Allbirds, the San Francisco-based startup known for its sustainable footwear collections, recently filed for an IPO. Initially launched as a DTC sneaker company, Allbirds has been growing its retail footprint over the last few years while also expanding into apparel categories. As Allbirds prepares for its public debut, consumer spending data reveals how returning customers and holiday sales have contributed to sales growth, as well as how the company’s retail locations in select metro areas have fared during the pandemic.

The summer brought positive signs for retail brands across the country with the big box giants, malls and even department stores seeing a needed boost. But with August in the rearview mirror, how much did the summer really contribute to the retail recovery? July and August brought a clear shift in consumer foot traffic, pushing many retail leaders back to positions of growth. Walmart saw visits up 2.9% and 3.9% in July and August when compared to the same months in 2019 – an especially impressive achievement considering the heights hit during that season.

The cigarette industry has faced a declining customer base for years—and COVID didn’t help. As more people quit smoking, cigarette producers are shifting their strategies. Philip Morris, owner of six of the world’s 15 top cigarette brands including Marlboro, is now changing course and pursuing a “smoke-free future.” In doing so, it is investing heavily in healthcare alternatives and respirable pharmaceuticals. The most recent CDC data found that 14% of Americans were regular smokers in 2019.

Ola, let’s talk about the food delivery market in Brazil. With Brazil covering almost half of the Latin America food delivery market, it is definitely the most important battlefield for on-demand food delivery companies. According to Measurable AI’s e-receipts data panel in Brazil: iFood, Rappi and UberEats are currently the three major players in the Brazil food delivery market. As of Q2 2021, iFood leads the market with over 80% market share, and UberEats comes next with around 10%. UberEats had a higher market share from March to July in 2020 at over 25%, but the momentum stopped soon after.

In this Placer Bytes, we dive into the recoveries of GameStop, Dave & Buster’s and AMC to gather insights on experiential retail and retail’s recovery overall. The wave of excitement surrounding GameStop’s stock had little to do with the retailer’s offline performance, but it does appear that the buzz is working in the brand’s favor. Comparing weekly visits to 2019 since the start of the year reveals a steady and consistent reduction in the visit gap. And while the initial rush of retail reopenings in March drove a short spurt of comparative growth

Since seeing demand decrease in the last year following the pandemic, the rideshare industry has been making a gradual recovery around the globe. In April of this year, Uber announced their plan to recruit 20,000 more drivers in the United Kingdom as demand began ramping up again. To see exactly how much UK rideshare services have recovered since the start of the pandemic, Edison Trends analyzed over 120,000 transactions.

With singles "vaxxed and waxed," will 2021 turn out to be the summer of love? Unfortunately, Pathmatics Explorer can't help us predict the future. But it can tell us how the top dating sites and apps are advertising. Pathmatics data shows us that dating apps overwhelmingly favor Facebook, Instagram, and Hulu, with over 90% of digital advertising budgets devoted to these three platforms. So who are the top advertisers in the dating industry, and how are they using digital to woo new customers?

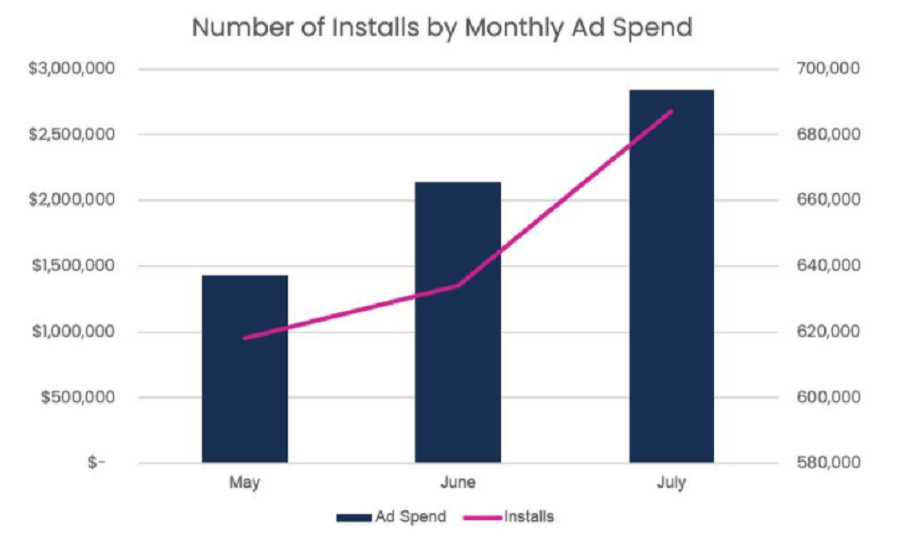

Affirm recently announced a partnership with Amazon to offer its Buy Now, Pay Later services on the site. While partnering with the world’s largest retailer outside China seems an easy choice to make, many other companies that offer services to retailers struggle with finding the kind of rapidly growing brands who need partners in their ecosystems to continue a strong trajectory. Be they payment, marketing, or logistics companies, these brands can find such partners on the CE Vision platform.

It’s difficult to properly contextualize the overwhelming power of the Pumpkin Spice Latte and the excitement it generates. In 2019, and then again last summer in a season heavily affected by COVID, the drink consistently managed to drive significant visits to Starbucks locations nationwide. And the push is incredibly strategic as it helps to herald in the coffee giant’s fall and winter strength after months of spring and summer. But could the launch deliver yet again?

Over the last two decades, we’ve seen several new business categories be born. Without companies like Netflix, Uber, Apple and many more changing the status quo, this past year would have been completely different. They’ve changed everything from how we watch videos and listen to music to how we order takeout. Consumer category creators are well known because they affect our everyday life. But behind the scenes, software category creators have been changing the way businesses run.

The college admissions scandal of 2019 highlighted the ways that elite private school students are using their resources to secure admission to top tier colleges. This week we focus on whether going to private high schools really improves your chances of getting into a top tier college. And if so, what colleges enroll the most private school students? Prior to 2005 only 40% of the students at top 20 universities were from public schools, but since then there has been a steady increase to 60%.

In the midst of rising concerns among retailers over a COVID resurgence and a critical Back-to-School season, we dove into Gap Inc. and Lululemon’s foot traffic to find out how these apparel leaders are faring amidst the uncertainty. Gap Inc. had a mixed experience over the pandemic, with some of its iconic brands taking a hit while others flourished. In October 2020, the company unveiled the “Power Plan 2023” – a strategy involving reducing the Gap and Banana Republic store count in North America to 870 by the end of fiscal 2023

The events of the past year and a half have highlighted existing regional disparities – and created some new ones – as a result of the differences in virus spread, regulatory decisions, and calendars reopening. But because of how retail data is usually presented, the variance in the pace of economic recovery between different locales can sometimes be hard to spot. Indeed, most stakeholders in the future of brick and mortar retail – retailers, CRE professionals, CPG executives, and financial analysis – stay up to date on their sectors of interest by tracking the performance of specific brands or categories.

The past year and a half has been exciting for the world of gaming. As an alternative to social media and Netflix titles, socially distanced people flocked to gaming platforms. Whether it was attending Travis Scott’s unforgettable concert in Fortnite or buying a Marc Jacobs outfit in Animal Crossing, people found enjoyment in their virtual worlds. August saw many new releases. Did top advertising brands line up with popular launches?

The beauty industry worldwide has been evolving over the past few years, with social media and changing definitions of attractiveness driving forces. In today’s Insight Flash, we dig into how the Beauty Products subindustry has been changing in the UK, focusing on online versus offline sales for direct-to-consumer brands, top spend growth, and average ticket sizes. Like many sectors, UK Beauty Products saw a decline in spend at the beginning of the COVID-19 pandemic last spring.

Your CEO says it’s too aggressive, the product manager says it’s too vague, the sales rep says it’s too long, and support? Well, they feel it doesn’t do much to answer the main questions customers usually ask. For digital researchers or market analysts, this scenario is all too familiar. You just can’t please everyone…or can you? With market segmentation, companies can optimize their digital strategies using an array of targeted messages and content specific to their audience, making sure that everyone, from C-levels to marketers, and customers included, are happy and on the same page.

Chewy is coming out of an exceptionally strong Q1 due in large part to the 2020 national trend towards pet adoption. With investor expectations high and very bullish management guidance in their last call, Chewy will need to deliver dazzling results to satisfy the market. Aggregate active customer growth is strong. However, Similarweb data suggests that the share of the all-important active customers versus non-Autoship customers (Chewy’s subscription program) is in clear decline.

Much like the timeless album cover of Dark Side of the Moon, the pandemic has been a prism for online retailers. It’s now July 2021, and a lot of us are locked up inside with nothing but Pink Floyd’s sampled sounds – like coins in a cash register at the start of Money – to remind us of the outside world. Online shopping has become the norm, and Australians are buying groceries, clothes, and recreational items with a click of their mouse or a swipe of their screen in never-before-seen numbers.

The healthcare industry remains in the spotlight, where it has been firmly planted since the pandemic began. Now with the rapid evolution of Delta and the new wave of cases that have come with it, we see story after story of continued pressure placed on the sector. Workers on the front lines are battling burnout during a wave of the pandemic that is, by and large,most gravely impacting the unvaccinated. Meanwhile, stories emerge almost daily about hospital systems in COVID hotspots on the brink of collapse.

Warby Parker is the latest direct-to-consumer company planning to go public. We reviewed statements made in the company’s S-1 and compared them with Earnest spend data, analyzing how Warby Parker has performed in the eyewear market among competitors like Lenscrafters, Sunglass Hut, and Zenni. We also looked at which eyewear companies have been most successful in retaining existing customers while attracting new buyers.