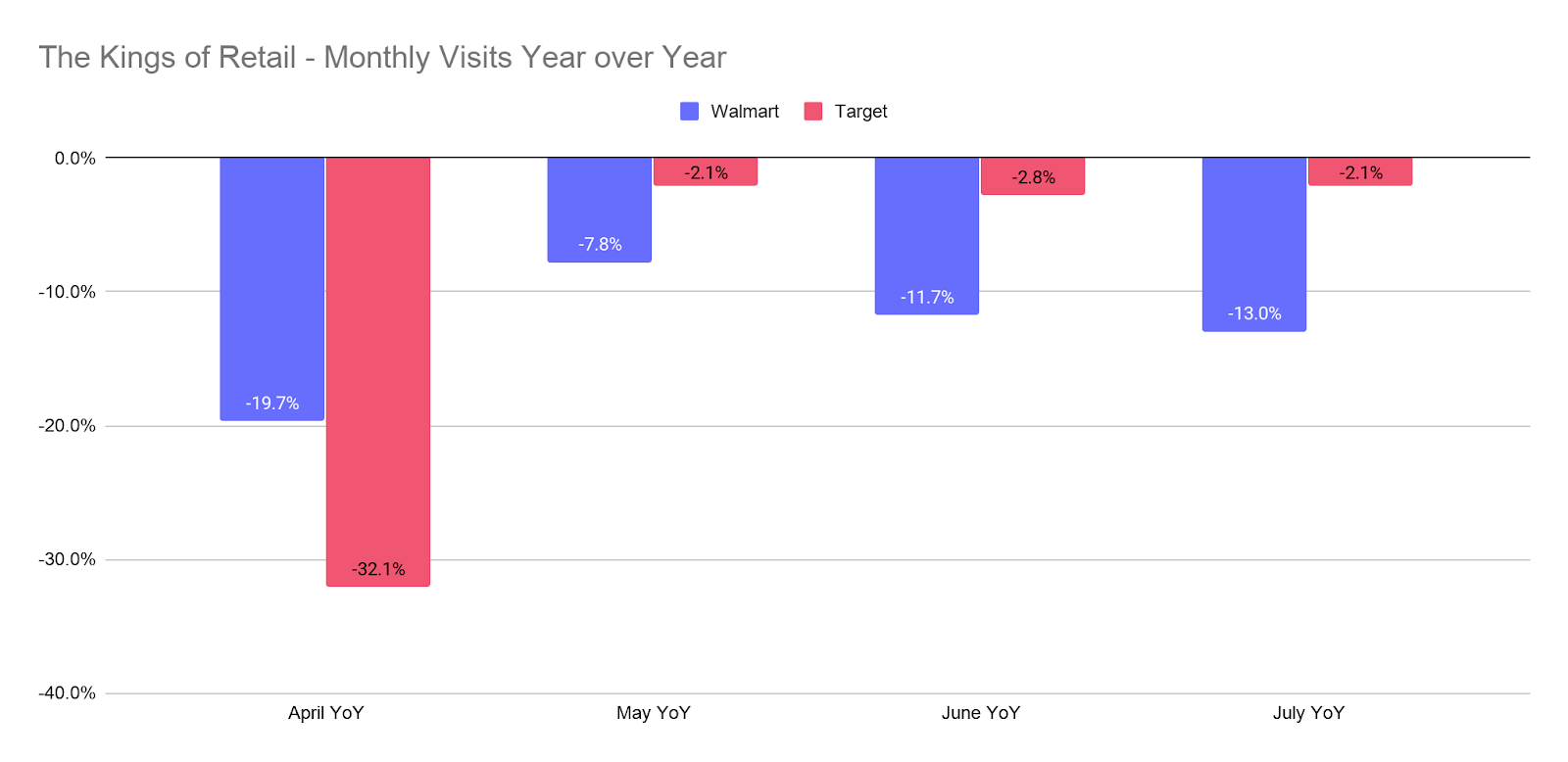

The first look at monthly visits for Walmart and Target showed brands that are recovering from their low points in April. Target quickly returned to about 2% down year over year and held steady at that rate for May, June, and July. Walmart saw visits rise to numbers just 7.8% lower than 2019 in May, before seeing visits drop to 11.7% down year over year in June and 13.0% down in July.

Essentially, both brands have seen visits rates stagnate lower than the norm, but to understand the cause of this trend requires a deeper analysis.

Regional Perspectives

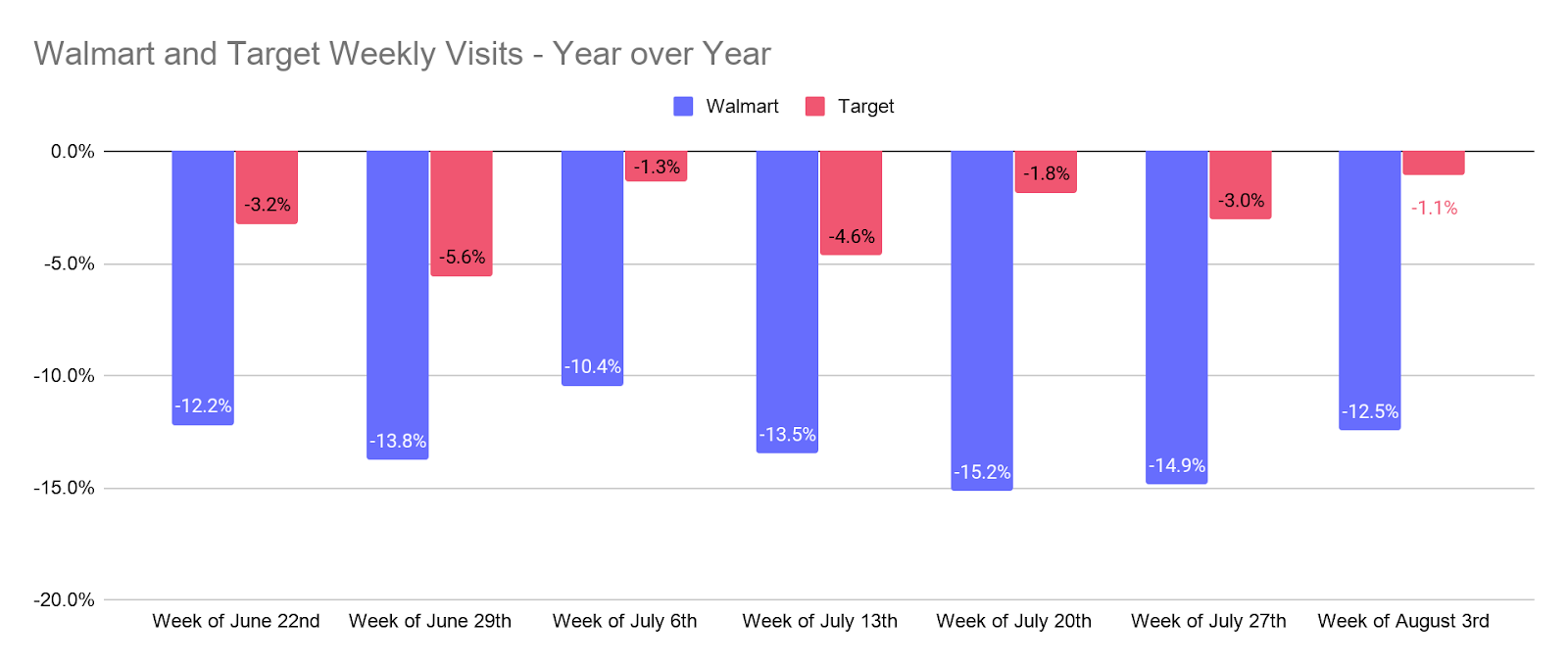

Looking at weekly visits year over year seems to present a similar picture. Target and Walmart both look to be sustaining relatively similar numbers since mid-June. Yet, nationwide visits can obscure the local picture. When analyzing data from California, New York, Texas, and Florida, four of the biggest states in terms of location density for both brands, a clear pattern emerges. Resurgences of cases in key states have heavily limited the ability of these brands to enjoy a full bounceback.

Looking at the week beginning July 27th, Walmart visits were down 14.9% year over year and Target visits were down 3.0%. Yet, the average decline for the four states mentioned was 23.0% for Walmart and 12.6% for Target, meaning the overall performance for both chains was being heavily limited by rising numbers of COVID cases in key states. And the signs of improvement are there as cases come under greater control with both brands showing strong steps forward the week beginning August 3rd. Target was within 1.1% of 2019 numbers with a week over week improvement of over 5%, and Walmart was within 12.5% with a week over week improvement of 2.9%.

Target’s Secret Weapon

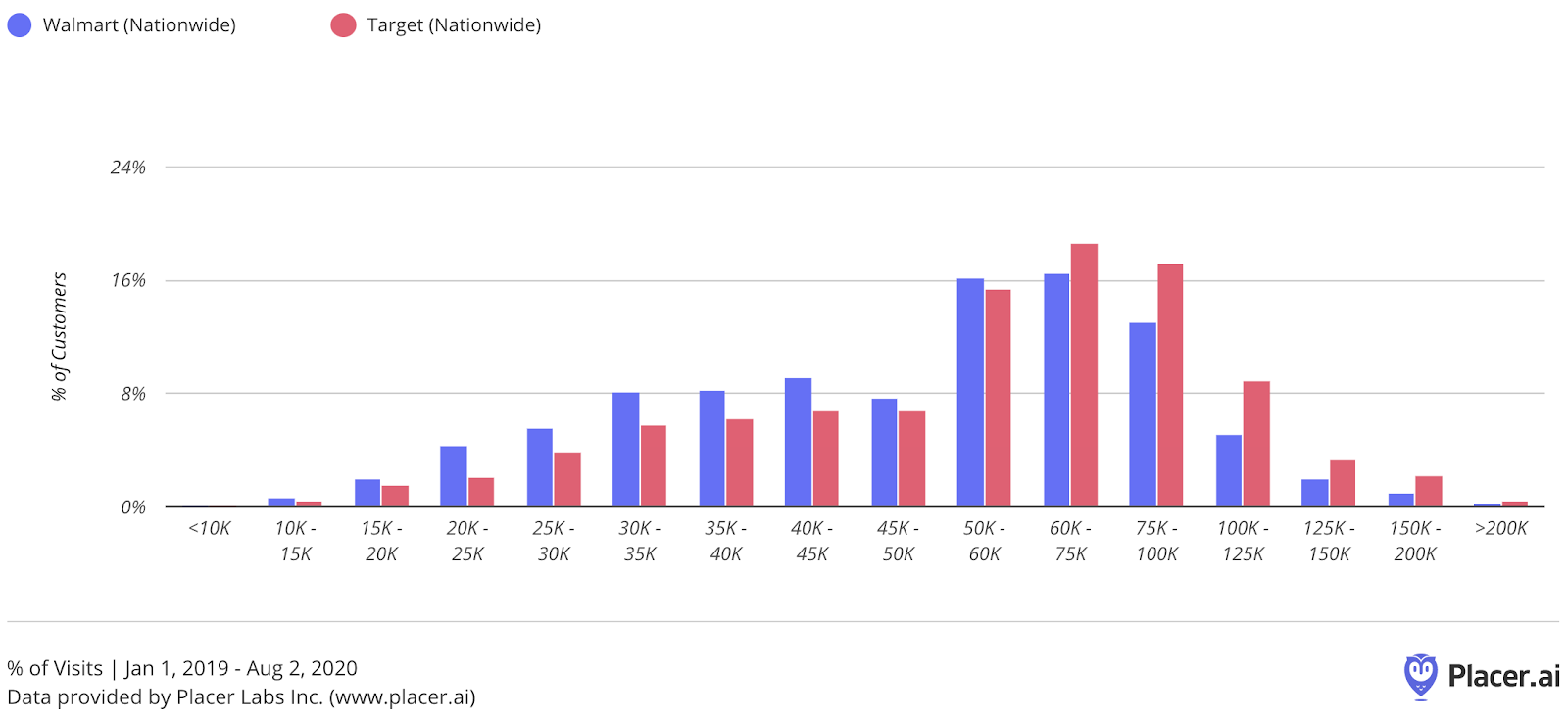

Even with this information, there is still a clear difference between the two. While Target’s drop was steeper mid-pandemic, its rise to normalcy has been faster. While the ‘middle class’ of retail has often been identified as a ‘goner,’ there are strong indications that Target has managed to master reaching this audience to great effect.

While 29.5% of Target shoppers earn between $75,000 and $150,000, only 20.3% of Walmart shoppers sit within that range. Being effective at hitting this audience comes with big advantages – it makes partnerships with premium brands like Disney work, it enables smaller format stores in higher-priced locations and allows the brand to use its unique approach to merchandising to full effect. And the approach is one of the many reasons we identified Target as one of the winners of 2020 back in January. In a sense, while Target and Walmart are often seen as direct competitors, part of Target’s unique potential rests in the lack of competition here and a more “open” landscape.

Who’s Competing with Walmart?

So, who is competing with Walmart? It is essential to note that Walmart’s reach is so massive that calling anyone a competitor requires the caveat that competition is near impossible. Yet, the brand may be facing at least a nudge on the cheaper side of the market and in an increasingly important category.

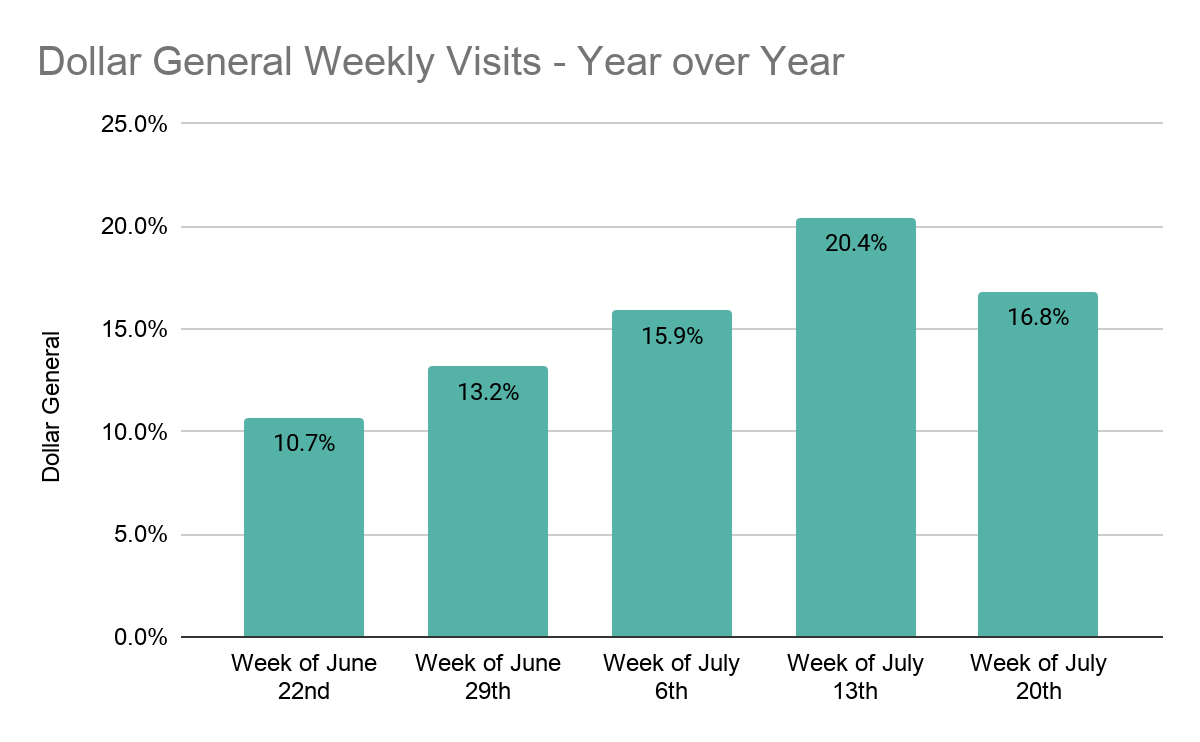

Looking at cross-shopping patterns between May and July 2020 and comparing them to the same period in 2019, Dollar General cross-shopping has grown substantially. In 2019, 19.4% of Walmart shoppers visited a Dollar General during that period, but in 2020 that number had grown to 24.2%, a huge shift considering the massive number of Walmart visitors. And Dollar General is rising on its own with weekly visits showing significant year-over-year growth.

The other shift is coming from the home improvement sector where a rise in people heading to giants like Home Depot and Lowe’s seem to be taking at least some visitors from Walmart. Home Depot cross-shopping went from 30.5% in 2019 to 34.1% in 2020, while Lowe’s cross-shopping jumped from 25.3% in 2019 to 37.8% in 2020.

Interestingly, this trend seems to indicate that the focus on home goods and improvement shopping takes away a need to visit a Walmart location that would normally be a go-to for those visitors. It also indicates that one of Walmart’s greatest threats, again, with threat clearly understood in the Walmart context, could be the growth of top dollar brands.

Conclusion

Walmart and Target are the top offline retailers for a reason, and this reality is not going to change anytime soon. Yet, the paths of their respective recoveries do reveal some interesting elements about their offline presence, competitive landscape, and channels for growth. While Walmart is still king, the pandemic has given rise to more home improvement shopping and growing dollar store visits, two segments that seem to be taking away visits. On the other hand, Target’s clear difference in audience focus could provide the strongest path forward for the brand.

Finally, both are being heavily hit by the resurgence of cases and slow recoveries in a handful of key states. The effects here, especially compared with the huge surges both brands experienced in the back to school season of 2019, are likely playing a significant role in the lingering limitations on growth.

To learn more about the data behind this article and what Placer has to offer, visit https://www.placer.ai/.

Sign up to receive our stories in your inbox.

Data is changing the speed of business. Investors, Corporations, and Governments are buying new, differentiated data to gain visibility make better decisions. Don't fall behind. Let us help.

Sign up to receive our stories in your inbox.

Data is changing the speed of business. Investors, Corporations, and Governments are buying new, differentiated data to gain visibility make better decisions. Don't fall behind. Let us help.